What is the Wet Pet Food Market Overview – definition, scope, and significance?

The Wet Pet Food Market encompasses all ready‑to‑serve, moisture‑rich food products formulated for companion animals, primarily dogs and cats. It includes products packaged in cans and pouches and distributed through supermarkets, specialized pet shops, and online channels. The market’s significance lies in its role in providing complete nutrition, catering to pet owners seeking convenience, palatability, and health benefits such as improved hydration and digestibility. With a 2026 market size of US 31.59 billion, the sector represents a substantial share of the broader pet‑food industry, reflecting growing pet ownership, humanization trends, and an increasing willingness to spend on premium nutrition.

What are the Wet Pet Food Market drivers, restraints, challenges, and opportunities?

Key drivers include rising disposable income, the human‑pet bond, and demand for functional ingredients (e.g., probiotics, joint‑support compounds). Urban lifestyles boost demand for convenient packaging such as pouches. Restraints stem from higher price points compared with dry food and sensitivities to ingredient sourcing. Challenges involve supply‑chain disruptions for protein and packaging materials, as well as stringent regulatory requirements across regions. Opportunities arise from product innovation (e.g., grain‑free, limited‑ingredient lines), expansion of e‑commerce, and emerging markets where pet ownership is accelerating.

What are the current Wet Pet Food Market growth trends?

Current trends feature a shift toward premium, human‑grade ingredients and transparent labeling. Manufacturers are expanding pouches for on‑the‑go consumption, which aligns with mobile purchasing behavior. There is a notable rise in “limited‑ingredient” and “superfood‑enriched” formulas targeting specific health concerns. Sustainability is influencing packaging choices, prompting the adoption of recyclable cans and biodegradable pouches. Digital marketing and subscription services are also gaining traction, especially in online channels.

How has COVID‑19 impacted the Wet Pet Food Market and what is the recovery trajectory?

The pandemic accelerated online purchasing, pushing many pet owners to buy wet food through e‑commerce platforms due to lockdowns and safety concerns. Supply‑chain bottlenecks initially caused temporary stockouts, but manufacturers adapted by diversifying sourcing and increasing production capacity. Post‑pandemic, the market has retained higher online sales volumes and sees continued growth, supported by sustained pet‑ownership rates and renewed focus on pet health.

What does the Wet Pet Food Market competitive landscape look like?

The competitive landscape is fragmented yet dominated by several multinational and regional players. Major competitors such as Mars, Inc., Nestlé Purina PetCare, Hill’s Pet Nutrition, and Blue Buffalo Co., Ltd. hold significant brand portfolios across dog and cat segments. Consolidation activity includes strategic acquisitions aimed at expanding flavor ranges and channel presence. Smaller innovators like Little BigPaw and FirstMate Pet Foods differentiate through niche formulations and direct‑to‑consumer models.

