What is the Artichokes Market Overview – definition, scope, and significance?

The Artichokes Market encompasses the global production, processing, and distribution of both globe and elongated artichokes, including organic and conventional varieties. Its scope covers end‑use applications in food processing, direct consumption, and beverages processing. Artichokes are valued for their nutritional profile, culinary versatility, and functional compounds such as antioxidants, making them significant for health‑focused consumers and innovative food manufacturers worldwide.

What are the main drivers, restraints, challenges, and opportunities in the Artichokes Market?

Key drivers include rising consumer awareness of plant‑based nutrition, growing demand for functional ingredients, and expanding gourmet food trends. Restraints stem from seasonality, limited shelf life, and higher production costs for organic cultivars. Challenges involve supply chain fragmentation and competition from alternative vegetables. Opportunities arise from product innovation (e.g., artichoke‑based snacks and beverages), expanding organic certifications, and entry into emerging markets with increasing disposable incomes.

What growth trends are currently shaping the Artichokes Market?

Current trends feature a surge in value‑added artichoke products such as pre‑cooked flours, extracts, and infused beverages. Manufacturers are adopting controlled atmosphere storage to extend freshness, while growers are expanding greenhouse cultivation to mitigate seasonal constraints. Additionally, the rise of plant‑forward restaurant menus is boosting demand for premium, fresh artichoke varieties, especially in urban culinary hubs.

How did COVID‑19 impact the Artichokes Market and what is the recovery trajectory?

The pandemic disrupted logistics and reduced food‑service demand, temporarily lowering sales volumes. However, the shift to home cooking and heightened interest in immune‑supporting foods accelerated direct‑consumption purchases. Recovery has been robust, with the market regaining momentum in 2022 and proceeding on a growth path supported by renewed food‑service activity and continued home‑cooking trends.

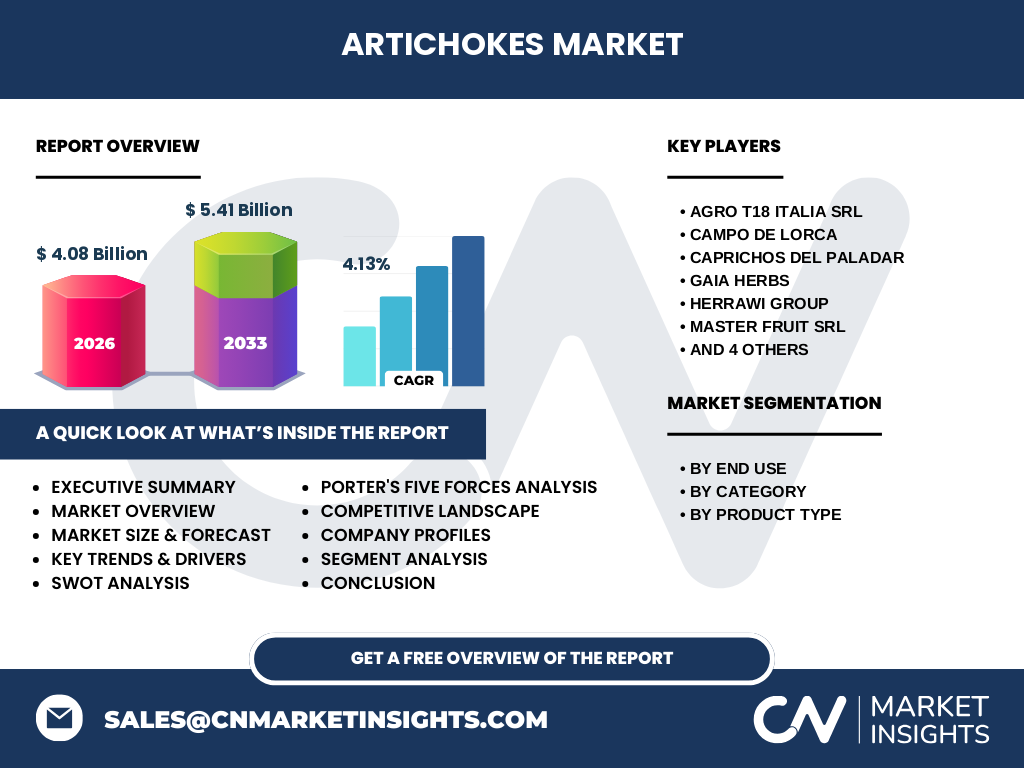

Who are the major competitors in the Artichokes Market and what is the level of market consolidation?

Key competitors include Agro T18 Italia Srl, Campo de Lorca, Caprichos del Paladar, Gaia Herbs, Herrawi Group, Master Fruit Srl, Ocean Mist, Ole, Societa Semplice Agricola F.lli Piras, and The Sa Marigosa Op. The market exhibits moderate consolidation, with several vertically integrated firms controlling cultivation, processing, and distribution, while smaller niche players focus on organic and specialty segments.

What are the high‑level insights presented in the Executive Summary?

The Executive Summary highlights a market size of USD 4.08 billion in 2026, projected to reach USD 5.41 billion by 2033, reflecting a CAGR of 4.13 %. Growth is driven by health‑centric consumer trends, product innovation, and expanding applications across food and beverage sectors. Competitive dynamics are shaped by a mix of large integrated firms and specialty growers, while opportunities lie in organic expansion and value‑added processing.

What are the forecast expectations for the Artichokes Market from 2025 to 2032?

