What is the Europe 5G Chipset Market Overview – Definition, scope, and significance?

The Europe 5G chipset market comprises semiconductor components that enable the transmission, reception, and processing of fifth‑generation (5G) radio signals across a variety of devices and infrastructure. This market covers chipsets used in mobile phones, automotive telematics, industrial IoT gateways, network base stations, and customer‑premises equipment such as routers and smart‑home hubs. Its scope includes products operating in sub‑6 GHz bands as well as millimeter‑wave (mmWave) frequencies ranging from 26 GHz to above 39 GHz. The significance of this market lies in its role as the technological backbone of Europe’s digital transformation, supporting ultra‑low latency, massive device connectivity, and high‑throughput applications that drive smart cities, autonomous vehicles, and Industry 4.0 initiatives.

What are the Europe 5G Chipset Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include strong governmental commitments to 5G rollout, substantial public‑private investment in broadband infrastructure, and growing demand for high‑speed connectivity in automotive, healthcare, and industrial sectors. The push for greener, energy‑efficient networks also accelerates adoption of advanced chipset designs. Restraints stem from high R&D costs, complex certification processes, and geopolitical tensions that affect supply chains, particularly for components sourced outside Europe. Challenges involve the need for skilled semiconductor talent and the integration of diverse frequency bands within a single platform. Opportunities arise from emerging use cases such as private 5G networks for manufacturing, edge‑computing deployments, and the forthcoming expansion of mid‑band spectrum, which will stimulate demand for versatile, multi‑band chipsets.

What are the Europe 5G Chipset Market Growth Trends?

Current trends show a steady shift from single‑band to multi‑band chipset solutions that can operate across sub‑6 GHz and mmWave spectra, enabling seamless handover and better coverage. There is also a noticeable increase in the integration of AI accelerators within chipsets to support real‑time analytics at the edge. OEMs are consolidating designs to reduce bill‑of‑materials costs, resulting in system‑on‑chip (SoC) architectures that combine baseband, RF front‑end, and power management. Moreover, the automotive sector is moving from prototype deployments to volume production of 5G‑enabled infotainment and V2X systems, creating a distinct growth segment.

How has COVID‑19 impacted the Europe 5G Chipset Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains for raw silicon and testing equipment, causing temporary production bottlenecks. However, remote work and heightened demand for reliable high‑speed connectivity accelerated investment in network upgrades, offsetting early setbacks. Post‑2020, the market rebounded strongly, with an increased focus on building resilient, cloud‑native 5G infrastructure. The recovery trajectory remains positive, supported by renewed capital expenditures from telecom operators and the continued rollout of 5G services across major European cities.

Who are the major competitors in the Europe 5G Chipset Market and what is the competitive landscape?