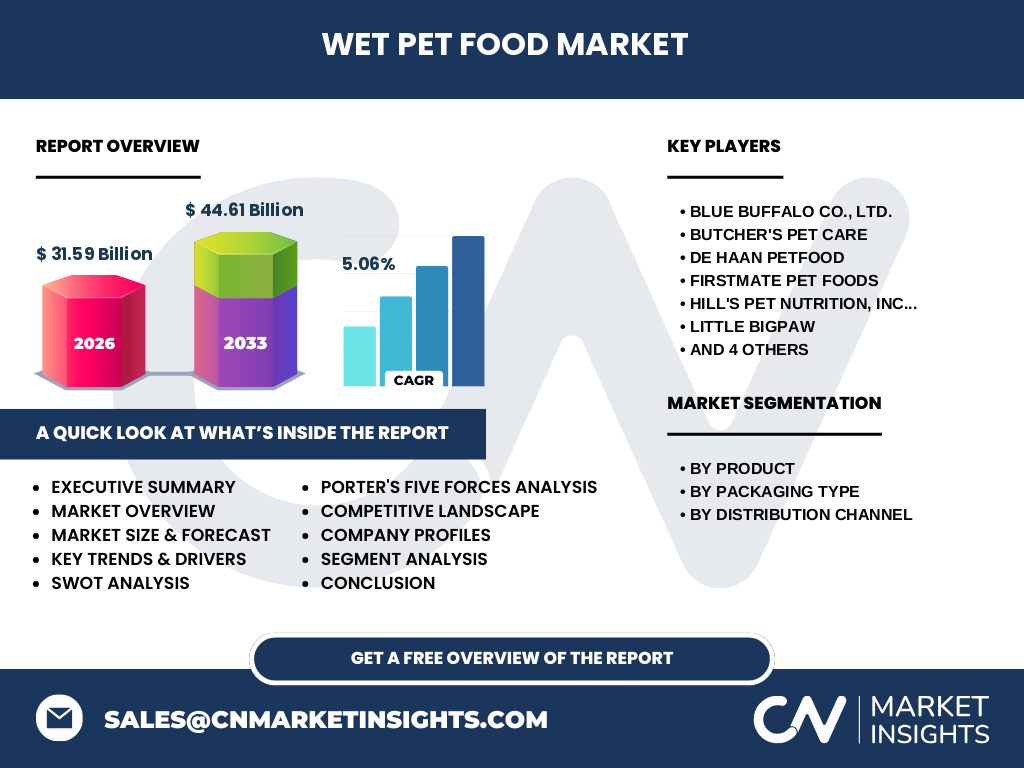

What are the key findings in the Executive Summary of the Wet Pet Food Market?

The Wet Pet Food Market is projected to grow from US 31.59 billion in 2026 to US 44.61 billion by 2033, reflecting a CAGR of 5.06 %. Growth is driven by premiumization, health‑focused product launches, and expanding e‑commerce distribution. Dogs account for the larger product‑type share, while cat products show higher per‑unit price growth. Canned packaging remains dominant, but pouches are the fastest‑growing segment. Regional demand is strongest in North America and Europe, with emerging opportunities in Asia‑Pacific. Competitive rivalry is intensifying as brands race to launch functional, sustainable, and convenient solutions.

What is the Wet Pet Food Market forecast for 2025‑2032?

Based on the provided CAGR of 5.06 %, the market is expected to maintain steady expansion through 2032. The forecasted size of US 44.61 billion for 2033 implies that by 2028 the market will exceed US 35 billion, positioning it well above the 2026 baseline. Growth will be powered by continued premium product introductions, increased penetration of online channels, and geographic expansion into high‑growth regions.

How is the Wet Pet Food Market sized and shared by segmentation?

By product, the market splits between Dog Food and Cat Food, with dog‑focused wet foods representing the larger portion due to higher consumption volumes. By packaging type, Canned products hold the majority share, while Pouches exhibit the highest growth rate, driven by convenience trends. Distribution channels are divided among Supermarkets & Hypermarkets, Specialized Pet Shops, and Online sales, with Online showing the fastest acceleration, reflecting changing shopping habits.

What is the global Wet Pet Food Market size and share by region?

Globally, the market totals US 31.59 billion in 2026. North America and Europe together command the bulk of this value, owing to mature pet‑ownership cultures and high disposable incomes. Asia‑Pacific, while smaller in absolute terms, is growing rapidly as pet adoption rises and urban middle‑class consumers seek premium nutrition. The Americas and Europe together contribute the majority of revenue, while the rest of the world supplies the remaining share.

What does the regional analysis of the Wet Pet Food Market reveal?

North America leads in both volume and value, driven by strong brand loyalty and widespread distribution networks. Europe follows, with a notable focus on sustainable packaging and organic formulations. Asia‑Pacific shows the highest CAGR, propelled by increasing pet ownership in China, India, and Southeast Asia, and a growing acceptance of wet food for cats and dogs. Latin America and the Middle East display modest growth, constrained by lower purchasing power but presenting long‑term potential.

Who are the leading companies in the Wet Pet Food Market and what are their strategies?

Key players include Mars, Incorporated, Nestlé Purina PetCare, Hill’s Pet Nutrition, and Blue Buffalo Co., Ltd. Their strategies revolve around portfolio diversification (adding grain‑free, breed‑specific lines), investment in research and development for functional nutrition, and expansion of direct‑to‑consumer platforms. Companies such as De Haan Petfood and Monge SPA focus on regional strongholds and specialty formulas, while startups like Little BigPaw leverage social media to build niche communities.

