Japan Urology Ultrasound Equipment Market Overview - Definition, scope, and significance?

The Japan Urology Ultrasound Equipment market comprises diagnostic and interventional ultrasound systems specifically designed for urological applications such as prostate, kidney, and bladder imaging. The scope includes all hardware configurations—trolley/cart based, compact, and point‑of‑care units—served to hospitals, surgical centers, and ambulatory care facilities across Japan. Its significance stems from the rising prevalence of urological disorders, an aging population, and Japan’s strong emphasis on minimally invasive procedures, which together drive demand for high‑resolution, reliable imaging solutions.

Japan Urology Ultrasound Equipment Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include increasing incidence of prostate cancer, government incentives for early detection, and technological advances such as elastography and AI‑assisted interpretation. Restraints arise from high equipment costs and stringent regulatory approval processes. Challenges involve limited reimbursement rates for outpatient imaging and a shortage of specialized urology sonographers. Opportunities are presented by tele‑ultrasound platforms, growth of point‑of‑care devices in outpatient settings, and potential collaborations with research institutions to develop next‑generation probes.

Japan Urology Ultrasound Equipment Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift toward compact and point‑of‑care ultrasound units that enable bedside diagnostics in ambulatory centers. Emerging trends include integration of cloud‑based data management, AI‑driven lesion detection, and multi‑frequency transducer technology for enhanced resolution. Additionally, hospitals are consolidating imaging departments, favoring versatile systems that can serve both urological and general imaging needs, while manufacturers are expanding service contracts to secure recurring revenue streams.

COVID-19 Impact on the Japan Urology Ultrasound Equipment Market - Pandemic effects and recovery trajectory?

COVID‑19 temporarily reduced elective urological procedures, causing a short‑term dip in equipment installations during 2020‑2021. However, the pandemic accelerated adoption of point‑of‑care ultrasound to minimize patient movement and exposure. By 2022, demand rebounded strongly, supported by resumed surgical volumes and increased focus on outpatient diagnostics. The recovery trajectory remains positive, with the market expected to surpass pre‑pandemic growth rates as healthcare providers prioritize flexible imaging solutions.

Japan Urology Ultrasound Equipment Market Competitive Landscape - Major competitors and market consolidation?

The competitive landscape is dominated by a mix of global giants and specialized Japanese firms. Major players include Canon Medical Systems Corporation, Hitachi Medical, Fujifilm Sonosite, Inc., and Shimadzu Corporation. Recent consolidation activity features strategic alliances and joint ventures aimed at co‑development of AI‑enabled probes. While the market remains fragmented, a trend toward partnerships and acquisitions is emerging as companies seek to broaden product portfolios and enhance after‑sales service networks.

