1. What is the Aircraft Brackets Market Overview – definition, scope, and significance?

The Aircraft Brackets Market encompasses the design, manufacturing, and supply of structural supports and mounting components used in commercial, general‑aviation, military, and helicopter platforms. Brackets are fabricated from materials such as aluminum and steel and serve critical applications in fuselage, wings, control surfaces, and engines. Their significance lies in ensuring structural integrity, weight optimisation, and compliance with stringent aerospace safety standards, making them essential for OEM production and aftermarket maintenance.

2. What are the market drivers, restraints, challenges, and opportunities?

Key drivers include rising air‑traffic demand, fleet modernisation programmes, and increasing after‑market services, all of which boost bracket volumes. Restraints arise from high material costs and strict certification cycles that lengthen time‑to‑market. Challenges involve supply‑chain disruptions for specialty alloys and pressure to reduce weight without compromising strength. Opportunities stem from advanced additive manufacturing, corrosion‑resistant coatings, and the growth of regional jet programs that require customised bracket solutions.

3. What growth trends are currently shaping the Aircraft Brackets Market?

Current trends feature a shift toward lightweight aluminum alloys for passenger‑aircraft brackets, while steel remains preferred for high‑stress military applications. Digital engineering tools, such as 3‑D modelling and simulation, are accelerating design validation. Additionally, the adoption of modular bracket systems enables faster assembly lines and easier maintenance, reflecting an industry‑wide push for greater efficiency and lower life‑cycle costs.

4. How has COVID‑19 impacted the Aircraft Brackets Market, and what is the recovery trajectory?

The pandemic caused a temporary dip in bracket demand due to grounded fleets and postponed new‑aircraft orders. However, the market demonstrated resilience as OEMs shifted focus to backlog fulfilment and aftermarket repairs, cushioning the decline. Recovery is now underway, driven by the resurgence of commercial travel, renewed defence spending, and accelerated certification of next‑generation aircraft, positioning the market for a strong post‑COVID expansion.

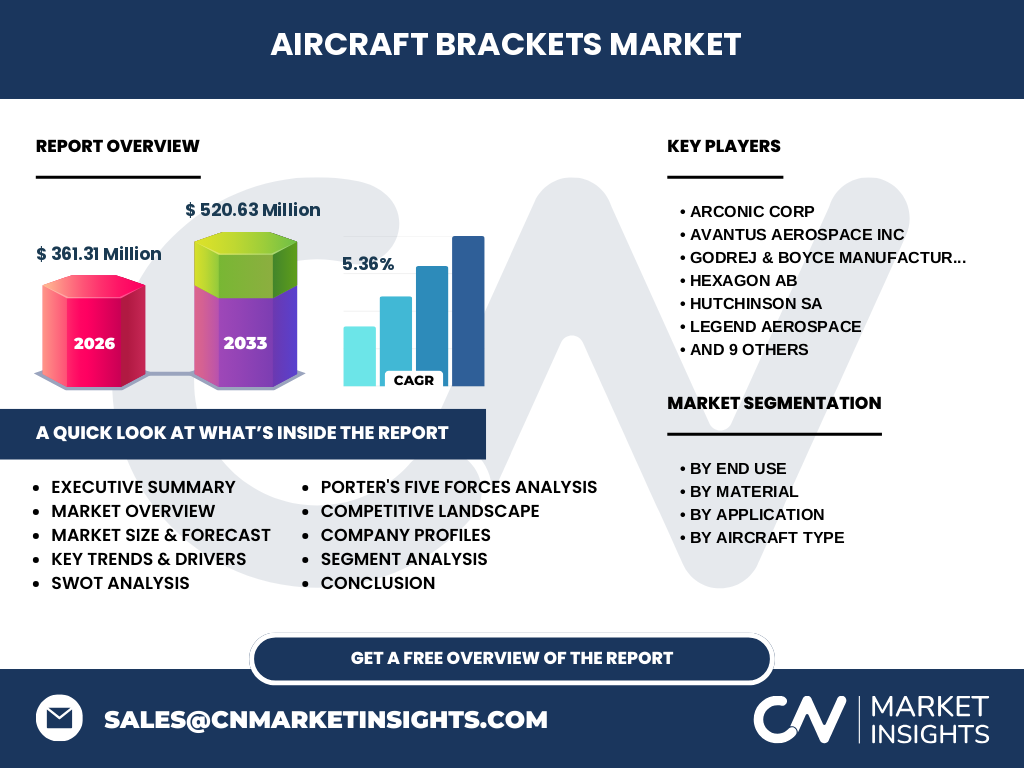

5. Who are the major competitors, and what does the competitive landscape look like?

The market is fragmented with several global players, including Arconic Corp, Avantus Aerospace, Godrej & Boyce Manufacturing, Hexagon AB, Hutchinson SA, Legend Aerospace, Meena Cast Pvt Ltd, Precision Castparts Corp, Premium Aerotec GmbH, RTP Company, SEKISUI Aerospace, STROCO, Singapore Technologies Engineering, Spirit AeroSystems, and Triumph Group. Companies compete on material expertise, technology adoption, and strategic partnerships, leading to moderate consolidation through joint ventures and occasional acquisitions to broaden product portfolios.

6. What are the key findings in the executive summary?

The Aircraft Brackets Market is projected to reach USD 520.63 million by 2033, growing at a 5.36 % CAGR from a 2026 base of USD 361.31 million. Growth is underpinned by expanding commercial fleets, increased aftermarket activity, and innovations in lightweight materials. Geographic diversification and a balanced mix of OEM and aftermarket demand provide a stable revenue foundation, while emerging technologies present pathways for higher margin offerings.

