What is the Digital Payment Market and why is it significant?

The Digital Payment Market encompasses electronic transactions that replace cash, checks, or manual processes, including mobile wallets, online gateways, QR‑code payments, and blockchain‑based solutions. Its scope covers all industries—from banking and retail to healthcare and travel—leveraging cloud‑based and on‑premises platforms. Significance lies in accelerating commerce, reducing transaction costs, enhancing security, and enabling real‑time financial inclusion worldwide.

What are the main drivers, restraints, challenges, and opportunities shaping the Digital Payment Market?

Key drivers include rising smartphone penetration, consumer demand for contactless experiences, and regulatory support for open banking. Restraints stem from data‑privacy concerns, legacy system integration costs, and fragmented standards across regions. Challenges involve fraud mitigation, interoperability, and the need for robust cybersecurity frameworks. Opportunities arise from emerging technologies such as AI‑powered fraud detection, tokenization, and the expansion of digital payments into underserved rural and emerging markets.

Which growth trends are currently influencing the Digital Payment Market?

Current trends feature the consolidation of payment ecosystems through super‑apps, the shift toward cloud‑native architectures, and the adoption of real‑time payments (RTP) standards. Embedded finance—integrating payment capabilities directly into non‑financial platforms—is gaining traction, as is the rise of decentralized finance (DeFi) solutions that offer peer‑to‑peer transactions without intermediaries. These trends collectively fuel rapid adoption across all industry segments.

How did COVID‑19 impact the Digital Payment Market and what is the recovery trajectory?

The pandemic accelerated digital payment adoption as lockdowns forced consumers and businesses to shift to online and contactless channels. Transaction volumes surged, prompting faster rollout of QR‑code and NFC solutions. Post‑pandemic, the market continues on an upward path, with sustained consumer preference for hygiene‑focused, remote payment methods supporting long‑term growth.

Who are the major competitors in the Digital Payment Market and how is consolidation evolving?

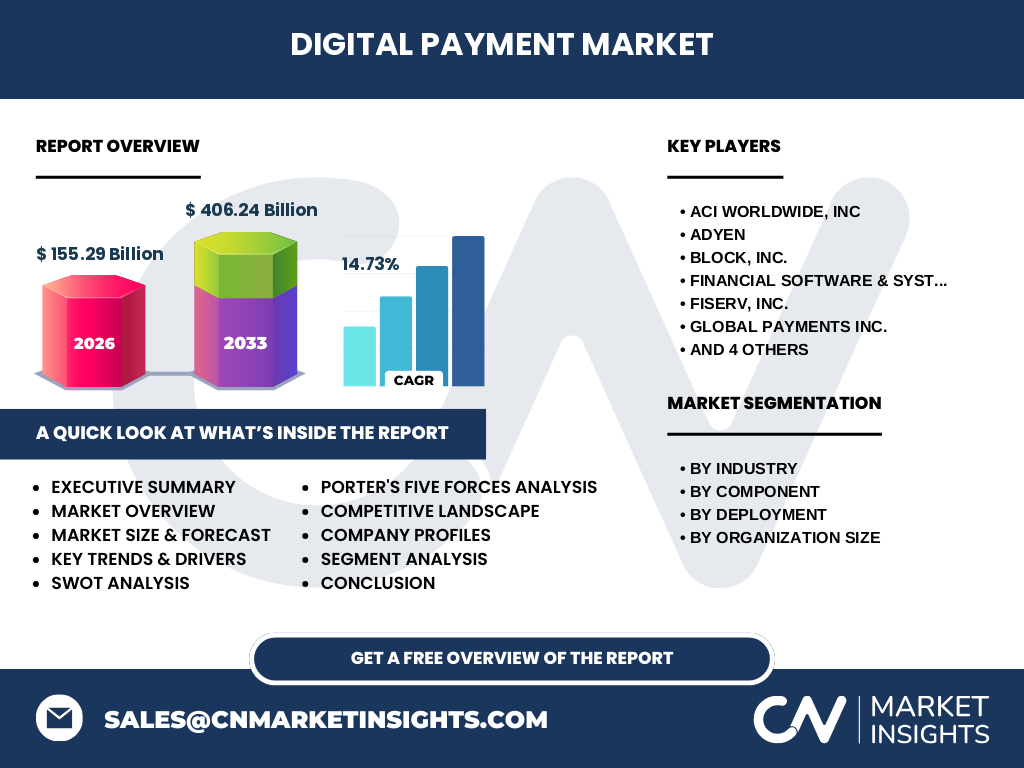

Prominent players include ACI Worldwide, Inc., Adyen, Block, Inc., Financial Software & Systems Pvt. Ltd., Fiserv, Inc., Global Payments Inc., Novatti Group Ltd, PayPal Holdings, Inc., Paysafe Limited, and PayU. The sector is witnessing consolidation through strategic acquisitions—such as larger processors buying niche fintechs—to broaden service portfolios, enhance cross‑border capabilities, and achieve economies of scale.

What are the key findings highlighted in the Executive Summary of the Digital Payment Market?