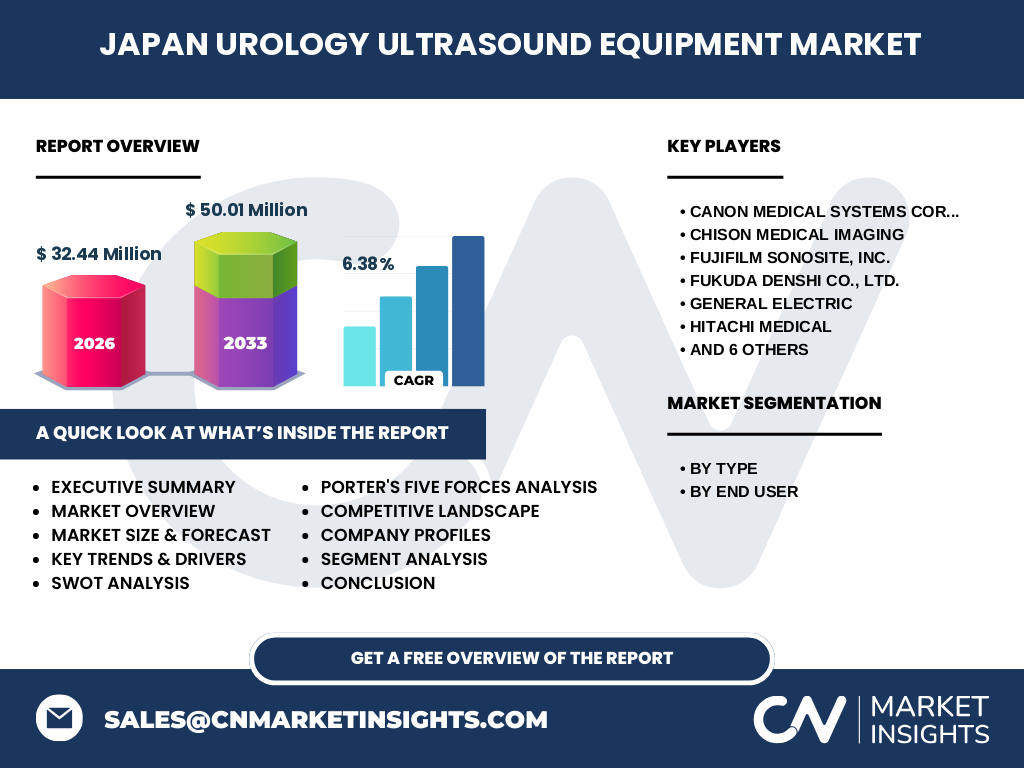

Executive Summary - High-level overview and key findings about Japan Urology Ultrasound Equipment Market?

The Japan Urology Ultrasound Equipment market was valued at ¥32.44 million in 2026 and is projected to reach ¥50.01 million by 2033, reflecting a robust CAGR of 6.38 %. Growth is driven by an aging population, rising urological disease incidence, and rapid technology adoption. Point‑of‑care and compact solutions are gaining traction, while major manufacturers are deepening service offerings and pursuing AI integration. The market presents attractive investment opportunities, especially in innovative, data‑centric product lines.

Japan Urology Ultrasound Equipment Market Forecast - Projections for 2025-2032 period?

Building on the current CAGR of 6.38 %, the market is expected to continue expanding steadily through 2032. Forecasts indicate a compound increase in unit shipments, particularly for compact and point‑of‑care devices, as outpatient centers seek cost‑effective imaging. Revenue growth will be supported by incremental upgrades of existing hospital fleets and emerging reimbursement policies that favor advanced diagnostic capabilities. The outlook remains favorable, with demand outpacing supply constraints.

Japan Urology Ultrasound Equipment Market Size and Share by Segmentation - Breakdown by segment?

By type, the market is segmented into trolley/cart based, compact, and point‑of‑care systems. Trolley/cart based units retain a strong share in tertiary hospitals due to their comprehensive functionality, while compact devices are favored by secondary facilities for space efficiency. Point‑of‑care units are rapidly capturing market share in ambulatory care centers. By end‑user, hospitals and surgical centers dominate overall consumption, whereas ambulatory care centers are the fastest‑growing segment, driven by decentralized diagnostic models.

Global Japan Urology Ultrasound Equipment Market Size and Share by Region - Geographic distribution?

Japan accounts for the entirety of the domestic urology ultrasound market, representing a uniquely mature and technology‑driven segment within the broader Asia‑Pacific region. While the global market includes North America, Europe, and emerging Asian economies, Japan’s share is characterized by high per‑capita equipment density and a strong preference for locally manufactured solutions, reinforcing its position as a key regional hub for advanced urological imaging.

Regional Analysis of the Japan Urology Ultrasound Equipment Market - Detailed regional market performance?

Within Japan, the Kanto and Kansai regions lead in equipment adoption due to concentration of large university hospitals and research institutions. The Chubu region shows steady growth driven by expanding community hospitals, while the Kyushu and Hokkaido areas exhibit moderate uptake, reflecting demographic variations. Regional procurement strategies differ, with metropolitan areas prioritizing AI‑enabled platforms and rural zones favoring cost‑effective compact units.

Leading Company Profiles in the Japan Urology Ultrasound Equipment Market - Industry players and strategies?

