Retail Clinics Market Overview - Definition, scope, and significance?

The Retail Clinics Market comprises walk‑in health facilities located within retail environments such as stores, malls, and other high‑traffic venues. These clinics deliver primary care, preventive services, and point‑of‑care diagnostics, often staffed by nurse practitioners or physician assistants. Their significance lies in expanding access to convenient, low‑cost medical care, reducing the burden on emergency departments, and integrating health services directly into consumers’ daily shopping journeys.

Retail Clinics Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising consumer demand for convenient care, increasing chronic disease prevalence, and expanding insurance coverage for preventive services. Opportunities arise from telehealth integration, partnerships with pharmacy chains, and the rollout of vaccination programs. Restraints involve regulatory variability across jurisdictions and concerns about care continuity. Challenges stem from workforce shortages, reimbursement complexities, and competition from urgent‑care centers.

Retail Clinics Market Growth Trends - Current and emerging trends shaping the market?

Current trends feature a shift toward store‑based clinics supported by digital appointment platforms and AI‑enabled triage tools. Emerging trends include mobile retail clinics, collaborative models with hospital systems, and expanded service lines such as point‑of‑care diagnostics for clinical chemistry and immunoassays. Growing emphasis on vaccination services, especially seasonal flu and COVID‑19 boosters, is also reshaping clinic offerings.

COVID-19 Impact on the Retail Clinics Market - Pandemic effects and recovery trajectory?

The pandemic accelerated adoption of retail clinics as safe, community‑based sites for testing, vaccination, and urgent care. Initial lockdowns reduced foot traffic, but rapid implementation of infection‑control protocols restored confidence. Post‑pandemic, clinics have retained higher patient volumes by leveraging vaccination campaigns and telehealth, positioning the market on a strong recovery path that supports the projected CAGR of 10.47%.

Retail Clinics Market Competitive Landscape - Major competitors and market consolidation?

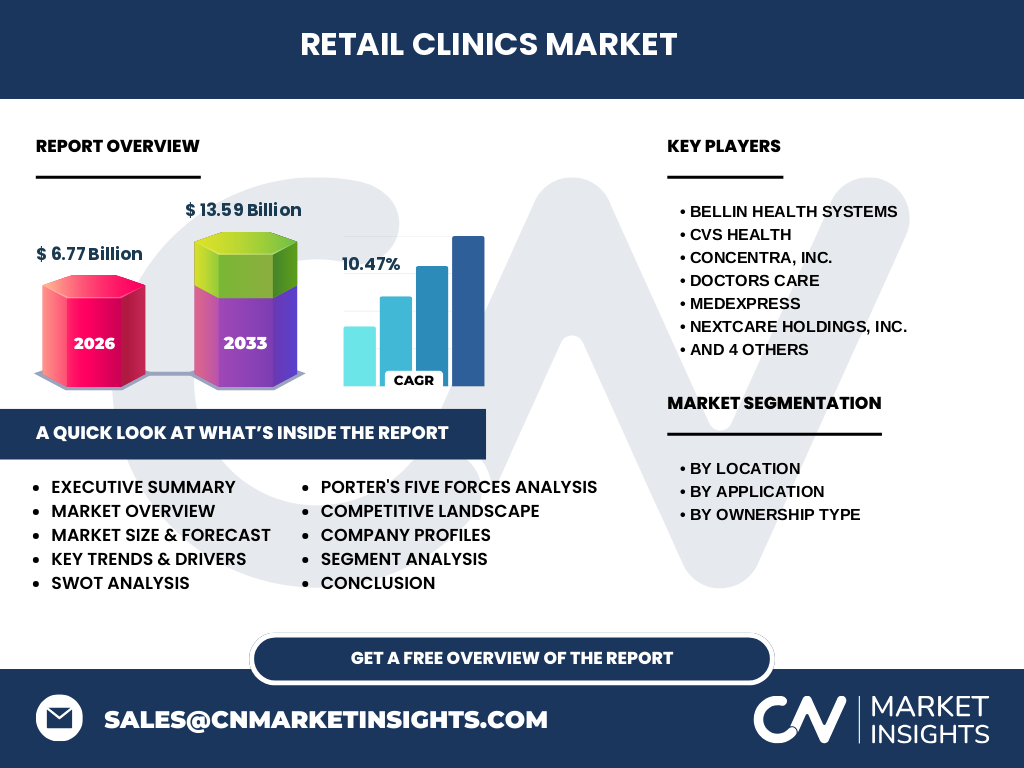

The competitive arena is dominated by large pharmacy and retail chains such as CVS Health, Walgreens, Walmart, and The Kroger Co., complemented by specialist operators like Bellin Health Systems, MedExpress, and Nextcare Holdings. Recent consolidation includes acquisitions of smaller clinic operators by these giants to broaden geographic reach and integrate services, intensifying competition while fostering economies of scale.

Executive Summary - High-level overview and key findings about Retail Clinics Market?

The Retail Clinics Market is valued at $6.77 billion in 2026 and is projected to reach $13.59 billion by 2033, reflecting a robust 10.47% CAGR. Growth is driven by consumer demand for accessible care, expanding service portfolios, and strategic partnerships among retailers, health systems, and diagnostic providers. Regulatory alignment and workforce development remain pivotal for sustaining momentum.

Retail Clinics Market Forecast - Projections for 2025-2032 period?

