1. What is the Rainscreen Cladding Market Overview – definition, scope, and significance?

The rainscreen cladding market comprises products and services that provide a ventilated façade system designed to protect building envelopes from moisture, improve thermal performance, and enhance aesthetic appeal. Its scope covers a wide range of applications—including residential, commercial, and industrial projects—and spans various materials such as ceramic, timber, composite material, and metal. The market is significant because it supports modern construction trends focused on energy efficiency, durability, and sustainable design, while also meeting increasingly stringent building codes worldwide.

2. What are the main drivers, restraints, challenges, and opportunities in the Rainscreen Cladding Market?

Key drivers include heightened demand for energy‑efficient building envelopes, stricter regulations on moisture management, and growing aesthetic preferences for high‑performance façades. Restraints stem from higher upfront material costs and the need for skilled installation. Challenges involve supply‑chain disruptions for specialized components and regional variations in construction standards. Opportunities arise from innovations in lightweight composite systems, increasing retro‑fit projects, and expanding market presence in emerging economies where new construction is accelerating.

3. Which growth trends are currently shaping the Rainscreen Cladding Market?

Current trends feature a shift toward eco‑friendly composite materials that combine durability with reduced carbon footprints. Integration of digital design tools and Building Information Modeling (BIM) is streamlining specification and coordination processes. Additionally, there is a rising preference for customizable façade panels that allow architects to achieve unique visual effects while maintaining performance standards. The market also sees growing adoption of prefabricated modules that shorten construction timelines.

4. How did COVID‑19 impact the Rainscreen Cladding Market and what is the recovery trajectory?

The pandemic caused temporary project delays, labor shortages, and supply‑chain constraints, which slowed demand in 2020‑2021. However, the sector rebounded quickly as construction activity resumed, driven by stimulus‑driven infrastructure spending and a surge in residential building projects. Recovery is now robust, with the market regaining momentum and positioning itself for sustained growth through 2032.

5. What does the competitive landscape of the Rainscreen Cladding Market look like?

The market is moderately consolidated, featuring several global players with strong product portfolios and extensive distribution networks. Major competitors such as Carea Ltd, Fundermax North America Inc., James Hardie Building Products Inc., Kingspan Group Plc, Knauf Digital GmbH, Merson Group, Nucor Corp, ROCKWOOL A/S, Soprema Insulation Limited, and Trespa International B.V. dominate key segments. Competition focuses on material innovation, strategic partnerships, and geographic expansion, leading to occasional mergers and acquisitions that further consolidate market share.

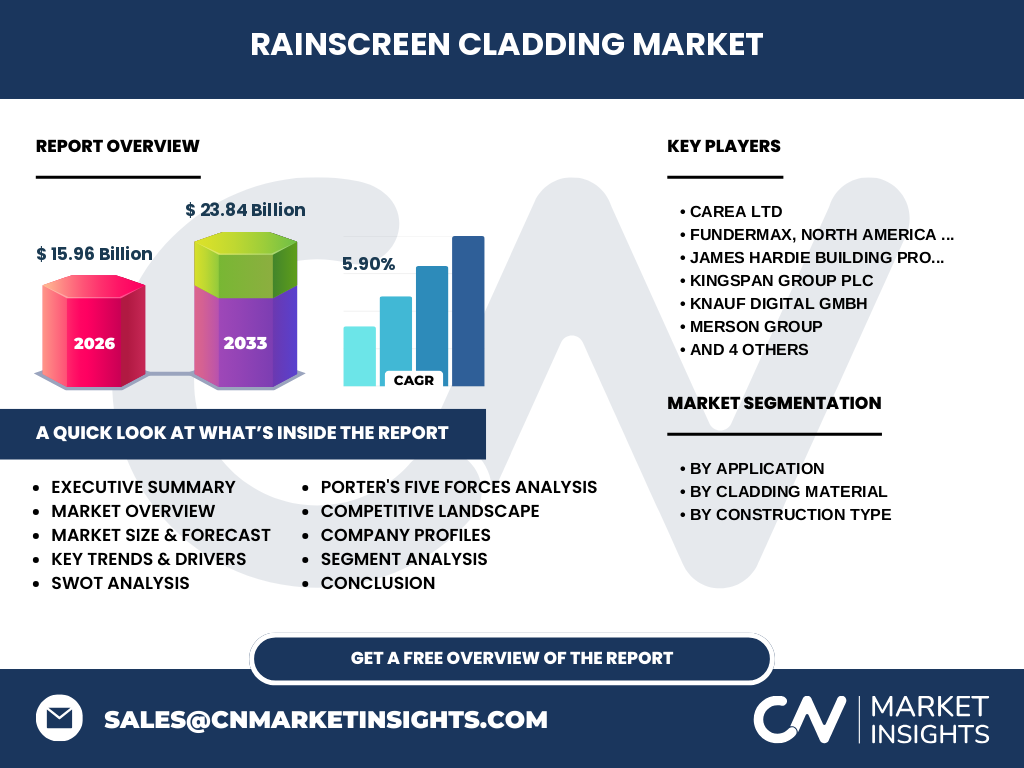

6. What are the key findings highlighted in the executive summary?

The executive summary emphasizes a market valued at USD 15.96 billion in 2026, with a projected expansion to USD 23.84 billion by 2033, reflecting a healthy CAGR of 5.90 %. Growth is propelled by demand across residential, commercial, and industrial applications, as well as by ongoing new‑construction and renovation activities. Material diversification, especially toward composites, and regional expansion in high‑growth zones are identified as critical success factors.