Based on the provided CAGR of 4.13 %, the market is expected to continue expanding steadily through 2032. Year‑over‑year growth will be supported by increasing demand for functional ingredients, broader geographic penetration, and ongoing product diversification. The forecast underscores a resilient trajectory despite macro‑economic fluctuations.

How is the Artichokes Market sized and shared by segmentation?

Segmentation by end use shows three primary categories: Food Processing, Direct Consumption, and Beverages Processing. By category, the market splits into Organic and Conventional artichokes. Product‑type segmentation distinguishes Globe Artichokes from Elongated Artichokes. Each segment contributes to the overall market value, with food processing and direct consumption representing the largest demand drivers, while organic products capture premium pricing opportunities.

What is the geographic distribution of the Global Artichokes Market size and share by region?

The market is globally distributed, with significant activity in traditional Mediterranean producing regions and growing presence in North America and Asia‑Pacific. While exact regional shares are not disclosed, the overall market size of USD 4.08 billion reflects contributions from these key areas, underpinned by established cultivation zones and emerging import markets.

What detailed performance does each region exhibit in the Artichokes Market?

Europe remains a core production hub, benefitting from climate suitability and culinary heritage. North America shows strong growth in direct‑consumption and food‑processing applications, driven by health‑focused consumer segments. Asia‑Pacific is an emerging market, with increasing import volumes as local cuisines adopt Mediterranean ingredients. Latin America and the Middle East present niche opportunities linked to gourmet restaurant expansion.

What are the leading company profiles and their strategic approaches in the Artichokes Market?

Agro T18 Italia Srl focuses on integrated greenhouse cultivation and export logistics. Campo de Lorca leverages sustainable farming practices to supply organic artichokes. Caprichos del Paladar emphasizes premium branding for direct‑consumer sales. Gaia Herbs develops functional extracts for nutraceutical markets. Herrawi Group and Master Fruit Srl invest in processing technology to create value‑added products. Ocean Mist and Ole target beverage‑processing niches, while Societa Semplice Agricola F.lli Piras and The Sa Marigosa Op concentrate on regional specialty varieties.

How does Porter’s Five Forces framework assess the Artichokes Market?

Threat of new entrants is moderate due to capital requirements for cultivation and processing. Bargaining power of suppliers is low, as growers can source inputs relatively easily. Bargaining power of buyers is moderate; large food processors negotiate volume discounts, while niche customers seek premium quality. Threat of substitutes is moderate, with other vegetables offering similar culinary uses. Industry rivalry is fairly intense, driven by product differentiation and price competition among established players.

What are the SWOT analysis findings for the Artichokes Market?

Strengths: Nutritional benefits, growing health consciousness, and versatile applications.

Weaknesses: Seasonality, perishability, and higher cost of organic production.

Opportunities: Expansion into functional foods, organic segment growth, and value‑added processing.

Threats: Climate variability, supply chain disruptions, and competition from alternative vegetables.

What does the Artichokes Market value chain look like?

The value chain starts with seed selection and cultivation (including greenhouse and open‑field methods), proceeds to harvesting and primary processing (sorting, cleaning, packaging), then to secondary processing (canning, freezing, extracting). Distribution channels include wholesale to food manufacturers, retail chains for direct consumption, and specialty distributors for beverage processors. Supporting services such as logistics, quality certification, and marketing complete the chain.

What key investment insights can be drawn for the Artichokes Market?

Investors should target companies with strong processing capabilities and diversified product portfolios, especially those advancing organic certifications. Funding greenhouse expansion can mitigate seasonality risks, while investing in innovative packaging and shelf‑life technologies offers competitive advantages. Partnerships with food‑service chains and nutraceutical firms can accelerate revenue growth in high‑margin segments.

What are the main conclusions of the Artichokes Market report?

The Artichokes Market demonstrates steady growth driven by health trends, product innovation, and expanding applications. With a projected market size of USD 5.41 billion by 2033, the sector offers attractive opportunities for both established players and new entrants, particularly in organic cultivation and value‑added processing. Strategic focus on supply‑chain resilience and geographic diversification will be critical for sustained success.

How was the research methodology designed for this Artichokes Market analysis?

The methodology combined primary interviews with industry experts, secondary data extraction from trade publications, company reports, and governmental statistics, followed by triangulation to ensure accuracy. Quantitative modeling applied the provided CAGR of 4.13 % to forecast future market size, while qualitative assessments informed the driver, restraint, and competitive analyses.

What is the scope of the research and any limitations?

The research covers global production, processing, and consumption of globe and elongated artichokes across organic and conventional categories, focusing on food processing, direct consumption, and beverages processing end uses. Limitations include the absence of granular regional share percentages and unavailability of detailed cost structures, which are addressed through broader trend analysis.

Which key companies are highlighted and what recent developments have they announced?

Agro T18 Italia Srl recently launched a climate‑controlled greenhouse facility to increase year‑round output. Campo de Lorca obtained EU organic certification for its new farm line. Caprichos del Paladar introduced a premium ready‑to‑eat artichoke platter for retail. Gaia Herbs expanded its artichoke extract line into nutraceutical capsules. Herrawi Group announced a joint venture for frozen artichoke products, while Master Fruit Srl invested in advanced canning technology. Ocean Mist unveiled an artichoke‑infused beverage pilot, and Ole began sourcing from sustainable farms in Southern Europe. Societa Semplice Agricola F.lli Piras released a limited‑edition heirloom variety, and The Sa Marigosa Op entered a strategic partnership with a major grocery chain for organic supply.