What is the India PVC Pipes Market Overview – Definition, scope, and significance?

The India PVC Pipes market comprises the manufacturing, distribution, and application of polyvinyl chloride (PVC) piping solutions across residential, commercial, and industrial sectors. PVC pipes are valued for their durability, corrosion resistance, lightweight nature, and cost‑effectiveness, making them a cornerstone in water supply, irrigation, sewerage, plumbing, and HVAC infrastructure. The market’s scope extends from raw material processing (PVC resin, stabilizers, plasticizers, lubricants, pigment base) to finished pipe products in chlorinated, plasticized, and unplasticized varieties. Its significance lies in supporting India’s rapid urbanization, government‑driven sanitation initiatives, and agricultural water‑management programs.

What are the India PVC Pipes Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include expanding urban housing projects, government schemes such as Swachh Bharat Mission, and rising demand for efficient irrigation systems. The low maintenance cost of PVC versus metal or concrete alternatives further fuels adoption. Restraints stem from fluctuating raw‑material prices, especially PVC resin, and regulatory scrutiny over plastic waste. Challenges involve competition from alternative polymers and the need for skilled installation labor. Opportunities arise in developing high‑performance, eco‑friendly pipe grades, leveraging prefabricated construction methods, and tapping into Tier‑II and Tier‑III city expansions.

What are the India PVC Pipes Market Growth Trends?

Current trends show a shift toward unplasticized PVC (uPVC) for water supply due to its superior rigidity and lifespan. Manufacturers are integrating additives to improve fire resistance and UV stability, catering to HVAC and outdoor applications. Smart city initiatives are prompting the use of PVC conduit systems for integrated utility networks. Additionally, there is a growing preference for locally sourced PVC resin to reduce dependence on imports, aligning with the “Make in India” agenda.

How has COVID-19 impacted the India PVC Pipes Market and what is the recovery trajectory?

The pandemic caused temporary disruptions in supply chains for PVC resin and ancillary chemicals, leading to short‑term project delays. However, post‑lockdown stimulus focused on infrastructure revitalization accelerated demand for water and sanitation projects, offsetting initial setbacks. Recovery has been steady, with construction activities resuming and government spending on rural water supply programs boosting pipe sales. The market is now on a clear growth path, reflected in the projected CAGR of 3.93%.

