What is the Europe Contract Research Organization (CRO) Market Overview – definition, scope, and significance?

The Europe Contract Research Organization (CRO) market encompasses service providers that assist pharmaceutical, biotechnology, medical device firms and academic institutions in conducting pre‑clinical and clinical research. CROs offer a range of services from early‑phase development and laboratory analytics to full‑scale clinical trial management and post‑approval support. The market’s scope includes both in‑house capabilities that companies retain internally and outsourced functions delivered by external CRO partners. Its significance lies in accelerating drug and device pipelines, reducing time‑to‑market, and providing cost‑effective expertise that many sponsors lack in‑house. By leveraging specialized CROs, European sponsors can navigate complex regulatory environments, access diversified patient pools across the continent, and benefit from advanced technologies such as digital biomarkers and decentralized trial platforms.

What are the key drivers, restraints, challenges, and opportunities shaping the Europe CRO market?

Drivers include rising R&D spending by pharma and biotech firms, increasing prevalence of chronic diseases (oncology, neurology, cardiology), and a strong emphasis on fast‑track approvals by European regulators. The growth of personalized medicine and the need for real‑world evidence further boost demand for specialized CRO services. Restraints involve stringent data‑privacy regulations (GDPR) and escalating operational costs for maintaining high‑quality clinical sites. Challenges revolve around talent shortages in clinical operations, variable reimbursement policies across EU member states, and the complexity of multi‑country trial coordination. Opportunities arise from emerging therapeutic areas such as metabolic disorders, the expansion of decentralized clinical trials, and the adoption of AI‑driven data analytics, which can enhance trial efficiency and patient engagement.

What are the current and emerging growth trends in the Europe CRO market?

Key trends include a shift from traditional site‑centric models to decentralized and hybrid trial designs, enabling remote patient monitoring and reducing site burden. There is increasing utilization of real‑world data (RWD) and real‑world evidence (RWE) to complement randomized trials, especially in oncology and rare diseases. CROs are expanding service portfolios to cover end‑to‑end solutions, integrating early‑phase development, clinical operations, laboratory services, and post‑approval surveillance. Partnerships between CROs and digital health tech firms are accelerating the adoption of wearables, e‑consent platforms, and electronic data capture (EDC) systems. Finally, consolidation through mergers and acquisitions is creating larger, multi‑functional CROs capable of handling complex, global studies.

How did COVID‑19 impact the Europe CRO market and what is the recovery trajectory?

The pandemic initially disrupted patient enrollment and site activation, causing delays in many clinical programs. However, CROs quickly adapted by implementing remote monitoring, virtual site visits, and digital consent processes, which mitigated disruptions. Post‑COVID, demand for CRO services rebounded strongly as sponsors accelerated late‑stage trials to meet urgent therapeutic needs, particularly in infectious diseases and oncology. The market has entered a recovery phase marked by accelerated digital transformation and an increased appetite for flexible trial designs, positioning CROs for sustained growth beyond the pandemic.

