What is the Connected Gym Equipment Market and why is it significant?

The Connected Gym Equipment Market comprises fitness machines that integrate digital technologies—such as sensors, wireless connectivity, and interactive software—to capture performance data, deliver personalized workouts, and enable remote monitoring. Its scope covers both cardiovascular and strength‑training devices used in residential, commercial gym, and other commercial settings. Significance stems from the shift toward data‑driven health management, rising consumer demand for immersive workout experiences, and the strategic importance of retaining members through technology‑enabled engagement.

What are the main drivers, restraints, challenges, and opportunities shaping the Connected Gym Equipment Market?

Key drivers include increasing health awareness, growing adoption of IoT in fitness, and the need for real‑time analytics to improve training outcomes. Restraints arise from high upfront costs of smart equipment and concerns over data privacy. Challenges involve integration complexity with legacy gym management systems and the rapid pace of technological change. Opportunities lie in expanding subscription‑based services, leveraging AI for personalized coaching, and tapping emerging markets where gym penetration is still low.

Which growth trends are currently influencing the Connected Gym Equipment Market?

Current trends feature gamified workout platforms, hybrid models combining on‑site and virtual classes, and the rise of subscription ecosystems that bundle hardware with software content. Manufacturers are embedding AI algorithms for automatic resistance adjustment, while wearables are increasingly synchronized with gym machines to provide holistic health insights. Additionally, the proliferation of cloud‑based data storage enables multi‑location analytics for franchise operators.

How did COVID‑19 affect the Connected Gym Equipment Market and what is the recovery trajectory?

The pandemic accelerated home‑fitness adoption, prompting a surge in residential purchases of connected treadmills, bikes, and strength rigs. Commercial gyms faced closures, leading many operators to retrofit existing fleets with connectivity to offer virtual coaching and retain members. Recovery is characterized by a hybrid demand pattern: continued growth in home‑based solutions alongside renewed investment by gyms seeking to differentiate through data‑rich member experiences.

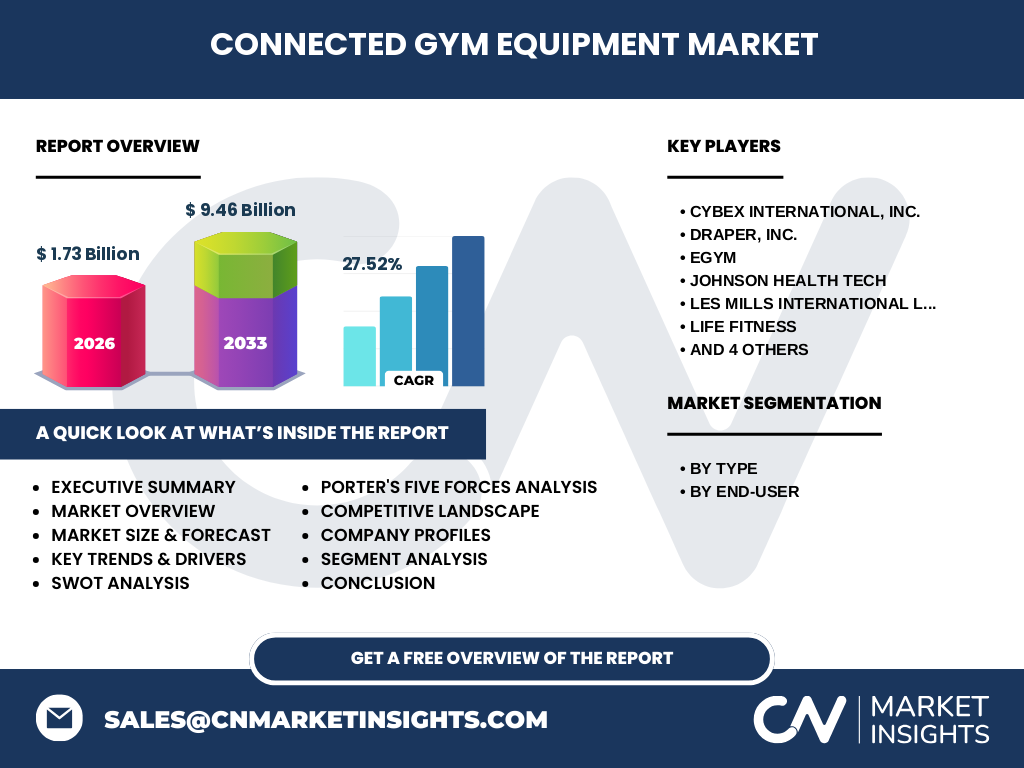

Who are the major competitors in the Connected Gym Equipment Market and what does the competitive landscape look like?

The market is populated by established fitness equipment manufacturers that have embraced digital transformation. Leading players include Cybex International, Draper, EGYM, Johnson Health Tech, LES MILLS INTERNATIONAL, Life Fitness, Nautilus, Precor, TRUE Fitness Technology, and Technogym. Consolidation is evident through strategic acquisitions and partnerships aimed at bolstering software capabilities, creating a landscape where few large firms dominate while niche innovators focus on specialized connectivity solutions.

What are the high‑level takeaways and key findings about the Connected Gym Equipment Market?

The market is expanding rapidly, with a 2026 valuation of $1.73 billion and a projected surge to $9.46 billion by 2033, reflecting a robust CAGR of 27.52 %. Demand is driven by health consciousness, IoT adoption, and the desire for personalized fitness experiences. Both residential and commercial segments are growing, but the residential side showed the fastest uptake during the pandemic. Competitive pressure is intensifying as firms invest heavily in software ecosystems.

