What is the definition, scope, and significance of the POS Software Market?

The POS (Point‑of‑Sale) Software Market comprises solutions that enable businesses to process transactions, manage inventory, generate sales reports, and engage customers at the point of purchase. Its scope spans multiple industries—including BFSI, hospitality, media and entertainment, and retail—and covers both software licences and related services delivered via on‑premise or cloud deployments. The market is significant because it drives operational efficiency, enhances customer experience, and provides critical data analytics that support strategic decision‑making across the commerce ecosystem.

What are the main drivers, restraints, challenges, and opportunities influencing the POS Software Market?

Key drivers include the growing need for integrated omnichannel experiences, rising adoption of cloud‑based solutions, and increasing regulatory compliance requirements in retail and financial services. Restraints arise from high initial implementation costs for legacy firms and data security concerns. Challenges involve fragmented technology standards and the rapid pace of innovation that can outpace vendor roadmaps. Opportunities lie in AI‑enhanced analytics, contactless payment integration, and expansion into emerging markets where digital transaction infrastructures are still developing.

Which current and emerging trends are shaping the POS Software Market?

Current trends feature a shift toward cloud‑native POS platforms, the incorporation of mobile devices as transaction terminals, and the use of real‑time inventory tracking. Emerging trends include AI‑driven sales forecasting, voice‑activated ordering, and deeper integration with loyalty and CRM systems to boost customer engagement. Additionally, the rise of decentralized payment networks and cryptocurrency acceptance is beginning to influence product roadmaps for forward‑looking vendors.

How has COVID‑19 impacted the POS Software Market and what is the recovery trajectory?

The pandemic accelerated the adoption of contactless and mobile POS solutions as merchants sought to minimize physical touchpoints. Many retailers and hospitality operators migrated to cloud‑based platforms to enable remote management and rapid scaling. While short‑term revenue dips were observed in sectors like brick‑and‑mortgage retail, the market quickly rebounded, driven by pent‑up consumer demand and the digital transformation initiatives sparked by COVID‑19. The recovery trajectory remains positive, with sustained investment in resilient, omnichannel POS ecosystems.

Who are the major competitors in the POS Software Market and what is the state of market consolidation?

