1. What is the Asia Pacific Ceramic Fiber Market Overview – definition, scope, and significance?

The Asia Pacific Ceramic Fiber market comprises the production and supply of high‑temperature insulation materials such as refractory ceramic fiber and alkaline‑earth silicate wool. These fibers are manufactured in various forms—blanket, module, board, and paper—and are employed across iron and steel, refining & petrochemical, power generation, and aluminum industries. The market’s significance stems from its role in improving energy efficiency, reducing emissions, and enabling safe operation of furnaces and kilns throughout the rapidly industrializing Asia‑Pacific region.

2. What are the key drivers, restraints, challenges, and opportunities in the Asia Pacific Ceramic Fiber Market?

Growth is driven by rising steel production, expansion of petrochemical complexes, and increasing power‑generation capacity, all of which demand high‑performance insulation. Urbanization and governmental emphasis on energy‑saving technologies create further demand. Restraints include high raw‑material costs and stringent environmental regulations governing fiber disposal. Challenges arise from the need for advanced manufacturing capabilities and competition from alternative inorganic insulators. Opportunities exist in developing eco‑friendly fiber grades, retrofitting old plants, and leveraging government subsidies for energy‑efficient upgrades.

3. What growth trends are currently shaping the Asia Pacific Ceramic Fiber market?

Current trends feature a shift toward low‑density, high‑temperature‑resistant blankets for next‑generation blast furnaces, and the adoption of modular insulation systems that shorten installation time. End‑users are increasingly integrating digital monitoring to track thermal performance, prompting manufacturers to offer smart‑compatible products. Moreover, the rise of renewable‑energy‑linked power generation (e.g., biomass and waste‑to‑energy) is expanding the market beyond traditional coal‑based plants.

4. How did COVID‑19 impact the Asia Pacific Ceramic Fiber market and what is the recovery trajectory?

The pandemic caused temporary plant shutdowns and delayed capital projects, leading to a short‑term dip in demand. However, stimulus packages and accelerated infrastructure spending in key economies such as China, India, and South Korea have helped the market rebound. By late 2023, order backlogs began to clear, and demand is now growing at a pace that aligns with the projected 8.89% CAGR, indicating a robust recovery trajectory.

