What is the Heavy Duty Truck Electrification Market Overview – definition, scope, and significance?

The Heavy Duty Truck Electrification Market encompasses the design, production, and integration of electric‑driven components and powertrains for trucks used in freight, construction, and logistics. It covers fully electric, hybrid, fuel‑cell, and electric‑assist systems, as well as ancillary components such as electric pumps, power steering, liquid heaters, compressors, actuators, and alternators. The market is significant because it enables substantial reductions in fuel consumption, greenhouse‑gas emissions, and total cost of ownership, while aligning with global decarbonisation policies and growing demand for sustainable transportation solutions.

What are the main drivers, restraints, challenges, and opportunities in the Heavy Duty Truck Electrification Market?

Key drivers include stringent emission regulations, rising fuel prices, corporate sustainability commitments, and advances in battery technology that improve range and durability. Restraints stem from high upfront capital costs, limited charging infrastructure, and concerns over payload reduction due to battery weight. Challenges involve supply‑chain constraints for rare‑earth materials and the need for standardized safety protocols. Opportunities arise from government incentives, emerging fuel‑cell technologies, and the expansion of telematics that optimize electric fleet management.

Which growth trends are currently shaping the Heavy Duty Truck Electrification Market?

The market is witnessing a rapid shift toward fully electric powertrains for short‑haul applications, while hybrid configurations dominate long‑haul segments. Integration of smart energy‑management software and over‑the‑air updates is becoming commonplace. Additionally, modular component designs—especially for electric pumps and actuators—allow OEMs to retrofit existing chassis, accelerating adoption. Partnerships between component suppliers and logistics firms are also accelerating pilot programs and real‑world testing.

How did COVID‑19 impact the Heavy Duty Truck Electrification Market and what is the recovery trajectory?

During the pandemic, production delays and supply‑chain disruptions temporarily slowed component shipments, causing a short‑term dip in order volumes. However, the crisis highlighted the resilience of electric fleets, as lower fuel dependency proved advantageous when fuel supply chains were strained. Post‑2020, demand rebounded strongly, supported by stimulus packages that prioritized green mobility, and the market is now on a clear upward trajectory.

What does the Competitive Landscape of the Heavy Duty Truck Electrification Market look like?