What are the market forecasts for the Connected Gym Equipment Market from 2025 to 2032?

Based on the provided CAGR of 27.52 %, the market is expected to maintain strong upward momentum throughout the forecast horizon. While specific yearly figures are not disclosed, the trajectory indicates a multi‑fold increase, positioning the sector as one of the fastest‑growing segments within the broader fitness industry. Strategic planning should account for accelerating adoption rates and the need for scalable digital infrastructure.

How is the Connected Gym Equipment Market sized and shared by type and end‑user?

Segmentation by type includes Cardiovascular Training and Strength Training equipment, each integrating connectivity features. By end‑user, the market splits into Residential, Gym, and Other Commercial Users. While exact monetary splits are not provided, the residential segment experienced notable acceleration during COVID‑19, whereas gyms are investing in upgrades to retain members. Strength‑training devices are gaining traction due to AI‑driven load adjustments, while cardio machines remain a staple for data‑rich cardio monitoring.

What is the geographic distribution of the Global Connected Gym Equipment Market?

The market exhibits a worldwide footprint, with major demand clusters in North America, Europe, and Asia‑Pacific. These regions benefit from high disposable incomes, advanced digital infrastructure, and strong fitness culture. Emerging economies within Asia‑Pacific are projected to accelerate adoption as urban gym concepts and home‑fitness platforms expand.

What are the regional performance highlights for the Connected Gym Equipment Market?

North America leads in early adoption, driven by consumer willingness to invest in premium connected devices and a mature commercial gym ecosystem. Europe follows closely, with regulatory support for health initiatives and strong boutique‑studio growth. Asia‑Pacific presents the highest growth potential, fueled by rising middle‑class populations, expanding gym chains, and increasing acceptance of smart home fitness solutions.

Which companies are leading the Connected Gym Equipment Market and what strategies are they pursuing?

Key players such as Technogym, Life Fitness, and Precor are focusing on end‑to‑end ecosystems that combine hardware, subscription content, and analytics dashboards. Cybex and EGYM are leveraging partnerships with digital health platforms to broaden data integration. Johnson Health Tech and Nautilus are expanding their global distribution networks, while TRUE Fitness Technology emphasizes AI‑enabled adaptive resistance. These strategies underline a shift from pure equipment sales to recurring revenue models.

How does Porter’s Five Forces framework apply to the Connected Gym Equipment Market?

Threat of new entrants is moderate; high capital requirements and technology expertise create barriers, yet niche startups can disrupt with innovative software. Bargaining power of buyers is increasing as gyms demand integrated solutions and consumers seek affordable subscription models. Bargaining power of suppliers is low to moderate, given the availability of generic sensor components. Threat of substitutes includes traditional non‑connected equipment and virtual‑only fitness apps. Competitive rivalry is intense, driven by rapid product cycles and the race to secure proprietary data platforms.

What are the strengths, weaknesses, opportunities, and threats (SWOT) of the Connected Gym Equipment Market?

Strengths: strong growth trajectory, high consumer engagement, and data monetization potential. Weaknesses: high initial cost and reliance on stable internet connectivity. Opportunities: expansion into emerging markets, development of AI‑driven coaching, and bundling of health‑service subscriptions. Threats: data‑privacy regulations, rapid technology obsolescence, and competitive pressure from pure‑software fitness providers.

How is value created and transferred within the Connected Gym Equipment value chain?

The value chain begins with component suppliers (sensors, connectivity modules), proceeds to OEMs that integrate hardware and software, followed by cloud service providers that host data platforms. Distributors and retailers bring products to end‑users, while fitness app developers and gym management software firms add value through analytics and content. Finally, after‑sales services, data analytics, and subscription renewals sustain revenue streams.

What investment insights can be drawn from the Connected Gym Equipment Market?

Investors should focus on companies that demonstrate strong software ecosystems, recurring‑revenue models, and strategic partnerships with health‑tech platforms. Capital allocation toward R&D in AI and data security will likely yield competitive advantage. Emerging geographic hubs, particularly in Asia‑Pacific, present attractive entry points for growth capital, while North American and European incumbents offer stable cash flows.

What are the concluding observations for the Connected Gym Equipment Market?

The Connected Gym Equipment Market is on a decisive upward path, underpinned by a compelling blend of health trends and digital innovation. With a projected market size of $9.46 billion by 2033 and a CAGR exceeding 27 %, the sector promises significant revenue potential. Success will hinge on delivering seamless user experiences, protecting data, and evolving subscription‑based business models.

How was the research for this report conducted?

Primary research involved interviews with industry executives, gym operators, and technology providers. Secondary sources comprised company filings, market databases, industry publications, and analyst reports. Data triangulation ensured consistency, while trend analysis leveraged historical performance and forward‑looking indicators to derive the forecast.

What is the scope of this research and its limitations?

The study covers global market dynamics, segmentation by equipment type and end‑user, and regional performance across major geographies. It excludes detailed financial breakdowns beyond the provided market size and CAGR, and does not quantify competitive shares for individual companies due to data constraints.

Which key companies are active in the Connected Gym Equipment Market and what recent developments have they announced?

Prominent players include Cybex International, Draper, EGYM, Johnson Health Tech, LES MILLS INTERNATIONAL, Life Fitness, Nautilus, Precor, TRUE Fitness Technology, and Technogym. Recent developments feature Technogym’s launch of a cloud‑based training platform, Life Fitness’s acquisition of a digital content startup, EGYM’s partnership with a leading health‑app provider, and Precor’s rollout of AI‑enabled strength machines across North American gym chains. These activities highlight a market focus on software integration, content expansion, and strategic alliances.