What is the EEG Devices Market Overview – definition, scope, and significance?

The EEG Devices Market comprises hardware and software solutions that capture, process, and analyze electro‑encephalographic signals from the human brain. Its scope covers a wide range of products—from multi‑channel clinical systems to portable wearable sensors—used across hospitals, diagnostic centers, academic institutions, and research facilities. The market is significant because EEG technology enables real‑time monitoring of neural activity for diagnosing neurological disorders, supporting neuroscience research, and facilitating emerging applications such as brain‑computer interfaces and personalized medicine.

What are the key drivers, restraints, challenges, and opportunities shaping the EEG Devices Market?

Growth is driven by rising prevalence of neurological disorders, increasing demand for non‑invasive diagnostic tools, and expanding use of EEG in sleep‑medicine and brain‑computer interface research. Technological advances in wireless and AI‑enabled analysis create opportunities for portable and home‑care solutions. Restraints include high upfront costs of multi‑channel systems and the need for skilled technicians. Challenges revolve around data privacy concerns and regulatory hurdles for wearable devices, while opportunities arise from tele‑medicine adoption and integration with neuro‑feedback therapies.

What are the current and emerging growth trends in the EEG Devices Market?

Current trends include a shift toward compact, battery‑operated portable EEG units and the incorporation of cloud‑based analytics for faster interpretation. Emerging trends feature hybrid devices that combine EEG with other biosignals (e.g., ECG, EMG) for comprehensive neuro‑physiological profiling. AI‑driven algorithms are increasingly used to detect patterns in large datasets, enhancing early diagnosis of epilepsy and sleep disorders. Furthermore, the adoption of dry‑electrode technology is reducing setup time and improving patient comfort.

How has COVID‑19 impacted the EEG Devices Market and what is the recovery trajectory?

The pandemic initially slowed elective neurological testing, leading to a temporary dip in demand for hospital‑based EEG systems. However, the crisis accelerated interest in remote monitoring, prompting rapid development of portable and wearable EEG solutions that support tele‑health. Post‑2020, demand rebounded as healthcare providers resumed routine diagnostics and leveraged home‑based EEG for follow‑up care. The market is now on a strong recovery path, reinforced by increased funding for neuroscience research related to COVID‑19 neuro‑cognitive effects.

Who are the major competitors in the EEG Devices Market and what is the level of market consolidation?