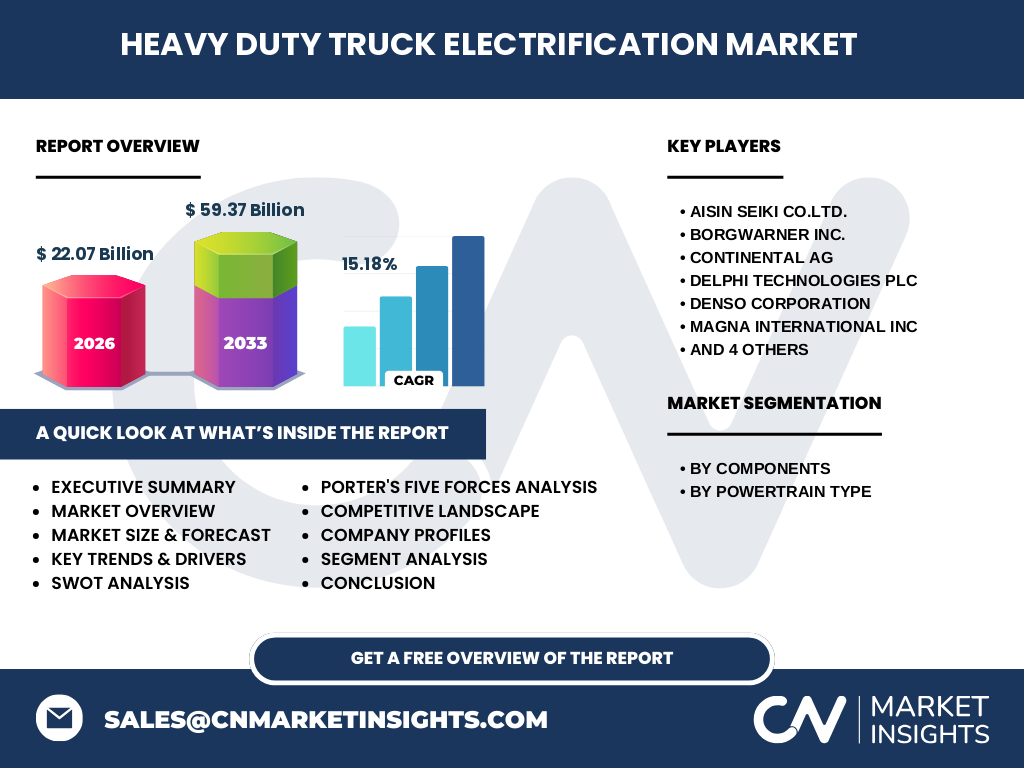

The market is moderately consolidated, led by a handful of global Tier‑1 suppliers and vehicle manufacturers. Companies such as Aisin Seiki, BorgWarner, Continental, Delphi Technologies, Denso, Magna International, Mitsubishi Motors, Bosch, Schaeffler, and ZF dominate component and powertrain development. Recent merger activity and strategic alliances have intensified competition, fostering rapid innovation cycles and pricing pressure across the segment.

What are the key findings summarized in the Executive Summary for the Heavy Duty Truck Electrification Market?

The market is projected to expand from a 2026 valuation of $22.07 billion to $59.37 billion by 2033, delivering a robust CAGR of 15.18 %. Growth is propelled by regulatory pressure, cost‑effective battery solutions, and expanding infrastructure. Component demand is diversifying across electric pumps, steering, heating, and compression systems, while powertrain adoption varies by region and application. Competitive dynamics are intensifying, with leading suppliers pursuing partnerships and technology acquisitions.

What is the forecast outlook for the Heavy Duty Truck Electrification Market from 2025 to 2032?

Based on the provided CAGR of 15.18 %, the market will continue to accelerate, reaching well beyond the $59.37 billion mark by 2033. The forecast anticipates increasing share of fully electric trucks in Europe and North America, while hybrid and fuel‑cell solutions will retain relevance in Asia‑Pacific where long‑haul distances are larger. Component segments linked to power‑train efficiency—such as electric power steering and alternators—are expected to outpace overall market growth.

How is the Heavy Duty Truck Electrification Market sized and shared across its major segments?

Segmentation by components includes electric pumps, electric power steering, liquid heater PTC, electric air‑conditioner compressors, actuators, and alternators. Each segment contributes to the overall market value, with power‑train‑related components (e.g., electric power steering and alternators) representing a larger share due to their direct impact on vehicle efficiency. By powertrain type, fully electric solutions command the fastest growth, followed by hybrids, fuel cells, and finally internal‑combustion‑engine‑based electric assist systems.

What is the global geographic distribution of the Heavy Duty Truck Electrification Market?

The market is globally dispersed, with North America and Europe leading in fully electric adoption driven by strict emissions standards and mature charging networks. Asia‑Pacific shows strong hybrid and fuel‑cell activity, reflecting regional logistics needs and governmental incentives. Emerging markets in Latin America and the Middle East exhibit nascent growth, primarily focused on electric auxiliary components and pilot electrification projects.

What are the detailed regional performance insights for the Heavy Duty Truck Electrification Market?

In North America, fleet operators are rapidly converting short‑haul trucks to fully electric platforms, supported by federal subsidies. Europe’s market is characterized by a balanced mix of electric and hybrid trucks, with extensive public‑charging infrastructure. Asia‑Pacific’s growth is fueled by megacities’ congestion policies and substantial investments in fuel‑cell research, especially in Japan and South Korea. Each region’s regulatory environment, fuel pricing, and infrastructure readiness shape its unique adoption curve.

Which leading companies are profiled in the Heavy Duty Truck Electrification Market and what are their strategies?

Aisin Seiki focuses on compact electric drive modules for commercial trucks. BorgWarner leverages its expertise in electric motors to supply integrated power‑train solutions. Continental delivers advanced control systems for electric steering and braking. Delphi Technologies emphasizes software‑defined electrification platforms. Denso invests in high‑efficiency compressors and thermal management. Magna International expands its modular electric chassis offerings. Mitsubishi Motors drives fuel‑cell truck prototypes. Bosch and ZF provide scalable electric driveline components, while Schaeffler concentrates on precision actuators and bearing technologies.

