What is the Electronic Shelf Label Market Overview – definition, scope, and significance?

The Electronic Shelf Label (ESL) market comprises technology solutions that replace traditional paper price tags with digital displays attached to store shelves. These labels convey real‑time pricing, product information, promotions, and compliance data through wireless communication with a central management system. The scope of the market includes hardware components (displays, batteries, transceivers, microprocessors), software platforms that control pricing updates, and related services such as installation, maintenance, and integration with point‑of‑sale (POS) systems. ESLs are significant because they enable retailers to improve pricing accuracy, reduce labor costs associated with manual tag changes, enhance the shopper experience with dynamic content, and gather data for analytics‑driven merchandising.

What are the key drivers, restraints, challenges, and opportunities in the Electronic Shelf Label Market?

Key drivers include the growing need for price agility in highly competitive retail environments, labor cost pressures, and the shift toward omnichannel retailing that requires synchronized online‑offline pricing. Technological advancements in low‑power e‑paper displays and battery life extensions further propel adoption. Restraints stem from the upfront capital investment for large‑scale deployments and integration complexity with legacy IT systems. Challenges involve ensuring label durability in harsh store conditions and managing the cybersecurity of wireless networks. Opportunities arise from emerging use cases such as in‑store navigation, RFID‑enabled inventory tracking, and expansion into non‑food retail segments where dynamic pricing can create new revenue streams.

What current and emerging growth trends are shaping the Electronic Shelf Label Market?

Current trends feature a rapid transition from LCD‑based ESLs to e‑paper displays that offer superior readability, longer battery life, and lower power consumption. Retailers are increasingly adopting cloud‑based management platforms that support AI‑driven price optimization. Emerging trends include the integration of NFC tags for consumer interaction, the use of blockchain for price‐change auditability, and the rollout of ultra‑thin flexible displays that can conform to irregular shelf shapes. Additionally, sustainability concerns are driving demand for labels with recyclable components and extended battery cycles.

How did COVID‑19 impact the Electronic Shelf Label Market and what is the recovery trajectory?

The pandemic accelerated digital transformation in retail as stores sought contact‑less solutions and rapid price updates to respond to supply‑chain disruptions. Demand for ESLs grew as retailers aimed to reduce staff exposure by limiting physical price‑tag changes. Although initial rollout projects were delayed due to lockdowns, the post‑pandemic recovery has been robust, with retailers increasing investments to support omnichannel strategies and enhanced in‑store safety measures. The market is now on a clear upward trajectory, supported by renewed capital spending and heightened focus on automation.