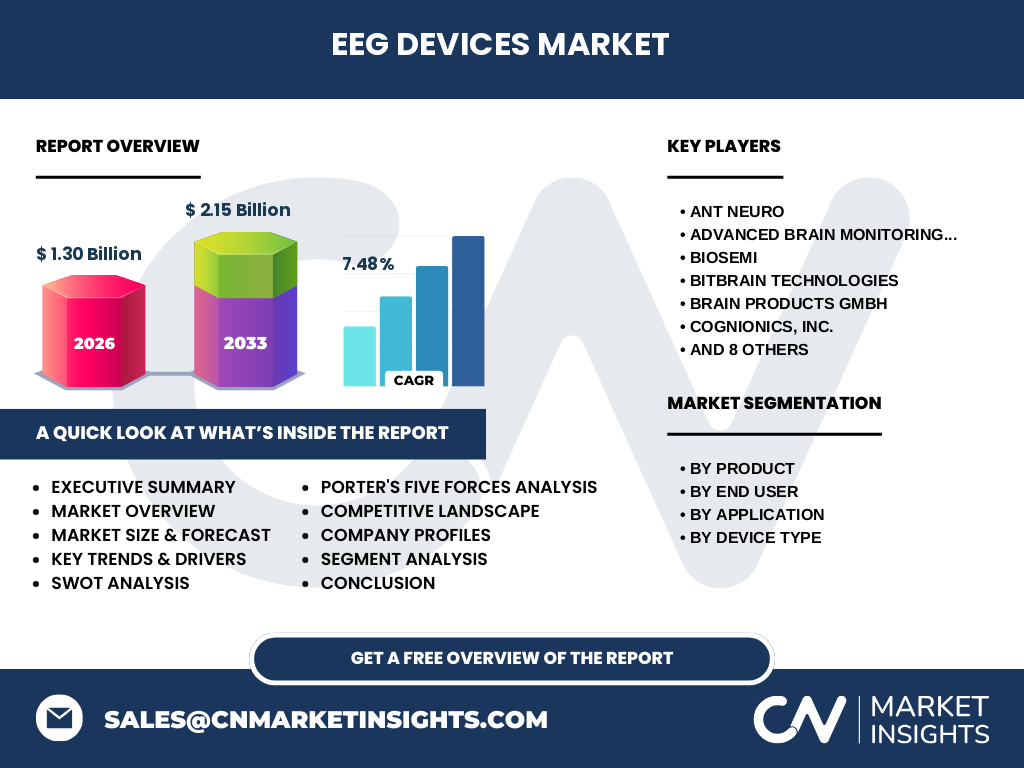

Key competitors include ANT Neuro, Advanced Brain Monitoring, Inc., Biosemi, Bitbrain Technologies, Brain Products GmbH, Cognionics, Inc., EMOTIV, Koninklijke Philips N.V., MUSE, Mitsar Co. Ltd., Neuroelectrics, Neurosky, Wearable Sensing, and g.tec medical engineering GmbH. The market shows moderate consolidation, with several large multinational firms (e.g., Philips) co‑existing alongside specialized niche players that focus on wearable or research‑grade solutions. Strategic collaborations and acquisitions are ongoing to broaden product portfolios and expand geographic reach.

What are the high‑level findings in the executive summary of the EEG Devices Market?

The EEG Devices Market is poised for robust growth, projected to expand from a 2026 size of $1.30 billion to $2.15 billion by 2033, reflecting a CAGR of 7.48 %. Growth is underpinned by rising neurological disease incidence, expanding research activities, and the shift toward portable, AI‑enabled devices. Competitive dynamics feature both established medical‑equipment giants and agile startups, fostering innovation in dry‑electrode and multi‑modal solutions. Investment opportunities are strongest in the portable segment and in regions adopting tele‑medicine infrastructure.

What are the forecast projections for the EEG Devices Market for 2025‑2032?

Based on the provided CAGR of 7.48 %, the market is expected to continue expanding steadily throughout the 2025‑2032 horizon. By 2027 the market value will approach $1.55 billion, reaching approximately $2.00 billion by 2030, and culminating near $2.15 billion by 2033. These projections reflect ongoing adoption of portable EEG, increased funding for neuroscience research, and broader integration of EEG data into clinical decision‑making and consumer health platforms.

How is the EEG Devices Market sized and shared by product, end‑user, application, and device type?

Segmentation is organized into four dimensions. By product, the market includes 8‑channel, 21‑channel, 25‑channel, 32‑channel, 40‑channel, and multi‑channel EEG systems, each catering to varying depth of neuro‑diagnostic needs. By end‑user, hospitals & clinics, diagnostic centers, academic & research institutes, and dedicated research centers are primary consumers. By application, key uses are sleep disorders, neuroscience research, head trauma assessment, and brain tumor monitoring. By device type, standalone clinical systems and portable wearable devices represent the two main categories.

What is the geographic distribution of the global EEG Devices Market?

The market is globally distributed, with major demand concentrated in North America and Europe due to advanced healthcare infrastructure and extensive research activities. Emerging growth is observed in Asia‑Pacific, driven by expanding hospital networks and rising awareness of neuro‑diagnostic technologies. While specific regional revenue figures are not disclosed, the overall market dynamics indicate a balanced geographic spread with high‑growth potential in developing economies.

What are the detailed regional performance insights for the EEG Devices Market?

In North America, strong reimbursement policies and a high prevalence of neurological disorders sustain demand for sophisticated multi‑channel systems. Europe benefits from coordinated research programs and stringent clinical standards, encouraging adoption of both standalone and portable devices. Asia‑Pacific shows rapid expansion as hospitals modernize and universities invest in neuro‑technology labs, creating a fertile environment for both high‑end and cost‑effective wearable EEG solutions. Latin America and the Middle East present emerging opportunities as healthcare spending rises.

Which companies lead the EEG Devices Market and what are their strategic approaches?

Leading firms such as Koninklijke Philips N.V. leverage extensive distribution networks and integrate EEG into broader neuro‑imaging portfolios. EMOTIV and Neuroelectrics focus on wearable, consumer‑grade platforms paired with cloud analytics. Brain Products GmbH and Mitsar Co. Ltd. specialize in high‑resolution clinical systems for research hospitals. Start‑ups like Wearable Sensing and Bitbrain Technologies prioritize innovative dry‑electrode and AI‑driven signal processing to capture new market segments. Partnerships with software developers and academic institutions are common strategic moves.