7. What are the forecast expectations for the Rainscreen Cladding Market from 2025 to 2032?

Forecasts indicate a steady upward trajectory, maintaining the 5.90 % compound annual growth rate through 2032. The market is expected to benefit from continued urbanization, stricter façade performance standards, and increasing retro‑fit projects. The forecast underscores sustained investment in research and development, particularly for lightweight, high‑performance composites and metal systems that address both sustainability and design flexibility.

8. How is the Rainscreen Cladding Market sized and shared by segmentation?

Segmentation by application shows residential, commercial, and industrial end‑uses each contributing to overall demand, with residential typically leading due to the volume of new housing construction. By cladding material, ceramic, timber, composite material, and metal each serve distinct architectural preferences and performance requirements; composite material is gaining traction for its balance of strength and weight. Segmentation by construction type highlights that both new construction and renovation projects drive market volume, with renovation gaining importance as existing building envelopes are upgraded for energy efficiency.

9. What is the global geographic distribution of the Rainscreen Cladding Market?

The market exhibits a worldwide footprint, with strong presence in North America and Europe where building codes heavily favor moisture‑controlled façades. Asia‑Pacific shows rapid growth due to expanding urban infrastructure and rising awareness of high‑performance envelope solutions. While specific regional revenue figures are not disclosed, the overall global size of USD 15.96 billion in 2026 reflects balanced contributions from mature and developing regions.

10. How does each region perform in the Rainscreen Cladding Market?

North America benefits from extensive commercial and industrial projects, coupled with stringent energy codes that promote rainscreen systems. Europe leverages historic retro‑fit initiatives and a strong tradition of durable façade solutions. Asia‑Pacific’s performance is fueled by large‑scale residential and mixed‑use developments, alongside government incentives for green construction. Emerging markets in Latin America and the Middle East are beginning to adopt rainscreen technologies as part of their modernization agendas.

11. Which companies lead the Rainscreen Cladding Market and what are their strategies?

Leading firms include Carea Ltd, which focuses on innovative ceramic panels; Fundermax North America Inc., known for high‑performance composite systems; James Hardie Building Products Inc., a dominant player in fiber‑cement solutions; Kingspan Group Plc, emphasizing insulated metal cladding; Knauf Digital GmbH, leveraging digital fabrication; Merson Group, with a broad timber portfolio; Nucor Corp, offering durable metal cladding; ROCKWOOL A/S, integrating insulation with façade systems; Soprema Insulation Limited, combining waterproofing with rainscreen; and Trespa International B.V., renowned for premium composite panels. Their strategies revolve around product differentiation, sustainability commitments, and expanding distribution channels.

12. What does Porter’s Five Forces reveal about the Rainscreen Cladding Market?

• Threat of new entrants: Moderate, due to high capital requirements and technical expertise needed for product development. • Bargaining power of suppliers: Moderate, as raw materials like metal and composites are sourced from a limited number of specialized providers. • Bargaining power of buyers: High, with architects and developers demanding performance, price, and design flexibility. • Threat of substitutes: Low to moderate, because alternative façade systems lack the moisture‑ventilation benefits of rainscreen technology. • Industry rivalry: Intense, driven by product innovation, geographic expansion, and strategic alliances among established players.

13. What are the SWOT insights for the Rainscreen Cladding Market?

Strengths: Proven moisture‑management performance, alignment with sustainability goals, and broad material options. Weaknesses: Higher initial costs and the need for skilled installation. Opportunities: Growth in retro‑fit projects, development of lightweight composites, and expansion into emerging economies. Threats: Volatile raw‑material prices, potential regulatory changes, and competition from alternative façade technologies.

14. How does the value chain of the Rainscreen Cladding Market operate?

The value chain begins with raw‑material suppliers (metal alloys, ceramic powders, timber, composites), followed by component manufacturers who produce panels and framing systems. Next, the distribution layer includes regional distributors and specialty façade contractors. Installation services constitute the final stage, often involving architects, engineers, and construction firms. After‑sales support—such as maintenance, warranties, and performance monitoring—adds value and reinforces long‑term product reliability.

15. What key investment insights can be drawn for the Rainscreen Cladding Market?

Investors should prioritize companies that demonstrate strong R&D pipelines in composite and metal technologies, as these segments are poised for growth. Strategic alliances with BIM software providers can create differentiation. Geographic diversification—particularly entry into high‑growth Asia‑Pacific markets—offers upside potential. Additionally, firms with robust retro‑fit capabilities are well‑positioned to capture demand from building‑envelope upgrades driven by energy‑efficiency regulations.

16. What conclusions can be drawn about the Rainscreen Cladding Market?

The rainscreen cladding market is on a solid growth path, supported by a 5.90 % CAGR and a forecasted increase from USD 15.96 billion (2026) to USD 23.84 billion (2033). Its relevance is reinforced by sustainability imperatives, regulatory pressure, and architectural trends favoring high‑performance façades. While cost and skilled‑labour considerations remain, ongoing material innovation and expanding regional demand create a compelling outlook for manufacturers, investors, and end‑users alike.

17. What research methodology was applied to develop this market report?

The study employed a mixed‑method approach, combining primary interviews with industry experts, manufacturers, and key buyers, together with secondary data collection from company filings, trade publications, and reputable market databases. Quantitative data were validated through triangulation, and qualitative insights were synthesized to produce forward‑looking forecasts. Trend analysis, competitive benchmarking, and scenario modelling were also utilized to ensure robustness.

18. What is the scope of this research and its limitations?

The scope covers global market size, segmentation by application, material,