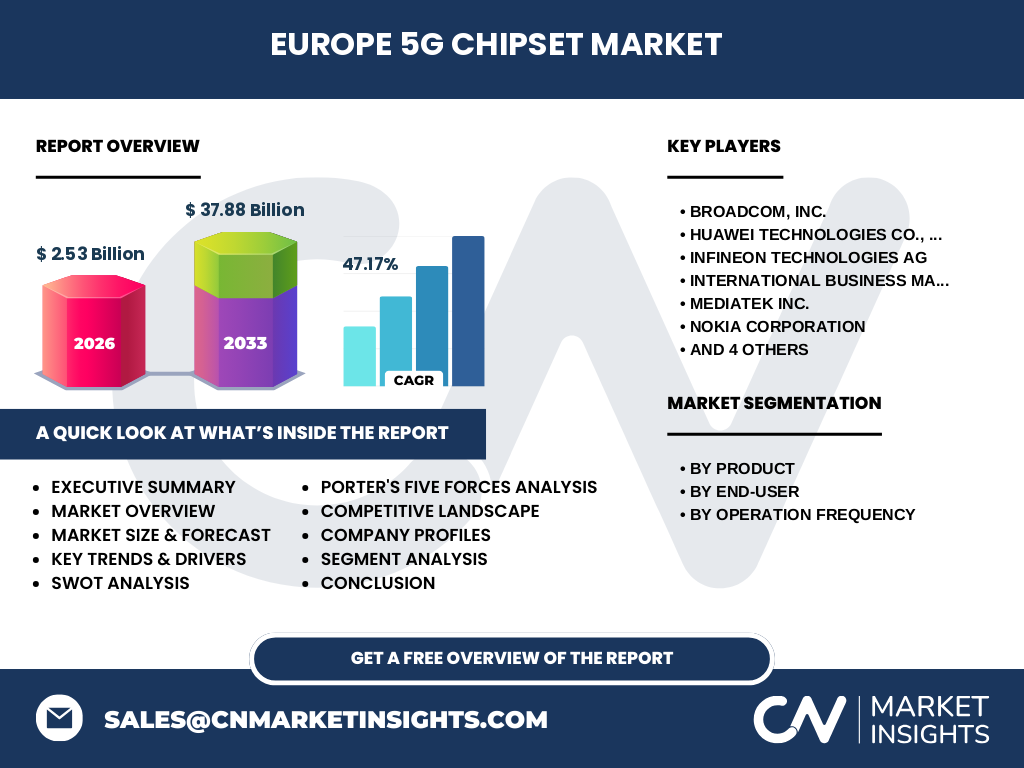

The competitive landscape is dominated by a mix of global semiconductor giants and specialized European players. Leading firms include Broadcom, Inc., Huawei Technologies, Infineon Technologies AG, IBM, MediaTek, Nokia, Qualcomm, Samsung Electronics, Ericsson, and Xilinx. These companies compete on technology leadership, frequency‑band coverage, power efficiency, and integration capabilities. Recent market consolidation has been modest, with strategic alliances forming around joint R&D programs and shared IP portfolios, while acquisitions are focused on niche RF and AI‑accelerator assets.

What are the key findings in the Executive Summary of the Europe 5G Chipset Market?

The Europe 5G chipset market is projected to expand from a 2026 valuation of €2.53 billion to €37.88 billion by 2033, reflecting a robust compound annual growth rate of 47.17 %. Growth is propelled by multi‑band chipset innovation, expanding use cases in automotive and industrial automation, and strong policy backing for 5G coverage. Competitive pressure is intensifying as incumbents invest heavily in AI‑enabled SoC designs, while new entrants focus on niche frequency bands. The market offers attractive investment prospects, particularly in the sub‑6 GHz and 26‑39 GHz segments where demand for versatile, low‑latency solutions is highest.

What is the Europe 5G Chipset Market Forecast for 2025‑2032?

Based on the provided CAGR of 47.17 %, the market is expected to maintain an accelerated growth path throughout the 2025‑2032 horizon. The forecast anticipates a steady increase in annual revenues, driven by expanding deployments of 5G network infrastructure and the proliferation of 5G‑enabled devices across all end‑user categories. The upward trajectory will be reinforced by emerging standards for higher frequency bands and the growing adoption of private 5G networks in manufacturing hubs.

How is the Europe 5G Chipset Market sized and shared by segmentation?

Segmentation by product reveals three primary categories: Devices, Customer Premises Equipment (CPE), and Network Infrastructure Equipment. Devices represent the largest share, reflecting strong consumer demand for 5G‑enabled smartphones and wearables. CPE, including routers and gateways, holds a significant portion as enterprises modernize connectivity. Network Infrastructure Equipment, encompassing base‑station radios and core‑network processors, accounts for a growing slice due to extensive rollout programs. By end‑user, automotive & transportation, industrial automation, and consumer electronics dominate, while healthcare, retail, and public safety exhibit steady growth. Frequency‑wise, sub‑6 GHz maintains the broadest adoption, while the 26‑39 GHz band is gaining traction for high‑capacity urban deployments, and above‑39 GHz is positioned for niche ultra‑high‑speed scenarios.

What is the Global Europe 5G Chipset Market size and share by region?

The Europe 5G chipset market, valued at €2.53 billion in 2026, represents a key segment of the global 5G chipset ecosystem. While precise figures for other regions are not disclosed, Europe’s share underscores its strategic importance as a hub for advanced telecommunications standards, strong regulatory frameworks, and a concentration of leading chipset manufacturers. The market’s projected expansion to €37.88 billion by 2033 highlights Europe’s role in driving global demand for next‑generation semiconductor solutions.

What does the Regional Analysis of the Europe 5G Chipset Market reveal?

Regional analysis shows that Western Europe, led by Germany, France, and the United Kingdom, is the primary driver of chipset adoption due to early 5G network launches and substantial automotive production. Northern Europe contributes with high levels of IoT integration and smart‑city projects, while Southern and Eastern European markets are accelerating deployment as part of EU cohesion funds. The varied pace of spectrum allocation across these sub‑regions creates differentiated demand for sub‑6 GHz versus mmWave chipsets, influencing product roadmaps for manufacturers.

Which companies lead the Europe 5G Chipset Market and what are their strategies?

Broadcom focuses on high‑performance RF front‑end modules and leverages its extensive IP portfolio to capture network‑infrastructure orders. Huawei, despite regulatory pressures, emphasizes cost‑effective multi‑band solutions for both devices and CPE. Infineon targets automotive and industrial segments with robust, safety‑rated silicon. IBM contributes AI acceleration capabilities that are integrated into chipset designs for edge computing. MediaTek drives volume growth in consumer devices through aggressive pricing and integration of 5G with application processors. Nokia and Ericsson, as telecom equipment leaders, secure chipset contracts tied to their radio access network (RAN) solutions. Qualcomm remains a dominant force in mobile chipset technology, while Samsung combines memory and processing expertise to deliver integrated platforms. Xilinx provides programmable logic that enables customized RF front‑end configurations for niche applications.