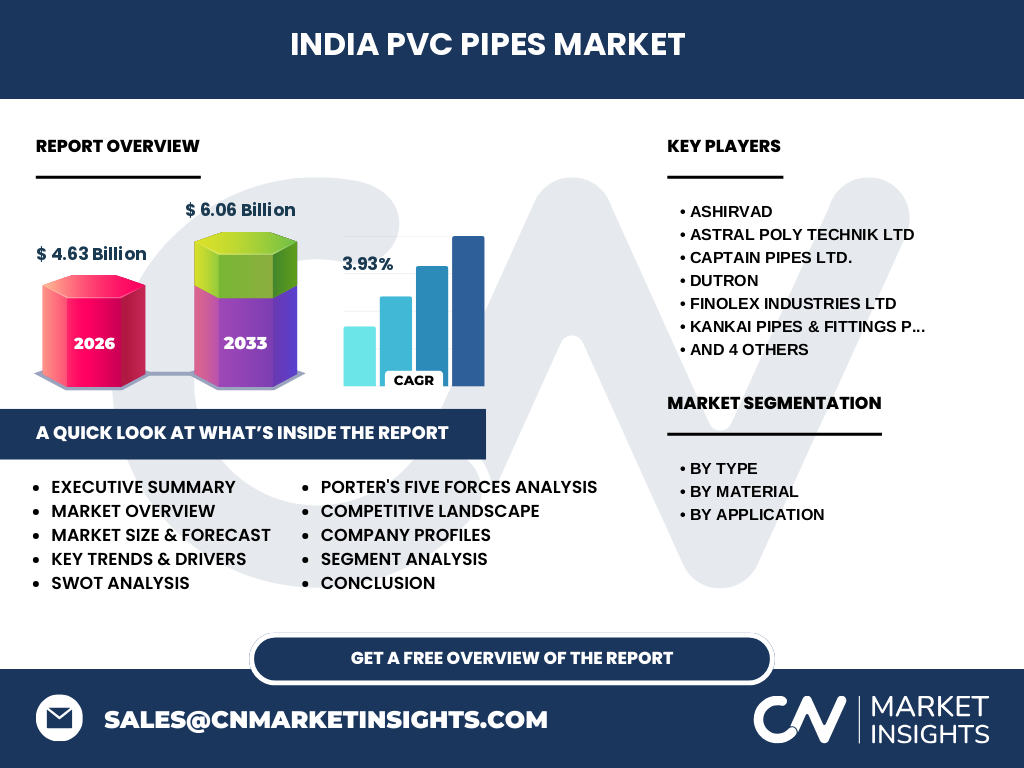

What does the India PVC Pipes Market Competitive Landscape look like?

The market is moderately consolidated, featuring a mix of large integrated players and specialized manufacturers. Major competitors such as Ashirvad, Astral Poly Technik Ltd, Finolex Industries Ltd, and Prince Pipes and Fittings Ltd dominate through extensive distribution networks and diversified product portfolios. Recent consolidation activity includes strategic alliances and capacity expansions to meet rising demand. Smaller firms like Dutron, Kankai Pipes & Fittings, Ori‑Plast, Supreme, and Utkarsh India focus on niche segments or regional dominance, fostering a competitive yet collaborative environment.

What are the key findings in the Executive Summary?

The India PVC Pipes market is valued at $4.63 billion in 2026 and is forecast to reach $6.06 billion by 2033, growing at a 3.93% CAGR. Growth is driven by urban infrastructure development, government sanitation initiatives, and increasing irrigation needs. While raw‑material price volatility presents a restraint, innovation in eco‑friendly pipe formulations and expansion into underserved regions provide strong upside potential. Leading players are investing in capacity, product diversification, and strategic partnerships to capture market share.

What is the India PVC Pipes Market forecast for 2025‑2032?

Based on the provided data, the market is expected to maintain a steady compound annual growth rate of 3.93% from 2027 through 2033, expanding from the 2026 base of $4.63 billion to an estimated $6.06 billion by 2033. This trajectory suggests consistent demand across all application segments, with particular acceleration in irrigation and water‑supply projects driven by government investments and climate‑resilient agriculture policies.

How is the India PVC Pipes Market sized and shared by segmentation?

Segmentation by type includes chlorinated, plasticized, and unplasticized PVC pipes, each catering to distinct performance requirements. By material, the market comprises PVC resin, stabilizers, plasticizers, lubricants, and pigment base, reflecting the value‑added stages of production. Application‑wise, the market is split among irrigation, water supply, sewerage, plumbing, and HVAC systems. While exact numeric shares are not disclosed, unplasticized pipes command a leading position in water supply, whereas plasticized variants see higher usage in HVAC and flexible plumbing networks.

What is the Global India PVC Pipes Market size and share by region?

Globally, India represents a significant segment of the PVC pipe industry due to its large construction and agricultural sectors. The market’s regional distribution is driven primarily by domestic demand, with the majority of revenue generated within the Indian subcontinent. Internationally, export opportunities exist but are comparatively modest, positioning India as a net consumer rather than a major exporter of PVC pipe products.

What does the Regional Analysis of the India PVC Pipes Market reveal?

North India leads in pipe consumption, fueled by extensive urban projects in Delhi, Uttar Pradesh, and Haryana. Western regions, particularly Maharashtra and Gujarat, exhibit strong demand from industrial and infrastructure developments. South India shows robust growth in irrigation and residential plumbing, while the East and Northeast are emerging markets with increasing government‑funded water‑supply schemes. Regional variations in climate and agricultural practices influence the relative importance of irrigation versus sewerage applications.

Who are the leading company profiles in the India PVC Pipes Market?

Ashirvad specializes in uPVC pipe systems for water supply and has expanded its manufacturing footprint across several states. Astral Poly Technik Ltd offers a broad range of chlorinated and unplasticized pipes, emphasizing R&D for fire‑resistant grades. Finolex Industries Ltd combines pipe production with a strong brand presence in plumbing fittings. Prince Pipes and Fittings Ltd. focuses on integrated solutions for HVAC and industrial applications. Other notable players—Captain Pipes, Dutron, Kankai Pipes & Fittings, Ori‑Plast, Supreme, and Utkarsh India—provide regionally tailored products and maintain agile supply chains.