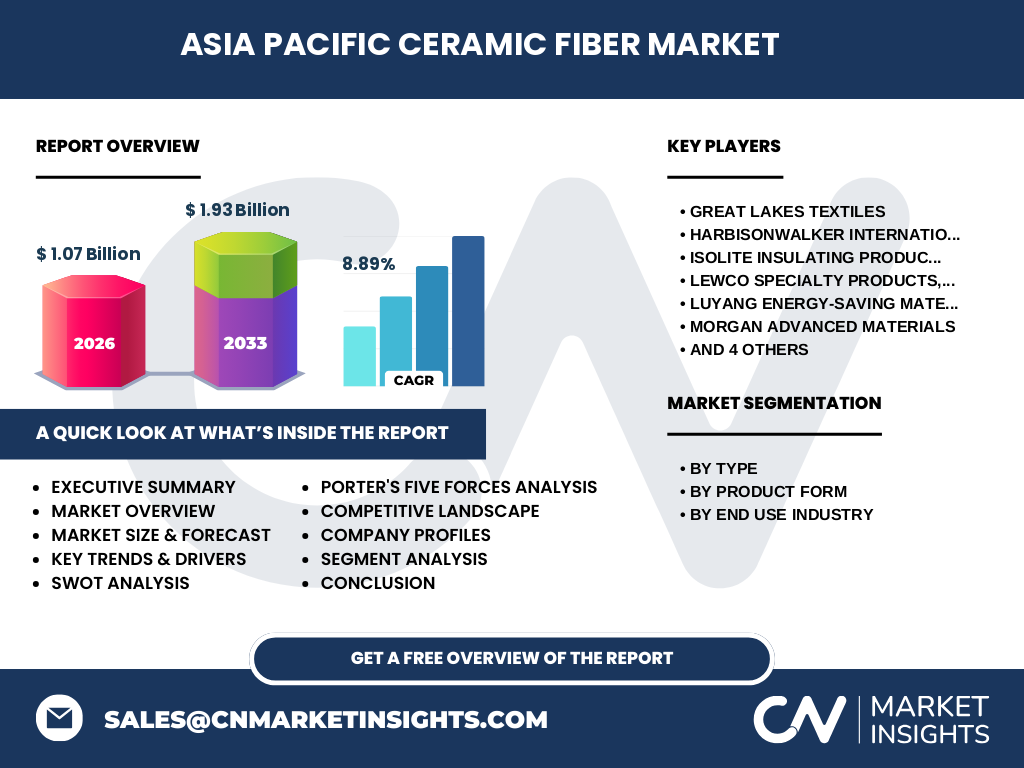

5. Who are the major competitors and what does the competitive landscape look like in the Asia Pacific Ceramic Fiber market?

The market is fragmented, with several global and regional players competing on product quality and service. Leading companies include Great Lakes Textiles, HarbisonWalker International, Inc., Isolite Insulating Products Co., Ltd., Lewco Specialty Products, Inc., Luyang Energy‑Saving Materials Co., Ltd., Morgan Advanced Materials, Nutec Group, Pyrotek Inc., Rath‑Group, and Unifrax LLC. Consolidation activity remains moderate, as firms pursue strategic partnerships and joint ventures to broaden geographic reach and enhance R&D capabilities.

6. What are the high‑level findings in the Executive Summary for the Asia Pacific Ceramic Fiber market?

The Asia Pacific Ceramic Fiber market is valued at USD 1.07 billion in 2026 and is forecast to reach USD 1.93 billion by 2033, reflecting an 8.89% CAGR. Strong industrial expansion, energy‑saving mandates, and innovation in fiber forms are the primary growth levers. The market is dominated by a mix of multinational manufacturers and specialized regional firms, with a clear trend toward eco‑friendly product development and digital integration.

7. What is the forecast for the Asia Pacific Ceramic Fiber market between 2025 and 2032?

Based on the projected CAGR of 8.89%, the market is expected to continue expanding steadily from its 2026 base of USD 1.07 billion to approximately USD 1.93 billion by 2033. This growth translates into a consistent upward trajectory through 2025‑2032, driven by ongoing capacity additions in steel, petrochemical, power, and aluminum sectors across the region.

8. How is the Asia Pacific Ceramic Fiber market sized and shared by segmentation?

By type, the market is split between refractory ceramic fiber and alkaline‑earth silicate wool, each serving distinct temperature ranges and durability requirements. Product‑form segmentation includes blanket, module, board, and paper, with blankets holding the largest share due to their versatility in furnace lining. End‑use segmentation shows iron and steel as the top consumer, followed by refining & petrochemical, power generation, and aluminum, reflecting the thermal insulation needs of high‑temperature processing.

9. What is the global Asia Pacific Ceramic Fiber market size and share by region?

Within the global context, the Asia Pacific region accounts for the majority of ceramic fiber consumption, underpinned by the region’s extensive heavy‑industry base. While exact global figures are not disclosed, the regional market’s USD 1.07 billion valuation in 2026 highlights its dominant position relative to other geographies.

10. What does the regional analysis reveal about market performance across Asia Pacific?

China leads the market with the highest demand, driven by its massive steel and petrochemical complexes. India and South Korea follow, supported by expanding power‑generation capacity and aluminum production. Southeast Asian nations such as Indonesia and Vietnam are emerging as new growth hubs due to rising industrialization and governmental incentives for energy‑efficient manufacturing.