How does Porter’s Five Forces analysis apply to the Europe 5G Chipset Market?

Threat of New Entrants: High capital requirements and complex IP landscapes create substantial barriers, limiting new entrants. Bargaining Power of Suppliers: Semiconductor fab facilities and raw‑material providers wield moderate power due to limited capacity for advanced nodes. Bargaining Power of Buyers: Telecom operators and OEMs possess strong negotiating leverage, especially in large volume contracts. Threat of Substitutes: Alternative wireless technologies (e.g., Wi‑Fi 6E, satellite broadband) pose limited substitution risk for core 5G services. Industry Rivalry: Intense competition among established players drives rapid innovation, price competition, and strategic collaborations.

What are the SWOT insights for the Europe 5G Chipset Market?

Strengths: Mature R&D ecosystem, strong policy support, and a diversified customer base across multiple verticals. Weaknesses: Dependency on a few advanced fabs and geopolitical supply‑chain vulnerabilities. Opportunities: Expansion of private 5G networks, rising demand for AI‑enabled edge chipsets, and emerging mmWave applications in smart‑city deployments. Threats: Trade restrictions, rapid technology obsolescence, and potential market saturation in consumer devices.

What does the Europe 5G Chipset Market value chain look like?

The value chain begins with raw silicon wafer production, followed by design and IP licensing, front‑end wafer fabrication, back‑end assembly and testing, and finally system integration into devices, CPE, or network hardware. Key value‑adding activities include custom RF front‑end design, power‑management optimization, and software/firmware development for protocol stack compliance. Distribution occurs through OEM partnerships, direct sales to telecom operators, and channel partners for industrial solutions.

What key investment insights can be drawn from the Europe 5G Chipset Market?

Investors should focus on companies that demonstrate a clear roadmap for multi‑band, AI‑integrated chipset platforms and possess strong IP portfolios. Partnerships with automotive OEMs and participation in EU‑funded 5G pilot programs provide de‑risked growth pathways. Capital allocation toward fab capacity expansion and advanced packaging technologies (e.g., chip‑on‑wafer) is likely to yield high returns given the market’s projected CAGR of 47.17 %.

What are the main conclusions of the Europe 5G Chipset Market report?

The Europe 5G chipset market is on a rapid expansion trajectory, driven by extensive network rollouts, diversified end‑user demand, and aggressive innovation in multi‑band and AI‑enabled designs. The market’s valuation growth from €2.53 billion in 2026 to €37.88 billion by 2033 reflects both strong policy backing and commercial opportunity across automotive, industrial, and consumer sectors. Competitive dynamics favor firms with deep IP assets and flexible manufacturing capabilities, while strategic investments in private 5G and edge computing present the most lucrative avenues.

How was the research for this report conducted?

The study employed a mixed‑method approach, combining primary interviews with industry executives, secondary data extraction from financial statements, regulatory filings, and reputable market databases. Trend analysis leveraged historical shipment data, spectrum allocation timelines, and technology roadmaps. Forecast modeling applied the disclosed CAGR of 47.17 % and incorporated scenario‑based adjustments for macro‑economic variables.

What is the scope of this research and its limitations?

The scope covers the Europe 5G chipset market across product, end‑user, and frequency‑band dimensions, with a temporal focus from 2026 to 2033. It includes major OEMs, telecom operators, and component suppliers active in the region. Limitations stem from the reliance on publicly available financial figures and the exclusion of confidential contract values, which may affect granular market‑share calculations.

Which key companies are highlighted and what recent developments have they announced?

Highlighted firms include Broadcom, Huawei, Infineon, IBM, MediaTek, Nokia, Qualcomm, Samsung, Ericsson, and Xilinx. Recent developments feature Broadcom’s launch of a high‑efficiency mmWave front‑end module, Huawei’s partnership with European automakers for V2X chipsets, Infineon’s rollout of automotive‑grade silicon for next‑gen driver assistance systems, IBM’s integration of AI inference engines into edge chipsets, MediaTek’s release of a cost‑optimized sub‑6 GHz solution for IoT gateways, Nokia’s collaboration with national operators on private 5G networks, Qualcomm’s announcement of a 7‑nm multi‑band SoC for smartphones, Samsung’s advancement in 3‑nm packaging for network equipment, Ericsson’s acquisition of a RF‑design specialist, and Xilinx’s supply of programmable logic for customizable mmWave front‑ends.