How does Porter’s Five Forces analysis apply to the India PVC Pipes Market?

Threat of new entrants is moderate; capital investment for extrusion lines is significant, but the growing market attracts new manufacturers. Bargaining power of suppliers is relatively high due to limited sources of PVC resin and additives, influencing raw‑material costs. Bargaining power of buyers is moderate; large construction firms and government agencies can negotiate volume discounts. Threat of substitutes is low to moderate, as alternatives like HDPE or ductile iron serve specific niches but lack PVC’s versatility. Industry rivalry is intense, with established players competing on price, quality, and distribution reach.

What are the SWOT insights for the India PVC Pipes Market?

Strengths: Cost‑effective material, corrosion resistance, extensive application range. Weaknesses: Dependency on volatile PVC resin prices, environmental concerns over plastic waste. Opportunities: Development of recyclable pipe grades, expansion into rural infrastructure, adoption of smart‑city conduit solutions. Threats: Regulatory tightening on plastic usage, competition from alternative piping materials, economic slowdown affecting construction spending.

How does the India PVC Pipes Market value chain function?

The value chain begins with raw‑material extraction and production of PVC resin, stabilizers, plasticizers, lubricants, and pigments. These inputs are supplied to pipe manufacturers who perform extrusion, calendaring, and chlorination processes to create chlorinated, plasticized, or unplasticized pipes. Finished products are then distributed through wholesale dealers, retailers, and direct sales to construction firms, municipal bodies, and agricultural cooperatives. After‑sales services, including installation support and warranty handling, complete the chain, while recycling firms address end‑of‑life pipe recovery.

What key investment insights can be drawn for the India PVC Pipes Market?

Investors should consider capacity expansion in regions with high urban growth, such as the Delhi‑NCR and Maharashtra corridors. Funding R&D for eco‑friendly and fire‑resistant PVC formulations can capture premium segments. Strategic partnerships with government bodies for water‑sanitation projects provide stable, long‑term revenue streams. Diversifying supply sources for PVC resin can mitigate price risk, while acquisition of niche regional players can accelerate market penetration.

What is the conclusion of the India PVC Pipes Market analysis?

The India PVC Pipes market is on a robust growth trajectory, underpinned by infrastructure development, agricultural water‑management needs, and supportive government policies. Despite raw‑material price sensitivity and environmental challenges, the sector offers ample opportunities for innovation, geographic expansion, and strategic investment. Leading firms are well‑positioned to benefit from sustained demand, making the market an attractive prospect for stakeholders seeking long‑term value.

What research methodology was used for this study?

The research combined primary interviews with industry experts, manufacturers, and distributors, alongside secondary data collection from company reports, government publications, and reputable market databases. Trend analysis, CAGR calculation, and Porter’s Five Forces were applied to assess competitiveness. Segmentation was derived from product specifications and application categories, ensuring a comprehensive view of the market dynamics.

What is the scope of this research?

The scope encompasses the Indian PVC pipe ecosystem, covering all pipe types (chlorinated, plasticized, unplasticized), material inputs, and end‑use applications (irrigation, water supply, sewerage, plumbing, HVAC). Geographic focus is nationwide, with regional breakdowns for major growth zones. The study excludes unrelated plastic products and does not quantify export‑import balances beyond the domestic consumption narrative.

Who are the key companies and what recent developments have they announced?

Ashirvad launched a new line of high‑pressure uPVC pipes for municipal water projects. Astral Poly Technik Ltd announced a joint venture with a European stabilizer supplier to enhance fire‑resistant pipe grades. Finolex Industries Ltd introduced a smart‑pipe monitoring system integrated with IoT sensors. Prince Pipes and Fittings Ltd. completed the acquisition of a regional pipe fabricator to broaden its HVAC portfolio. Other companies such as Captain Pipes, Dutron, Kankai Pipes & Fittings, Ori‑Plast, Supreme, and Utkarsh India reported capacity upgrades and new product launches targeting irrigation efficiencies.