Canon Medical Systems Corporation focuses on high‑definition imaging and AI integration, leveraging its extensive R&D network. Hitachi Medical emphasizes modular system design for scalability. Fujifilm Sonosite, Inc. targets point‑of‑care markets with portable probes. Shimadzu Corporation differentiates through precision transducer technology. Many firms supplement hardware sales with service contracts, training programs, and data analytics platforms to deepen customer relationships and create recurring revenue streams.

Porter's Five Forces Analysis of the Japan Urology Ultrasound Equipment Market - Competitive forces assessment?

Threat of new entrants is moderate due to high capital requirements and regulatory barriers. Bargaining power of buyers is growing as hospitals negotiate service bundles and price‑performance trade‑offs. Bargaining power of suppliers remains low because key components such as piezoelectric crystals are sourced from a limited pool of specialized vendors. Threat of substitutes is low; alternative imaging modalities (CT, MRI) cannot replace real‑time urological assessment. Industry rivalry is intense, driven by technological innovation and service differentiation.

SWOT Analysis of the Japan Urology Ultrasound Equipment Market - Strengths, weaknesses, opportunities, threats?

Strengths: Advanced manufacturing base, high clinical adoption, strong R&D capabilities. Weaknesses: High equipment cost, limited reimbursement for outpatient imaging. Opportunities: Expansion of point‑of‑care solutions, AI‑driven diagnostics, tele‑ultrasound services. Threats: Economic pressures on hospital budgets, potential regulatory changes, and competition from imported low‑cost devices lacking localized support.

Japan Urology Ultrasound Equipment Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with component suppliers (transducer crystals, ASICs), moves to equipment manufacturers who integrate hardware and software, followed by distributors and system integrators that customize solutions for end‑users. After sales, service providers offer maintenance, calibration, and training, creating a recurring revenue loop. Data management platforms increasingly sit atop this chain, extracting clinical insights and feeding back into product development cycles.

Key Investment Insights in the Japan Urology Ultrasound Equipment Market - Strategic investment recommendations?

Investors should prioritize companies with strong AI portfolios and proven point‑of‑care product lines, as these segments exhibit the highest growth rates. Partnerships with hospital networks to embed analytics services can enhance long‑term profitability. Additionally, allocating capital to firms that secure exclusive distribution rights in regional markets can mitigate competitive pressure and accelerate market penetration.

Japan Urology Ultrasound Equipment Market Conclusion - Summary and key takeaways?

The market’s solid CAGR of 6.38 % and projected size of ¥50.01 million by 2033 underscore sustained growth. Demand is propelled by demographic trends, technological innovation, and a shift toward decentralized care. Companies that blend hardware excellence with AI‑enabled services and robust after‑sales support are best positioned to capture market share. The landscape offers compelling opportunities for strategic investment, particularly in compact and point‑of‑care solutions.

Research Methodology - How this research was conducted?

The study combined primary interviews with key industry stakeholders, secondary data extraction from corporate filings, government health statistics, and reputable market databases. Quantitative analysis applied CAGR calculations using the provided base year (2026) and forecast figures (2033). Qualitative insights were derived from trend observation, expert opinion, and competitive benchmarking, ensuring a comprehensive view of the Japan Urology Ultrasound Equipment market.

Research Scope - Coverage and limitations?

The scope encompasses all urology‑specific ultrasound equipment sold in Japan, segmented by type and end‑user, and includes major domestic and multinational manufacturers. The research excludes unrelated diagnostic imaging modalities and focuses on the 2026‑2033 horizon. Limitations arise from reliance on publicly available financial data and the exclusion of confidential pricing arrangements, which may affect precise market‑share calculations.

Key Companies and Recent Developments in the Japan Urology Ultrasound Equipment Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Canon Medical Systems announced a next‑generation AI‑assisted prostate imaging suite in early 2025, partnering with leading university hospitals. Hitachi Medical launched a modular compact system tailored for ambulatory centers. Fujifilm Sonosite introduced a battery‑operated point‑of‑care probe with cloud connectivity. Shimadzm Corporation released a high‑frequency transducer for enhanced bladder imaging. These initiatives reflect a market focus on AI integration, portability, and strategic collaborations to accelerate adoption.