11. Which companies are leading in the Asia Pacific Ceramic Fiber market and what are their key strategies?

Great Lakes Textiles focuses on high‑performance blanket technologies, while HarbisonWalker emphasizes sustainable fiber blends. Isolite Insulating Products leverages localized production to reduce lead times. Morgan Advanced Materials invests heavily in R&D for heat‑resistant nano‑coated fibers. Nutec Group and Luyang Energy‑Saving Materials pursue strategic partnerships with steel mills to secure long‑term supply contracts. Across the board, companies are expanding distribution networks and enhancing after‑sales technical support.

12. How does Porter’s Five Forces analysis apply to the Asia Pacific Ceramic Fiber market?

• Threat of new entrants: Moderate – high capital intensity and technical expertise create barriers. • Bargaining power of suppliers: Low to moderate – raw material (silica, alumina) markets are competitive. • Bargaining power of buyers: High – large steel and petrochemical firms negotiate volume discounts. • Threat of substitutes: Low – few alternative materials match the high‑temperature performance of ceramic fibers. • Competitive rivalry: Intense – numerous specialized players compete on product differentiation and service.

13. What are the SWOT insights for the Asia Pacific Ceramic Fiber market?

Strengths: Proven high‑temperature performance and energy‑saving benefits. Weaknesses: High production costs and disposal concerns. Opportunities: Development of greener fiber grades, retrofitting projects, and digital‑enabled insulation monitoring. Threats: Potential regulatory tightening on fiber waste and emerging alternative insulation technologies.

14. How is the value chain structured for the Asia Pacific Ceramic Fiber market?

The value chain starts with raw‑material extraction (silica, alumina), followed by fiber spinning and heat‑treatment processes. Next, manufacturers convert fibers into specific forms—blanket, module, board, paper. Distribution channels include direct sales to large industrial customers and third‑party distributors. After‑sales services encompass installation assistance, performance monitoring, and replacement planning, creating added value throughout the chain.

15. What key investment insights should investors consider for the Asia Pacific Ceramic Fiber market?

Investors should target companies with strong R&D pipelines for eco‑friendly fibers and those securing long‑term contracts with major steel and petrochemical firms. Partnerships that enhance regional manufacturing footprints and enable faster delivery are also attractive. Given the 8.89% CAGR, capital allocation toward capacity expansion in China, India, and Southeast Asia offers solid upside potential.

16. What are the main conclusions and takeaways from the Asia Pacific Ceramic Fiber market analysis?

The market is on a solid growth path, underpinned by industrial expansion and energy‑efficiency mandates. Refractory ceramic fiber and alkaline‑earth silicate wool remain essential, with blankets dominating product form share. Competitive dynamics favor firms that combine technological innovation with localized production. The forecasted rise to USD 1.93 billion by 2033 underscores a lucrative opportunity for manufacturers, investors, and end‑users alike.

17. How was the research methodology designed for this market study?

The study employed a mixed‑method approach, combining primary interviews with industry experts, manufacturers, and key end‑users, alongside secondary data from company reports, trade publications, and government statistics. Quantitative data were validated through cross‑checking with multiple sources, and qualitative insights were integrated to contextualize market drivers and trends.

18. What is the scope of this research and what limitations, if any, should be noted?

The scope covers the Asia Pacific Ceramic Fiber market from 2026 to 2033, segmented by type, product form, and end‑use industry, and includes competitive, regional, and value‑chain analyses. Limitations stem from the proprietary nature of some company financials, which restricts the inclusion of exact revenue shares for individual firms.

19. Which key companies have recent developments, and what are their latest announcements?

Great Lakes Textiles launched a low‑emission blanket line targeting the Chinese steel sector. HarbisonWalker International announced a joint venture with an Indian petrochemical firm to localize production. Isolite Insulating Products introduced a high‑flexibility module for power‑generation retrofits. Morgan Advanced Materials unveiled a nano‑coated refractory fiber aimed at extending furnace life. Nutec Group signed a multi‑year supply agreement with a major aluminum producer in South Korea, while Luyang Energy‑Saving Materials opened a new plant in Vietnam to serve emerging markets.