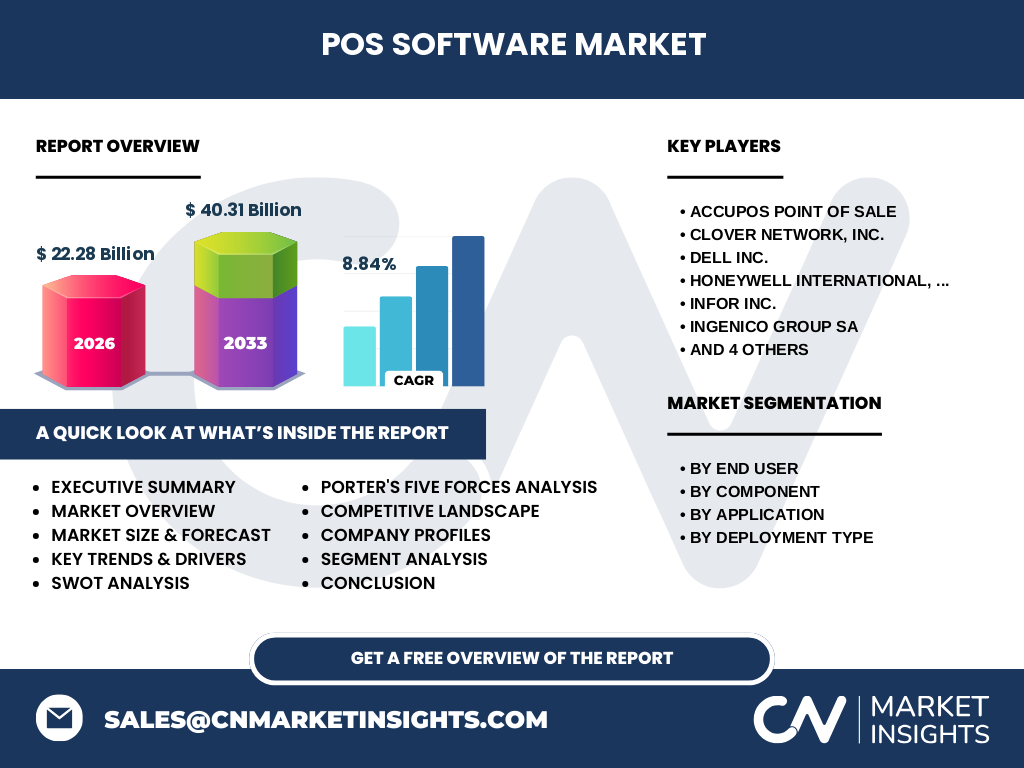

Leading competitors include AccuPOS Point of Sale, Clover Network, Inc., Dell Inc., Honeywell International, Inc., Infor Inc., Ingenico Group SA, Intuit, Inc., LightSpeed POS Inc., ShopKeep, and Vend Limited. The market exhibits moderate consolidation, as large technology firms acquire niche players to broaden functionality and geographic reach. Strategic alliances and OEM partnerships are common, enabling vendors to offer bundled hardware‑software solutions and accelerate entry into new verticals.

What are the high‑level findings and key takeaways from the Executive Summary?

The POS Software Market is poised for robust growth, underpinned by an 8.84% CAGR and an expansion from a $22.28 billion valuation in 2026 to $40.31 billion by 2033. Cloud deployment models are gaining market share, while demand from retail and hospitality remains the strongest. Competitive dynamics are driven by innovation in AI, analytics, and omnichannel integration. Opportunities abound for vendors that can deliver secure, scalable, and data‑rich solutions across diverse end‑user segments.

What are the forecast expectations for the POS Software Market from 2025 to 2032?

Based on current trajectories, the market is expected to continue its upward momentum, reaching the projected $40.31 billion mark by 2033. Growth will be fueled by expanding cloud adoption, enhanced regulatory compliance tools, and increased investment in AI‑enabled decision support. Geographic expansion into emerging economies will contribute additional volume, while mature markets will focus on upgrading legacy systems to more flexible, subscription‑based models.

How is the POS Software Market sized and shared by segmentation?

Segmentation by end‑user shows four primary verticals: BFSI, hospitality, media and entertainment, and retail, each leveraging POS capabilities for transaction processing and customer insights. By component, the market is divided into software licences and associated services, reflecting ongoing revenue from implementation, support, and upgrades. Application‑level segmentation includes inventory tracking, purchasing management, sales reporting, and customer engagement, highlighting the functional breadth of modern POS suites. Deployment segmentation distinguishes on‑premise installations from cloud‑hosted solutions, with cloud growing faster due to scalability and lower total cost of ownership.

What is the global POS Software Market size and share by region?

While specific regional dollar values are not disclosed, the market exhibits a worldwide footprint with notable activity in North America, Europe, APAC, and Latin America. North America leads in early cloud adoption and enterprise‑grade deployments, whereas APAC demonstrates rapid growth driven by expanding retail networks and increasing smartphone penetration. Europe maintains steady demand through regulatory‑driven upgrades, and Latin America shows emerging opportunities as merchants modernize payment infrastructures.

What are the detailed regional performance insights for the POS Software Market?

In North America, strong financial services integration and a mature hospitality sector drive robust POS software implementations. Europe benefits from harmonized payment standards and a focus on data privacy, prompting upgrades to secure cloud platforms. APAC’s growth is propelled by a surge in e‑commerce, mobile commerce, and government initiatives supporting digital payments. Latin America experiences incremental adoption as businesses transition from cash‑centric operations to digital transaction processing.

Which leading companies are shaping the POS Software Market and what strategies are they employing?