The market is valued at $155.29 billion in 2026 and is projected to reach $406.24 billion by 2033, delivering a robust CAGR of 14.73 %. Growth is driven by multi‑industry adoption, cloud migration, and regulatory encouragement. Competitive dynamics are intensifying, with innovation focused on AI, tokenization, and embedded finance serving as differentiators.

What are the forecast expectations for the Digital Payment Market from 2025 to 2032?

Based on the given CAGR of 14.73 %, the market is expected to maintain strong expansion through 2032, surpassing the $400 billion mark. Demand from BFSI, retail, and ecommerce will dominate, while emerging segments such as healthcare and travel will contribute incremental growth as digital checkout becomes standard practice.

How is the Digital Payment Market sized and shared by segment?

Segmentation by industry shows BFSI, Retail & Ecommerce, Healthcare, Travel & Hospitality, Media & Entertainment, and IT & Telecom as primary adopters. By component, Solutions and Services represent the core offering. Deployment splits into On‑Premises and Cloud‑Based models, with Cloud gaining momentum. Organization size analysis distinguishes Small and Medium Enterprises from Large Enterprises, each requiring tailored payment stacks.

What is the geographic distribution of the Global Digital Payment Market?

The market’s global footprint reflects diversified adoption across North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa. While specific regional share percentages are not disclosed, all regions demonstrate increasing volumes, with Asia‑Pacific leading in mobile wallet usage and North America driving enterprise‑grade payment solutions.

How does the Digital Payment Market perform in each major region?

In North America, mature banking infrastructure and high fintech investment foster advanced payment gateways. Europe emphasizes regulatory frameworks like PSD2, spurring open‑banking integration. Asia‑Pacific benefits from rapid smartphone growth and government‑backed cash‑less initiatives. Latin America sees rising ecommerce penetration, and the Middle East & Africa are focusing on financial inclusion through mobile money platforms.

Which companies lead the Digital Payment Market and what are their strategies?

Leading firms such as PayPal, Adyen, and Fiserv focus on global reach and platform scalability, investing heavily in AI fraud detection and API ecosystems. Block, Inc. and PayU target small and medium enterprises with affordable, plug‑and‑play solutions. Regional players like Novatti Group and Financial Software & Systems Pvt. Ltd. prioritize localized compliance and partnership models to capture niche markets.

What does Porter’s Five Forces reveal about the Digital Payment Market?

Threat of new entrants is moderate due to high regulatory barriers but lower entry costs for SaaS‑based solutions. Bargaining power of suppliers is low, as technology components are commoditized. Bargaining power of buyers is rising, driven by demand for price‑transparent, feature‑rich platforms. Threat of substitutes remains limited, given the convenience of digital over cash. Competitive rivalry is intense, with both established processors and agile fintech startups vying for market share.

What are the SWOT insights for the Digital Payment Market?

Strengths: strong growth trajectory, broad industry applicability, and supportive regulation. Weaknesses: legacy system dependencies and cybersecurity risks. Opportunities: expansion into underserved regions, embedded finance, and leveraging AI for personalized services. Threats: evolving fraud tactics, data‑privacy legislation, and potential market saturation in mature economies.

How is the Digital Payment Value Chain structured?

The value chain begins with payment initiation (consumer or merchant), proceeds to transaction processing (gateway, acquirer, issuer), includes settlement and clearing, and ends with post‑transaction services such as analytics, loyalty, and dispute management. Cloud service providers and API aggregators increasingly act as enablers, reducing latency and enhancing scalability across the chain.

What investment insights are critical for stakeholders in the Digital Payment Market?

Investors should target companies with scalable cloud architectures, strong API ecosystems, and proven cross‑border capabilities. Funding rounds in AI‑driven fraud prevention and tokenization signal promising returns. Partnerships that extend payment services into non‑financial platforms—like ride‑hailing or ecommerce marketplaces—offer differentiated growth pathways.

What are the main conclusions drawn from the Digital Payment Market analysis?

The market is on a decisive upward swing, underpinned by a 14.73 % CAGR and a projected valuation exceeding $400 billion by 2033. Digital payments are becoming indispensable across all sectors, with cloud adoption and embedded finance shaping the next wave of innovation. Companies that prioritize security, interoperability, and seamless user experiences will capture the most value.

What methodology was employed to conduct this research?

The study combined primary interviews with industry experts, secondary data from corporate filings, market reports, and reputable databases. Trend analysis, CAGR calculation, and competitive benchmarking were applied to derive insights. All figures are aligned with the provided market size of $155.29 billion for 2026 and the forecasted $406.24 billion for 2033.

What is the scope of this research and its limitations?

The scope covers global Digital Payment market dynamics, segmented by industry, component, deployment model, and organization size. Geographic analysis includes all major regions. Limitations arise from the reliance on publicly available data and the exclusion of proprietary financial ratios not disclosed in the provided dataset.

Which key companies have made notable recent developments in the Digital Payment Market?

PayPal launched a new suite of B2B payment APIs, expanding its merchant services. Adyen announced a partnership with a leading Asian telecom to integrate QR‑code payments. Block, Inc. introduced a low‑cost POS system targeting SMBs. Paysafe rolled out tokenized card‑on‑file technology, enhancing security for recurring payments. These developments illustrate a focus on API openness, security, and market expansion.