How does Porter’s Five Forces analysis apply to the Wet Pet Food Market?

• Threat of new entrants – Moderate; high brand loyalty and capital requirements for production create barriers, yet niche brands can enter via e‑commerce. • Bargaining power of suppliers – Moderate to high; reliance on quality protein sources and specialized packaging increases supplier influence. • Bargaining power of buyers – High; retailers and online platforms demand competitive pricing and product differentiation. • Threat of substitutes – Low to moderate; dry food and fresh‑pet meals are alternatives, but wet food’s unique benefits sustain demand. • Industry rivalry – Intense; leading firms continuously launch new SKUs and pursue promotional activities to capture market share.

What is the SWOT analysis of the Wet Pet Food Market?

Strengths: Strong growth drivers, premium pricing power, high consumer loyalty. Weaknesses: Higher cost relative to dry food, sensitivity to raw material price volatility. Opportunities: Expansion into emerging markets, sustainable packaging innovations, functional ingredient blends. Threats: Regulatory changes, supply‑chain disruptions, competitive pressure from alternative pet‑food formats.

What does the Wet Pet Food Market value chain look like?

The value chain begins with raw‑material sourcing (meat, vegetables, additives), followed by formulation and processing (cooking, sterilization). Next is packaging (canning or pouching) and quality assurance, then distribution through wholesalers to retailers (supermarkets, specialty pet stores) or directly to consumers via online fulfillment centers. After‑sales support includes consumer education, veterinary partnerships, and product feedback loops that inform R&D.

What key investment insights can be drawn for the Wet Pet Food Market?

Investors should target companies with strong e‑commerce capabilities and a pipeline of health‑focused, premium products. Brands that own proprietary ingredients or have sustainable packaging patents are positioned for differentiation. Mergers and acquisitions remain a viable growth path, especially to acquire niche innovators or expand geographic reach. Monitoring regulatory trends around labeling and pet‑food safety will be critical for risk management.

What is the conclusion of the Wet Pet Food Market analysis?

The Wet Pet Food Market is on a robust growth trajectory, projected to reach US 44.61 billion by 2033 with a 5.06 % CAGR. Consumer preferences for convenience, health benefits, and premium quality are the core engines of demand. While price sensitivity and supply‑chain complexities present challenges, innovation in formulation and packaging, coupled with the acceleration of online sales, provide ample opportunity for market participants and investors.

What research methodology was used for this Wet Pet Food Market report?

The research combined primary interviews with industry executives, pet‑nutrition experts, and key retailers, alongside secondary data collection from company filings, market databases, and trade publications. Quantitative analysis applied compound‑annual‑growth calculations using the provided market size and forecast figures. Segmentation and regional breakdowns were derived through triangulation of sales data, distributor reports, and consumer surveys.

What is the scope of the Wet Pet Food Market research?

The scope covers global wet pet‑food products for dogs and cats, segmented by product type, packaging, and distribution channel. Geographic coverage includes North America, Europe, Asia‑Pacific, Latin America, and the Middle East. The study focuses on the period 2026 (base year) through 2033 (forecast horizon) and excludes fresh‑pet meals and raw diets, which are considered separate market categories.

Which key companies and recent developments are highlighted in the Wet Pet Food Market?

Key companies include Blue Buffalo Co., Ltd., Butcher's Pet Care, De Haan Petfood, FirstMate Pet Foods, Hill’s Pet Nutrition, Inc., Little BigPaw, Mars, Incorporated, Monge SPA, Nestlé Purina PetCare, and Petguard Holdings, LLC. Recent developments feature Mars’s launch of a line of grain‑free canned meals, Nestlé Purina’s partnership with a veterinary research institute for probiotic formulations, Hill’s introduction of a senior‑cat pouch series, and Blue Buffalo’s expansion into e‑commerce subscription services. These initiatives illustrate the market’s focus on health‑oriented innovation and digital distribution.