What is the Smart Container Market Overview – definition, scope, and significance?

The Smart Container market encompasses containers equipped with embedded sensors, communication modules, and analytics software that enable real‑time tracking of location, temperature, humidity, security breaches, and other critical parameters. Its scope covers hardware components (sensors, processors, power units), connectivity technologies (GPS, cellular, LoRaWAN, BLE), and software/services for data aggregation, visualization, and decision support. The significance lies in enhancing supply‑chain visibility, reducing spoilage, preventing theft, and optimizing logistics costs across multiple industries.

What are the Smart Container Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising demand for cold‑chain integrity in food, beverage, and pharmaceuticals, stricter regulatory requirements for traceability, and the digital transformation of logistics. Restraints stem from high upfront investment, integration complexity with legacy systems, and concerns over data privacy. Challenges involve ensuring reliable connectivity in remote routes and standardizing interoperability across vendors. Opportunities arise from growth in e‑commerce, integration of AI‑based predictive analytics, and expansion into emerging sectors such as chemicals and oil & gas.

What are the current Smart Container Market Growth Trends?

Recent trends feature a shift toward edge‑computing within containers to process data locally, reducing latency and bandwidth costs. Adoption of low‑power wide‑area networks (LPWAN) like LoRaWAN is increasing for long‑range, low‑cost connectivity. Suppliers are bundling hardware, software, and managed services into subscription models, driving recurring revenue. Additionally, blockchain is being explored to secure data provenance, while modular sensor kits enable rapid customization for specific verticals.

How has COVID‑19 impacted the Smart Container Market and what is the recovery trajectory?

The pandemic exposed vulnerabilities in cold‑chain logistics, accelerating interest in real‑time monitoring to prevent product loss during lockdown‑induced delays. Initial supply‑chain disruptions slowed new deployments, but the subsequent surge in vaccine distribution and e‑commerce shipments spurred rapid adoption. Recovery is strong, with market confidence rebuilding as manufacturers resume production and logistics providers prioritize resilient, digitized container solutions.

What does the Smart Container Market Competitive Landscape look like?

The market features a mix of established logistics giants and specialist technology firms. Major players such as A.P. Møller‑Mærsk, Hapag‑Lloyd AG, and Orbcomm Inc. leverage extensive shipping networks to embed smart capabilities fleet‑wide. Niche innovators like Ambrosus, Traxens, and Smart Containers Group AG focus on sensor precision and analytics platforms. Recent years have seen strategic partnerships and acquisitions aimed at consolidating technology stacks and expanding global service footprints.

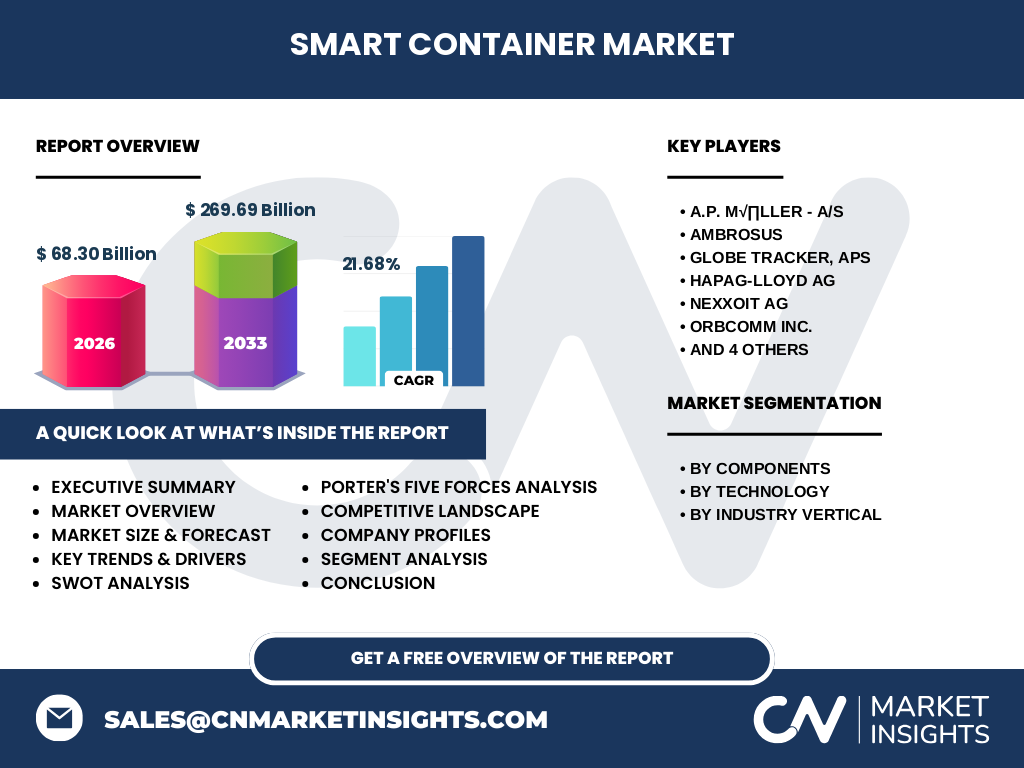

What are the key findings in the Executive Summary of the Smart Container Market?

The Smart Container market is projected to reach $68.30 billion in 2026 and grow to $269.69 billion by 2033, reflecting a robust 21.68 % CAGR. Growth is propelled by regulatory pressure for traceability, the expansion of temperature‑sensitive shipments, and digital logistics initiatives. Hardware, software, and services segments all exhibit strong demand, with GPS and cellular technologies leading connectivity. North America and Europe dominate early adoption, while Asia‑Pacific shows the fastest growth potential.