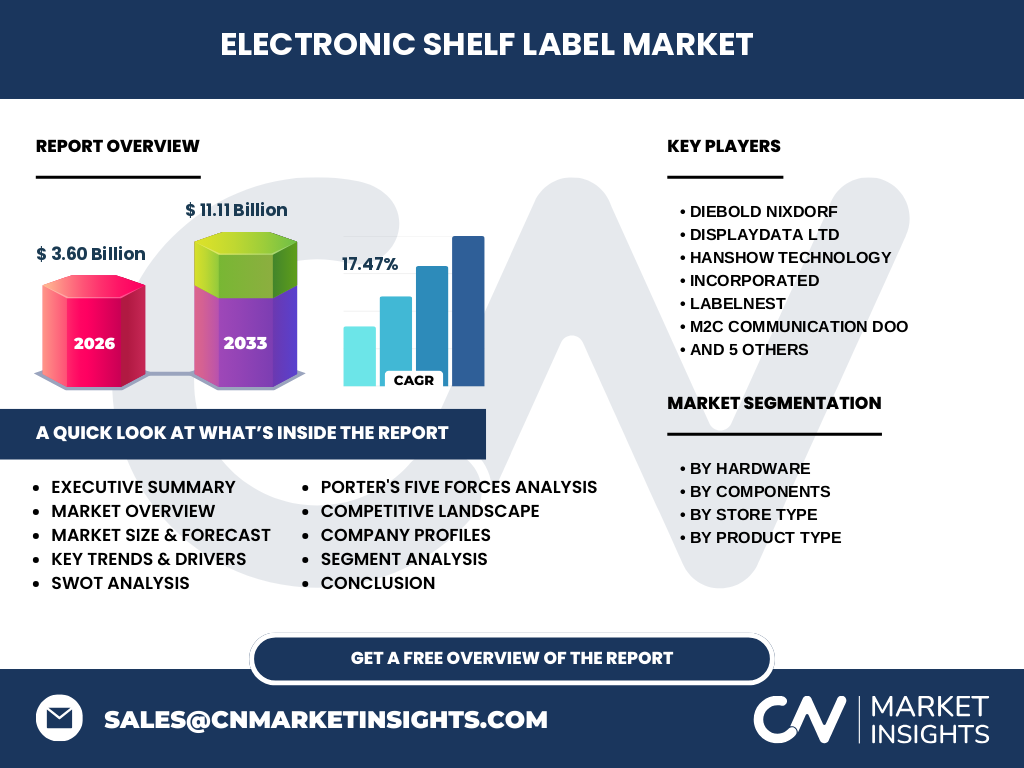

Who are the major competitors and what does the competitive landscape look like in the Electronic Shelf Label Market?

The market is moderately consolidated, featuring a mix of established technology firms and specialized niche players. Leading companies include Diehard Nixdorf, Displaydata Ltd, Hanshow Technology, Incorporated, LabelNest, M2C Communication DOO, Opticon Sensors Europe BV, Panasonic Holdings Corp, Pricer AB, Samsung Electro‑Mechanics Co Ltd, and Ses Imagotag SA. These firms compete on display technology (e‑paper vs. LCD), wireless protocol efficiency, integration capabilities, and service ecosystems. Strategic partnerships with POS vendors and retail consulting firms are common, and recent M&A activity focuses on acquiring software intelligence capabilities to complement hardware offerings.

What are the high‑level insights and key findings in the Executive Summary for the Electronic Shelf Label Market?

The ESL market is projected to expand from a 2026 valuation of $3.60 billion to $11.11 billion by 2033, reflecting a robust CAGR of 17.47 %. Growth is driven by retailer demand for price agility, labor cost reductions, and enhanced shopper engagement. E‑paper displays dominate the hardware segment, while software and services are gaining share as retailers seek integrated pricing intelligence. Geographic expansion in North America and Europe leads the market, with emerging opportunities in Asia‑Pacific’s hyper‑ and specialty stores. Competitive intensity is increasing as incumbents add AI‑powered pricing tools and pursue ecosystem partnerships.

What are the market forecast expectations for the Electronic Shelf Label Market from 2025 to 2032?

Based on the provided CAGR of 17.47 %, the market is expected to continue its rapid expansion throughout the forecast horizon. By 2027 the market size will approach roughly $4.2 billion, climbing to $7.5 billion by 2030, and reaching the projected $11.11 billion by 2033. The forecast reflects sustained retailer investment in digital price‑tagging, escalating adoption across all store types, and incremental revenue from software subscriptions and services that support dynamic pricing models.

How is the Electronic Shelf Label Market sized and shared by segment?

Segmentation by hardware includes Displays, Batteries, Transceivers, and Microprocessors. By components, the market divides into Hardware, Software, and Services. By store type, the categories are Hypermarkets, Supermarkets, Non‑Food Retail Stores, and Specialty Stores. By product type, the market splits into LCD‑based ESL and E‑Paper‑based ESL. While exact monetary shares are not disclosed, the hardware segment—particularly Displays and Batteries—accounts for the largest portion of spend, with Software and Services contributing growing fractions as retailers adopt cloud‑based pricing platforms and maintenance contracts.

What is the global Electronic Shelf Label Market size and share by region?

The global ESL market totals $3.60 billion in 2026. The highest concentration of market activity is observed in North America and Europe, reflecting early adoption by large retail chains and strong technology ecosystems. Asia‑Pacific shows a rapidly expanding share, driven by the rollout of hypermarkets and specialty stores. While specific regional dollar values are not provided, the distribution aligns with the overall growth trajectory and the presence of key OEMs and system integrators in these regions.

What does the regional analysis reveal about the Electronic Shelf Label Market performance?

North America leads in terms of early adoption, with retailers leveraging ESLs to support omnichannel fulfillment and dynamic pricing. Europe follows closely, emphasizing sustainability and regulatory compliance that favor e‑paper solutions. Asia‑Pacific is the fastest‑growing region, where expanding retail footprints in China, India, and Southeast Asia create new deployment opportunities across hypermarkets and specialty stores. Latin America and the Middle East present nascent but promising markets as retailers begin digital transformation initiatives.

What are the profiles and strategies of leading companies in the Electronic Shelf Label Market?