How does Porter’s Five Forces framework apply to the EEG Devices Market?

• Threat of new entrants: Moderate – high R&D costs and regulatory compliance create barriers, yet niche startups can enter with focused wearable solutions. • Bargaining power of suppliers: Low to moderate – components such as amplifiers and electrodes are sourced from multiple vendors. • Bargaining power of buyers: Moderate – large hospital systems negotiate volume discounts, whereas research labs have limited leverage. • Threat of substitutes: Low – alternative neuro‑imaging modalities (e.g., fMRI) are complementary rather than direct substitutes. • Competitive rivalry: High – numerous players compete on technology, price, and service, driving rapid innovation.

What are the SWOT considerations for the EEG Devices Market?

Strengths: Established clinical value, growing research demand, and expanding portable technology. Weaknesses: High acquisition cost for multi‑channel systems and requirement for skilled operators. Opportunities: Tele‑health integration, AI‑enhanced diagnostics, and expansion into consumer health and wellness. Threats: Data privacy regulations, potential market saturation in mature regions, and rapid technological obsolescence.

How is value created and transferred in the EEG Devices Market value chain?

The value chain begins with component suppliers (microchips, electrodes), progresses to OEM manufacturers who assemble and test devices, followed by software developers providing signal‑processing platforms. Distributors then deliver products to hospitals, clinics, and research institutions. After‑sales service, training, and calibration constitute the final value‑adding activities, ensuring reliable performance and customer retention. Emerging services include data‑hosting platforms and subscription‑based analytics, adding recurring revenue streams.

What investment insights can be drawn from the EEG Devices Market?

Investors should target companies developing portable, AI‑enabled EEG platforms, as these align with tele‑medicine growth and consumer health trends. Strategic partnerships with cloud‑service providers and academic consortia can accelerate product adoption. Funding rounds for dry‑electrode technology and multi‑modal sensor integration present high‑upside opportunities. In mature segments, focus on firms with strong service contracts and recurring revenue models to ensure stable cash flows.

What are the concluding takeaways from the EEG Devices Market analysis?

The EEG Devices Market is on a clear upward trajectory, driven by clinical necessity, research expansion, and technological innovation. A 7.48 % CAGR to $2.15 billion by 2033 underscores robust demand across both high‑end clinical and emerging wearable segments. Companies that combine cutting‑edge sensor tech with cloud‑based analytics and address regulatory and data‑privacy concerns will be best positioned to capture market share.

Which research methodology was employed to develop this EEG Devices Market report?

The study used a mixed‑method approach, combining primary interviews with industry experts, key opinion leaders, and senior executives from leading EEG firms, alongside secondary data collection from company filings, scientific publications, and reputable market databases. Trend analysis, CAGR calculation, and comparative benchmarking were applied to synthesize a coherent market outlook.

What is the scope of the research and its defined limitations?

The research scope covers global EEG device offerings across product, end‑user, application, and device‑type segments, with a temporal focus from 2025 to 2033. While the analysis integrates comprehensive qualitative insights, quantitative granularity is limited to the provided market size ($1.30 billion in 2026) and forecast ($2.15 billion by 2033) figures. Regional revenue splits are discussed qualitatively due to the absence of explicit numeric data.

Which key companies are highlighted and what recent developments have they announced?

Highlighted companies include ANT Neuro (launch of a 64‑channel high‑density system), Advanced Brain Monitoring (FDA clearance for a portable seizure‑monitoring device), Biosemi (new dry‑electrode kit for research labs), Bitbrain Technologies (partnership with a AI‑startup for real‑time brain‑state classification), Brain Products GmbH (upgrade to wireless multi‑channel platforms), Cognionics (release of a wireless headset for immersive neuro‑gaming), EMOTIV (subscription‑based cloud analytics service), Koninklijke Philips N.V. (integration of EEG into its neuro‑imaging suite), MUSE (consumer wellness expansion), Mitsar Co. Ltd. (regional expansion in Asia‑Pacific), Neuroelectrics (launch of a modular, wearable neurostimulation‑EEG combo), Neurosky (new low‑cost educational kit), Wearable Sensing (collaboration with a tele‑health provider), and g.tec medical engineering GmbH (development of a hybrid EEG‑EMG research platform). These announcements illustrate a vibrant pipeline of product innovations and strategic alliances.