7. What is the market forecast for 2025‑2032?

Based on the provided CAGR of 5.36 %, the market is expected to continue its upward trajectory, moving from the 2026 valuation of USD 361.31 million toward the 2033 forecast of USD 520.63 million. This steady growth reflects sustained aircraft deliveries, intensified refurbishment cycles, and ongoing investments in advanced bracket manufacturing processes across all aircraft categories.

8. How is the market sized and shared by segmentation?

Segmentation by end use shows OEMs as the primary demand driver, with aftermarket services contributing a significant secondary share as aircraft age. Material segmentation highlights aluminum as the preferred choice for weight‑critical applications, while steel dominates in high‑load military brackets. Application‑wise, fuselage and wing brackets together account for the largest portion, followed by control surfaces, with engine brackets representing a niche yet high‑value segment. Aircraft‑type segmentation indicates commercial aircraft as the dominant consumer, supported by robust general‑aviation and defence demand.

9. What is the global market size and share by region?

While specific regional dollar values are not disclosed, the market’s global footprint spans North America, Europe, Asia‑Pacific, the Middle East, and Latin America. Each region contributes to the overall USD 361.31 million base in 2026, with North America and Europe historically holding the largest shares due to mature aerospace ecosystems, and Asia‑Pacific emerging rapidly driven by new aircraft programmes and rising defence budgets.

10. What does the regional analysis reveal about market performance?

North America continues to lead in bracket innovation, benefiting from major OEMs and a strong aftermarket network. Europe sustains high demand through legacy commercial programmes and defence contracts. Asia‑Pacific shows the fastest growth rate, propelled by expanding commercial fleets in China and India, and increasing military modernization. The Middle East and Latin America present steady growth linked to regional airline expansion and selective defence procurement.

11. Which companies lead the market and what are their strategies?

Industry leaders such as Arconic Corp and Precision Castparts Corp leverage advanced alloy technologies and scale production capacity. Avantus Aerospace focuses on custom‑engineered solutions for niche military applications. Spirit AeroSystems and Triumph Group pursue vertical integration, expanding from bracket fabrication to complete structural assemblies. Companies like Hexagon AB invest in digital twin and simulation tools to shorten design cycles, while Singapore Technologies Engineering emphasizes strategic partnerships in the Asia‑Pacific region.

12. How do Porter’s Five Forces affect the Aircraft Brackets Market?

Threat of new entrants is moderate due to high capital requirements and certification barriers. Bargaining power of suppliers is significant, especially for specialised aerospace‑grade aluminum and steel alloys. Bargaining power of buyers is strong, with OEMs demanding strict quality and cost controls. Threat of substitutes remains low because brackets are essential structural components with few alternatives. Industry rivalry is intense, driven by technology differentiation and price competition among a large pool of qualified manufacturers.

13. What are the market’s SWOT elements?

Strengths: Essential role in aircraft safety, diversified end‑use base, and robust demand from both OEM and aftermarket. Weaknesses: High material costs and lengthy certification timelines. Opportunities: Adoption of additive manufacturing, development of high‑strength lightweight alloys, and expansion into emerging regional markets. Threats: Supply‑chain volatility for critical alloys and potential regulatory changes affecting material standards.

14. How is the value chain structured for aircraft brackets?

The value chain starts with raw‑material sourcing (aluminum, steel), followed by alloy processing and precision casting or machining. Next, design and engineering services apply digital simulation before prototype testing. Manufacturing includes CNC machining, forging, or additive processes, after which brackets undergo surface treatment and rigorous inspection. Final stages involve logistics, OEM integration, and aftermarket distribution, with after‑sales support completing the cycle.

15. What key investment insights should stakeholders consider?

Investors should target companies with proven capabilities in lightweight alloy processing and digital design platforms, as these areas promise higher margins. Partnerships with OEMs and long‑term service agreements in the aftermarket provide revenue stability. Funding R&D for additive manufacturing and corrosion‑resistant coatings can create differentiated product lines, while geographic expansion into Asia‑Pacific offers growth leverage.

16. What are the main conclusions of the market analysis?

The Aircraft Brackets Market is on a steady growth path, projected to exceed USD 520 million by 2033. Weight‑reduction trends, rising aftermarket activity, and technological advancements create a resilient demand environment. While material costs and certification remain challenges, the market’s diversified end‑use base and regional expansion opportunities make it an attractive segment for manufacturers and investors alike.

17. How was the research conducted?

The study combined primary interviews with industry experts, OEM engineers, and supplier representatives, alongside secondary data from aerospace trade publications, company filings, and reputable market databases. Trend analysis, quantitative forecasting using the provided CAGR, and segmentation modeling were applied to ensure a comprehensive view of the market dynamics.

18. What is the scope of the research and its limitations?

The research covers global aircraft bracket demand across four material types, five application areas, and four aircraft categories, spanning OEM and aftermarket segments. It does not provide detailed regional revenue figures beyond the aggregate market size, nor does it quantify individual company market shares, as such data were not supplied. The analysis focuses on the period up to 2033.

19. Which key companies have recent developments, and what are they?

Arconic Corp announced a new high‑strength aluminum alloy line for commercial wing brackets. Avantus Aerospace secured a defence contract to supply steel brackets for next‑generation fighter jets. Precision Castparts Corp launched an additive‑manufacturing pilot plant for complex bracket geometries. Spirit AeroSystems expanded its bracket‑assembly facility in Wichita, enhancing capacity for both OEM and aftermarket customers. Triumph Group reported a strategic partnership with a leading Asian airline to provide customised after‑market bracket solutions.