Diehard Nixdorf focuses on end‑to‑end retail solutions, integrating ESL hardware with POS and inventory systems. Displaydata Ltd emphasizes proprietary e‑paper technology and low‑power transceivers. Hanshow Technology targets Asian markets with cost‑effective ESL kits and cloud‑based pricing software. LabelNest offers a subscription‑based service model, bundling hardware, software, and maintenance. Panasonic Holdings Corp leverages its manufacturing scale to provide high‑volume displays, while Pricer AB concentrates on AI‑driven pricing analytics. Samsung Electro‑Mechanics supplies microprocessors and sensors, supporting ecosystem partners.

How does Porter’s Five Forces analysis apply to the Electronic Shelf Label Market?

• Threat of new entrants – Moderate: High capital requirements and the need for specialized hardware expertise deter many entrants, though software‑focused startups may enter via SaaS models. • Bargaining power of buyers – High: Large retail chains negotiate volume discounts and demand integration with existing systems. • Bargaining power of suppliers – Moderate: Component suppliers such as display manufacturers have limited concentration, but critical components like e‑paper displays can exert influence. • Threat of substitutes – Low: Manual price tags are less efficient, and alternative digital signage lacks the shelf‑level specificity of ESLs. • Industry rivalry – High: Numerous vendors compete on technology, price, and service contracts, driving innovation and price pressure.

What are the SWOT findings for the Electronic Shelf Label Market?

Strengths: Proven cost savings, real‑time pricing, and data collection capabilities. Weaknesses: High initial deployment cost and integration complexity. Opportunities: Expansion into non‑food retail, AI‑enabled pricing, and sustainable label design. Threats: Cybersecurity risks, rapid technology obsolescence, and potential regulatory changes affecting wireless communications.

How is the value chain structured in the Electronic Shelf Label Market?

The ESL value chain starts with core component manufacturers (display panels, batteries, microprocessors), proceeds to system integrators that assemble hardware and embed firmware, continues with software developers delivering cloud‑based management platforms, and ends with retailers who deploy the labels and consume data services. After‑sales support, maintenance, and periodic label replacement form the service layer that adds recurring revenue.

What key investment insights can be drawn for the Electronic Shelf Label Market?

Investors should prioritize companies that combine robust hardware with scalable software platforms, as recurring subscription revenue enhances valuation stability. Funding opportunities exist in firms developing ultra‑low‑power e‑paper displays, AI‑driven pricing engines, and secure wireless protocols. Strategic partnerships with major POS providers can accelerate market penetration. Geographic diversification, especially targeting fast‑growing Asia‑Pacific retailers, offers upside potential.

What conclusions can be drawn about the Electronic Shelf Label Market?

The ESL market is on a high‑growth trajectory, driven by retailer demand for automation, price agility, and enhanced shopper experiences. The shift toward e‑paper technology, combined with software and services expansion, positions the market for sustained revenue growth through 2033. Competitive dynamics encourage continuous innovation, while emerging use cases broaden the addressable retail base.

What research methodology was employed to compile this Electronic Shelf Label Market report?

The study used a mixed‑method approach, combining primary interviews with industry experts, vendor questionnaires, and secondary data collection from company filings, press releases, and reputable market databases. Quantitative data were validated through cross‑reference with financial reports and trend analysis, while qualitative insights were synthesized to identify drivers, challenges, and strategic themes.

What is the scope of this research and its limitations?

The research covers global market size, segmentation by hardware, components, store type, and product type, as well as regional performance, competitive landscape, and forward‑looking forecasts through 2033. Limitations include reliance on publicly available financial figures and the exclusion of proprietary data not disclosed by companies, which may affect granularity of market share estimates.

Which key companies are highlighted and what recent developments have they announced?

Key players include Diehard Nixdorf (launched a cloud‑based pricing analytics module), Displaydata Ltd (introduced a next‑generation e‑paper display with 5‑year battery life), Hanshow Technology (secured a partnership with a major Asian hypermarket chain), LabelNest (rolled out a subscription service bundling hardware and software), Panasonic Holdings Corp (expanded its display manufacturing capacity in Southeast Asia), Pricer AB (acquired a AI pricing startup), Samsung Electro‑Mechanics (released a low‑power microprocessor for ESLs), and Ses Imagotag SA (opened a new R&D center focused on NFC integration). These developments underscore the market’s emphasis on integration, sustainability, and intelligent pricing.