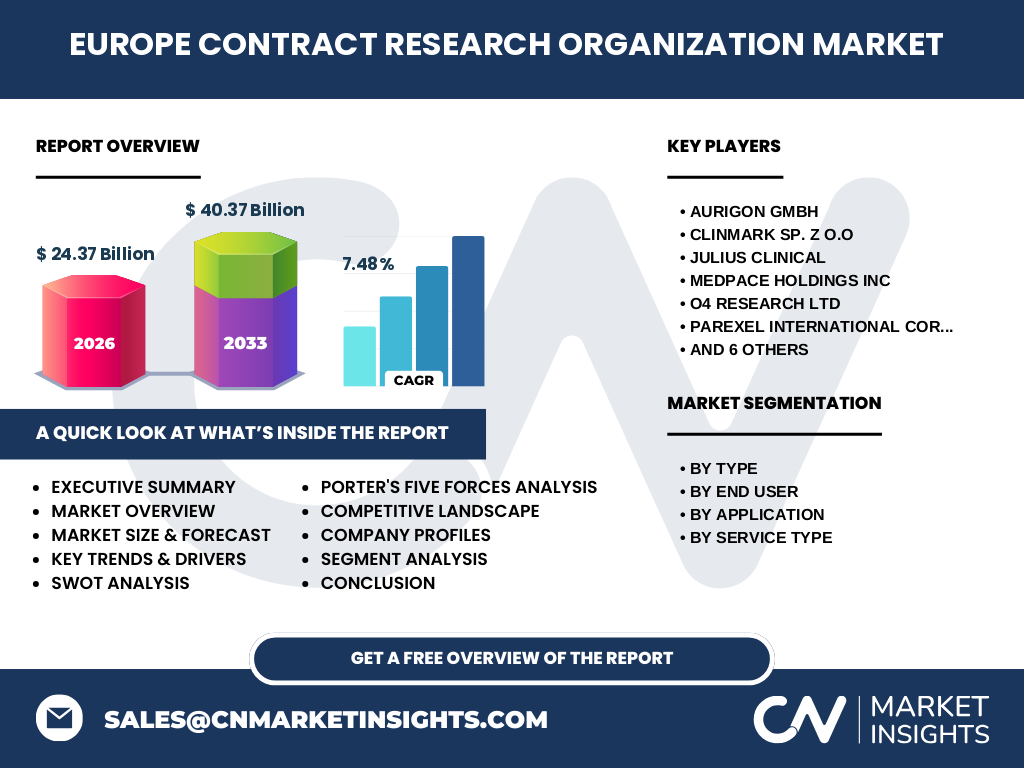

Who are the major competitors and what is the competitive landscape of the Europe CRO market?

The European CRO landscape is fragmented but increasingly consolidated, featuring both global players and niche specialists. Prominent competitors include Thermo Fisher Scientific (PPD Inc), Parexel International Corp, Medpace Holdings Inc, Julius Clinical, Smerud Medical Research Group, and ProPharma Group. Regional specialists such as AURIGON GMBH, Clinmark sp. z o.o, O4 Research Ltd, Pharmaxi LLC, Precision Medicine Group LLC, and Siron Clinical add depth to the market. Competitive strategies focus on expanding service breadth, investing in digital platforms, and forming strategic alliances to broaden geographical reach across Europe.

What are the key findings in the Executive Summary of the Europe CRO market?

The Europe CRO market is valued at €24.37 billion in 2026 and is projected to reach €40.37 billion by 2033, representing a CAGR of 7.48 %. Growth is driven by rising R&D intensity, the expansion of therapeutic areas, and the rapid adoption of decentralized trial models. The market demonstrates a balanced mix of in‑house and outsourced activities, with strong demand from pharmaceutical and biotech companies, medical device firms, and academic research institutes. Competitive pressures are intensifying through consolidation, while opportunities abound in digitalization, AI‑enabled analytics, and emerging disease segments.

What are the forecast projections for the Europe CRO market from 2025 to 2032?

Based on the provided CAGR of 7.48 %, the market is expected to continue expanding robustly through 2032. The forecast indicates a steady increase in total market value, reaching approximately €40.37 billion by 2033. This growth reflects ongoing investment in innovative drug development, heightened regulatory encouragement for expedited approvals, and the scaling of digital trial infrastructures across Europe.

How is the Europe CRO market sized and shared by segmentation?

The market is segmented by type, end‑user, application, and service type. By type, services are divided between In‑House capabilities retained by sponsors and Outsource solutions provided by CROs. End‑users include Pharmaceutical and Biotech Companies, Medical Device Companies, and Academic and Research Institutes. Application areas span Oncology, Neurology, Cardiology, Infectious Diseases, Metabolic Disorders, Nephrology, Respiratory, Dermatology, Ophthalmology, and Hematology. Service‑type segmentation covers Early Phase Development Services, Clinical Research Services, Laboratory Services, and Post‑Approval Services. While exact numerical shares are not disclosed, the broad distribution highlights the market’s versatility across multiple therapeutic and functional domains.

What is the global Europe CRO market size and share by region?

Europe remains a core region within the global CRO ecosystem, contributing the majority of the market’s value at €24.37 billion in 2026. The region’s share reflects its mature regulatory frameworks, extensive clinical trial networks, and high concentration of pharmaceutical headquarters. While specific figures for other continents are not provided, Europe’s dominant position underscores its strategic importance for global drug development programs.

What does the regional analysis reveal about Europe’s CRO market performance?

Regional performance varies across Western, Central, and Eastern Europe. Western Europe, led by Germany, the United Kingdom, and France, exhibits the highest concentration of CRO facilities and sponsor activities due to robust infrastructure and funding environments. Central and Eastern European countries, such as Poland and the Czech Republic, are gaining traction thanks to cost‑effective sites, skilled clinical staff, and favorable patient recruitment rates. This geographic diversification enables sponsors to balance cost efficiencies with high‑quality data generation.

Which companies lead the Europe CRO market and what are their strategic approaches?