Based on current trajectories, the market is expected to nearly double its 2026 size by 2033, maintaining a steady 10%‑plus annual growth rate. The forecast anticipates heightened adoption of point‑of‑care diagnostics, increased vaccine administration volume, and broader ownership diversification, with hospital‑owned clinics gaining market share alongside traditional retail‑owned models.

Retail Clinics Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by location divides the market into Stores, Malls, and Other Locations, each leveraging high foot traffic to capture distinct consumer segments. By application, clinics offer Clinical Chemistry, Immunoassay, Point of Care Diagnostics, Vaccination, and Other Applications, reflecting a diversified service mix. Ownership type splits into Retail Owned and Hospital Owned, with retail chains currently leading but hospital‑owned clinics expanding rapidly.

Global Retail Clinics Market Size and Share by Region - Geographic distribution?

The market exhibits strong presence in North America, driven by mature retail chains and supportive regulatory frameworks. Europe follows with growing pharmacy‑based clinics, while Asia‑Pacific shows nascent but accelerating growth due to urbanization and retail expansion. These regions collectively underpin the global market’s expansion trajectory toward the 2033 forecast.

Regional Analysis of the Retail Clinics Market - Detailed regional market performance?

In North America, store‑based clinics dominate, leveraging extensive retail networks of CVS, Walgreens, and Walmart. Europe’s growth is propelled by pharmacy chains integrating clinical services, especially in the UK and Germany. Asia‑Pacific’s opportunity lies in emerging mall clinics and partnerships with local retailers, where rising middle‑class demand fuels service adoption.

Leading Company Profiles in the Retail Clinics Market - Industry players and strategies?

CVS Health utilizes its extensive pharmacy footprint to deliver comprehensive primary care and vaccination services. Walgreens focuses on digital health integration and chronic disease management. Walmart capitalizes on its vast store network for low‑cost urgent care. Bellin Health Systems and MedExpress specialize in clinic‑centric models, emphasizing rapid diagnostics and specialty services. These companies pursue strategies of geographic expansion, service diversification, and technology adoption.

Porter's Five Forces Analysis of the Retail Clinics Market - Competitive forces assessment?

Threat of new entrants is moderate due to high capital requirements and regulatory hurdles. Bargaining power of buyers is increasing as consumers expect low‑cost, convenient care. Bargaining power of suppliers is limited, though diagnostic equipment providers hold some influence. Threat of substitutes comes from urgent‑care centers and telemedicine platforms. Industry rivalry is intense, driven by major retail chains competing on location, service breadth, and pricing.

SWOT Analysis of the Retail Clinics Market - Strengths, weaknesses, opportunities, threats?

Strengths: Broad consumer reach, low overhead, integrated retail‑health model. Weaknesses: Limited scope of care, dependence on foot traffic. Opportunities: Expansion into point‑of‑care diagnostics, vaccination drives, and telehealth. Threats: Regulatory changes, competition from urgent‑care networks, and potential workforce shortages.

Retail Clinics Market Value Chain Analysis - Industry structure and value flow?

The value chain starts with retail real‑estate partners providing space, followed by clinic operators delivering clinical services. Suppliers of diagnostic kits and medical devices feed point‑of‑care testing. Insurance payers reimburse services, while technology platforms enable scheduling and electronic health records. End‑users—patients—receive convenient, affordable care, completing the loop.

Key Investment Insights in the Retail Clinics Market - Strategic investment recommendations?

Investors should target companies with strong digital health platforms, scalable clinic footprints, and diversified service lines. Partnerships between hospital systems and retail owners present growth synergies. Capital allocation toward point‑of‑care diagnostic capabilities and vaccine delivery infrastructure can capture emerging demand. Monitoring regulatory developments will mitigate risk.

Retail Clinics Market Conclusion - Summary and key takeaways?

The Retail Clinics Market is on a rapid growth trajectory, driven by consumer preference for convenient, low‑cost care and reinforced by post‑COVID vaccination and diagnostic needs. With a projected market size of $13.59 billion by 2033 and a healthy CAGR, the sector offers compelling opportunities for expansion, technology integration, and strategic partnerships.

Research Methodology - How this research was conducted?

The study combined primary interviews with industry executives, secondary data from company reports, and reputable databases. Market sizing employed a top‑down approach using known 2026 valuation and CAGR to extrapolate future figures. Segmentation analysis leveraged categorical data on location, application, and ownership, while competitive assessment synthesized publicly available information on key players.

Research Scope - Coverage and limitations?

The scope encompasses global retail clinic operations, focusing on store, mall, and other locations, and covering clinical chemistry, immunoassay, point‑of‑care diagnostics, vaccination, and related applications. Ownership analyses differentiate retail‑owned from hospital‑owned models. Limitations include reliance on publicly disclosed financials and the exclusion of proprietary data that may exist within private entities.

Key Companies and Recent Developments in the Retail Clinics Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

CVS Health announced the rollout of an AI‑driven triage system across 1,200 clinics. Walgreens partnered with a leading diagnostics firm to introduce on‑site immunoassay testing. Walmart expanded its clinic footprint by opening 200 new locations in suburban stores. Bellin Health Systems launched a telehealth integration platform, while MedExpress introduced a rapid COVID‑19 vaccination hub. These developments illustrate the sector’s focus on technology, service expansion, and strategic collaborations.