How does Porter’s Five Forces analysis apply to the Heavy Duty Truck Electrification Market?

Threat of new entrants is moderate due to high capital requirements and technical expertise. Bargaining power of suppliers is elevated for battery and rare‑earth materials, though component diversification mitigates risk. Bargaining power of buyers—large fleet operators—remains strong, pushing for cost reductions and performance guarantees. Threat of substitutes is low, as diesel and gasoline trucks are increasingly regulated out. Industry rivalry is intense, with major OEMs and tier‑1 suppliers racing to secure contracts and technology patents.

What are the SWOT insights for the Heavy Duty Truck Electrification Market?

Strengths: Alignment with climate policies, clear cost‑of‑ownership benefits, and rapid tech advancement. Weaknesses: High initial investment, limited charging density for long‑haul routes. Opportunities: Expansion of public‑private charging partnerships, growth of fuel‑cell powertrains, and integration of AI‑driven fleet analytics. Threats: Supply‑chain volatility for batteries, possible regulatory delays, and competitive pressure from alternative low‑carbon fuels.

What does the value chain of the Heavy Duty Truck Electrification Market look like?

The value chain begins with raw material sourcing (lithium, rare‑earths) followed by component engineering (motors, pumps, actuators). Next, assembly plants integrate these components into powertrain modules, which are then installed in truck chassis by OEMs. Aftermarket services—such as battery management, software updates, and maintenance—complete the chain, providing recurring revenue streams and data feedback loops for continuous improvement.

What key investment insights can be drawn for the Heavy Duty Truck Electrification Market?

Investors should prioritize companies with strong battery‑management IP and diversified component portfolios, as they are best positioned to capture growth across all powertrain types. Funding of charging‑network projects offers synergistic returns, especially in regions with emerging infrastructure. Strategic stakes in firms advancing fuel‑cell technology provide a hedge against future shifts in energy sources. Monitoring policy incentives will help time market entry for maximal upside.

What are the main conclusions of the Heavy Duty Truck Electrification Market report?

The market is on a decisive growth path, driven by environmental regulation, cost pressures, and technological breakthroughs. Component diversification and powertrain flexibility are essential for meeting varied regional demands. Leading suppliers are consolidating expertise through partnerships, while emerging players focus on niche innovations such as smart thermal management. Overall, the sector presents a compelling case for strategic investment and long‑term participation.

How was the research methodology designed for this Heavy Duty Truck Electrification Market study?

The study combined primary interviews with industry executives, OEM engineers, and policy makers, alongside secondary data collection from company reports, regulatory filings, and reputable databases. Quantitative analysis employed time‑series modeling to derive the 15.18 % CAGR, while qualitative assessment triangulated insights across technology trends, regulatory impacts, and supply‑chain dynamics. Validation was performed through cross‑checking with independent market forecasts.

What is the scope of the research and its limitations?

The research covers global heavy‑duty truck electrification, focusing on component and powertrain segmentation, geographic distribution, and competitive dynamics up to 2033. It excludes detailed cost‑breakdown analyses for specific battery chemistries and does not quantify market share for individual companies beyond the listed key players. Data is limited to publicly available information and the provided financial figures.

Which key companies and recent developments are highlighted in the Heavy Duty Truck Electrification Market?

Aisin Seiki announced a joint venture to produce compact electric drive units for urban delivery trucks. BorgWarner unveiled a new high‑torque electric motor optimized for heavy‑load applications. Continental introduced an integrated electric steering system with predictive torque assistance. Delphi Technologies launched a cloud‑based platform for real‑time electric‑fleet monitoring. Denso released a next‑generation electric compressor with improved energy efficiency. Magna International secured a partnership with a major logistics firm to develop modular electric chassis. Mitsubishi Motors demonstrated a fuel‑cell truck prototype capable of 500 km range. Bosch rolled out a scalable alternator for hybrid trucks. Schaeffler introduced a low‑friction actuator line for electric powertrains. ZF Friedrichshafen expanded its e‑axle portfolio with increased load‑capacity options.