Leading firms include Thermo Fisher Scientific (PPD Inc), Parexel International Corp, Medpace Holdings Inc, Julius Clinical, and Smerud Medical Research Group. These companies pursue growth through global expansion, service diversification, and technology integration. Regional specialists such as AURIGON GMBH, Clinmark sp. z o.o, and O4 Research Ltd focus on niche therapeutic expertise and localized site networks. Strategic approaches commonly involve M&A activity, partnerships with digital health providers, and investment in AI‑driven trial optimization platforms.

How does Porter’s Five Forces analysis apply to the Europe CRO market?

Threat of new entrants: Moderate, as entry barriers exist in terms of regulatory compliance, capital intensity, and need for specialized expertise. Bargaining power of buyers: High, sponsors demand cost‑effective, high‑quality services and can switch providers. Bargaining power of suppliers: Low to moderate; key inputs (clinical sites, patient pools) are abundant, though skilled staff can be scarce. Threat of substitutes: Low, given limited alternatives to professional CRO services for comprehensive trial execution. Industry rivalry: Intense, driven by consolidation, service diversification, and price competition among both global and regional CROs.

What are the SWOT insights for the Europe CRO market?

Strengths: Established regulatory environment, mature clinical trial infrastructure, and strong expertise in therapeutic areas. Weaknesses: Fragmented market with varying cost structures, and reliance on skilled personnel that are in short supply. Opportunities: Expansion of decentralized trials, AI‑enabled data analytics, and growth in emerging therapeutic fields such as metabolic disorders. Threats: Regulatory changes, data‑privacy constraints, and potential economic downturns affecting sponsor budgets.

How is value created and transferred in the Europe CRO value chain?

The value chain begins with protocol design and pre‑clinical support, proceeds through clinical site selection, patient recruitment, data collection, and statistical analysis, and concludes with regulatory submission support and post‑approval surveillance. CROs add value by offering specialized expertise at each stage, deploying technology platforms for efficient data capture, and providing regulatory consultancy. The flow of value moves from sponsors (who fund and set strategic objectives) to CROs (who execute and manage trial operations) and finally to regulators and patients who benefit from timely access to safe therapies.

What investment insights are key for stakeholders in the Europe CRO market?

Investors should target CROs that demonstrate robust digital capabilities, diversified service portfolios, and geographic reach across both Western and Eastern Europe. Companies investing in AI‑driven trial optimization, decentralized trial platforms, and strategic alliances with technology firms are likely to capture higher margins. Additionally, firms with a proven track record of successful M&A integration and strong regulatory expertise present attractive long‑term growth prospects.

What is the concluding summary and key takeaways for the Europe CRO market?

The Europe CRO market is on a strong upward trajectory, forecast to grow from €24.37 billion in 2026 to €40.37 billion by 2033 at a 7.48 % CAGR. The market’s growth is propelled by increasing R&D investment, digital transformation, and expanding therapeutic indications. While regulatory and talent challenges persist, opportunities in decentralized trials and AI‑enhanced analytics provide compelling avenues for differentiation. Stakeholders should focus on technology adoption, strategic partnerships, and geographic diversification to maximize returns.

How was the research for this Europe CRO market report conducted?

The research employed a mixed‑method approach, combining secondary data collection from industry reports, regulatory publications, and company filings with primary interviews of key opinion leaders, CRO executives, and sponsor representatives. Quantitative analysis utilized the provided market size and CAGR to generate forecasts, while qualitative insights were derived from trend monitoring and competitive intelligence.

What is the scope and any limitations of this Europe CRO market research?

The scope covers the entire European CRO ecosystem, including all service types, end‑users, and therapeutic applications listed in the segmentation. Geographic coverage includes Western, Central, and Eastern Europe. Limitations stem from the reliance on publicly available data and the absence of granular market‑share percentages for individual regions or segments, which are addressed through qualitative benchmarking.

Which key companies have recent developments, and what are their latest initiatives in the Europe CRO market?

Recent developments include Thermo Fisher Scientific (PPD Inc) expanding its decentralized trial platform across the EU, Parexel International Corp launching an AI‑driven patient recruitment engine, and Medpace Holdings Inc acquiring a boutique European laboratory services firm to bolster its Laboratory Services offering. Julius Clinical announced a partnership with a leading digital health startup to integrate wearable sensor data into oncology trials. Smerud Medical Research Group opened new clinical sites in Poland and the Czech Republic to support oncology and neurology programs. Regional players such as AURIGON GMBH and Clinmark sp. z o.o have secured multi‑year contracts with major pharma sponsors for Early Phase Development Services, reflecting growing confidence in their specialized expertise.