AccuPOS Point of Sale emphasizes customizable hardware bundles, while Clover Network expands its ecosystem through third‑party app marketplaces. Dell leverages its enterprise infrastructure expertise to offer integrated solutions for large retailers. Honeywell focuses on hardware‑software convergence for high‑traffic environments. Infor adopts industry‑specific suites, and Ingenico strengthens its position via payment gateway integrations. Intuit targets small‑business owners with easy‑to‑use cloud POS, LightSpeed pursues upscale retail experiences, ShopKeep caters to independent merchants, and Vend Limited drives omnichannel capabilities through SaaS models.

How does Porter’s Five Forces framework apply to the POS Software Market?

Threat of new entrants is moderate, as substantial development costs and regulatory compliance act as barriers. Bargaining power of buyers is high, given the availability of multiple vendors and the ease of switching to cloud alternatives. Supplier power is low to moderate because most components (cloud infrastructure, APIs) are commoditized. The threat of substitutes is low, as POS software uniquely combines transaction processing with analytics and inventory control. Competitive rivalry is intense, driven by rapid innovation cycles and the pursuit of differentiated features.

What are the SWOT strengths, weaknesses, opportunities, and threats for the POS Software Market?

Strengths include high demand for integrated commerce solutions and strong recurring revenue models. Weaknesses involve legacy system migration challenges and sensitivity to data security breaches. Opportunities arise from AI‑driven personalization, expansion into underserved regions, and the growing importance of contactless payments. Threats encompass evolving cybersecurity regulations, potential market saturation in mature economies, and disruptive technologies such as blockchain‑based payment platforms.

How is the value chain of the POS Software Market structured?

The value chain begins with core software development and platform engineering, followed by integration services that tailor solutions to specific industry workflows. Next are distribution channels—direct sales, OEM partnerships, and cloud marketplaces—that deliver the product to end users. Post‑sale, the chain includes implementation consulting, training, and ongoing support services, which generate recurring revenue and foster customer loyalty. Data analytics and insights derived from POS usage feed back into product enhancement cycles.

What key investment insights can be drawn from the POS Software Market?

Investors should target companies with strong cloud migration roadmaps and robust API ecosystems, as these are positioned to capture the fastest‑growing segment. Firms that have secured strategic partnerships with payment processors or hardware manufacturers can leverage cross‑selling opportunities. Additionally, businesses investing in AI and advanced analytics capabilities are likely to command premium valuations due to differentiated value propositions for enterprise customers.

What are the concluding remarks and primary takeaways for the POS Software Market?

The POS Software Market is on a clear growth trajectory, underpinned by an 8.84% CAGR and a projected rise to $40.31 billion by 2033. Cloud adoption, AI integration, and omnichannel functionality are the central pillars of future expansion. Competitive pressures will intensify, rewarding firms that can deliver secure, scalable, and data‑rich platforms. Stakeholders should monitor regulatory developments and emerging payment technologies to stay ahead of market shifts.

Which research methodology was used to create this report?

The study employed a mixed‑method approach, combining primary interviews with industry executives, secondary data extraction from reputable market databases, and quantitative modeling to project future volumes. Trend analysis, competitive benchmarking, and scenario planning were applied to validate assumptions. All financial figures—$22.28 billion (2026), $40.31 billion (forecast), and an 8.84% CAGR—derive from the supplied data set.

What is the scope of this research and its coverage limitations?

The scope encompasses global POS software offerings across all major verticals, focusing on component, application, deployment, and end‑user segmentation. Geographic analysis includes the primary regions of North America, Europe, APAC, and Latin America. Limitations stem from the reliance on publicly available information and the exclusion of proprietary financial details beyond the supplied market size and growth metrics.

Which key companies and recent developments are noteworthy in the POS Software Market?

Notable players include AccuPOS Point of Sale, Clover Network, Dell Inc., Honeywell International, Infor Inc., Ingenico Group SA, Intuit, LightSpeed POS, ShopKeep, and Vend Limited. Recent developments feature Honeywell’s launch of rugged, contactless terminals for high‑traffic retail, Clover’s expansion of its app marketplace to include AI‑driven loyalty tools, and Intuit’s integration of advanced tax compliance modules into its cloud POS suite. These initiatives illustrate the market’s focus on innovation, security, and ecosystem expansion.