What is the Precision Aquaculture Market Overview – definition, scope, and significance?

Precision aquaculture refers to the application of advanced technologies—such as sensors, data analytics, automation, and robotics—to optimize the cultivation of fish, crustaceans, and other aquatic species. The market encompasses smart feeding systems, monitoring and control platforms, and underwater ROV solutions, covering hardware, software, and services that support feeding management, health monitoring, and environmental control. By delivering real‑time insights and automated interventions, precision aquaculture improves productivity, reduces resource waste, and enhances sustainability, making it a critical enabler for the rapidly expanding global seafood industry.

What are the main drivers, restraints, challenges, and opportunities in the Precision Aquaculture Market?

Key drivers include rising global protein demand, tightening environmental regulations, and decreasing margins that push producers toward efficiency‑enhancing technologies. Opportunities arise from the integration of AI‑based analytics, the growing adoption of IoT connectivity in offshore farms, and increasing venture capital interest. Restraints involve high upfront capital costs and limited technical expertise among traditional aquaculture operators. Challenges revolve around data security concerns, interoperability of legacy systems, and the need for robust connectivity in remote marine locations.

Which growth trends are currently shaping the Precision Aquaculture Market?

Current trends feature a shift toward fully automated feeding cycles powered by machine‑learning algorithms that predict appetite based on water quality and fish behavior. Another emerging trend is the deployment of underwater ROVs equipped with high‑resolution imaging for early disease detection. Hybrid cloud‑edge architectures are also gaining traction, allowing real‑time processing of sensor data on‑site while leveraging cloud analytics for long‑term pattern recognition.

How did COVID‑19 affect the Precision Aquaculture Market and what is the recovery trajectory?

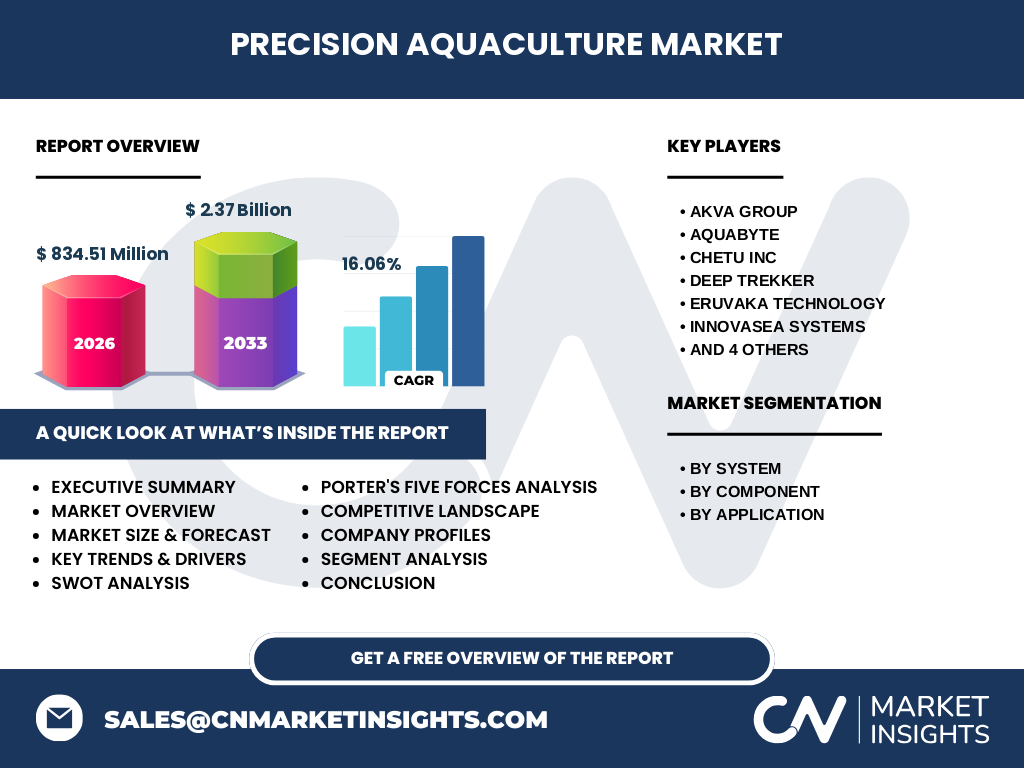

The pandemic initially disrupted supply chains for hardware components, delaying several pilot projects. However, heightened awareness of food security and the resilience of aquaculture prompted accelerated investment in automation to offset labor shortages and social distancing requirements. By 2022, project pipelines recovered, and the market entered a strong growth phase, reflected in the robust forecasted CAGR of 16.06% through 2033.

Who are the major competitors in the Precision Aquaculture Market and what is the level of consolidation?

Leading players include AKVA GROUP, Aquabyte, CHETU INC, DEEP TREKKER, ERUVAKA TECHNOLOGY, INNOVASEA SYSTEMS, PENTAIR AES, SOLVAY, Scale AQ, and XYLEM INC. The competitive landscape shows moderate consolidation, with larger firms acquiring niche technology startups to broaden their product portfolios and enhance end‑to‑end service offerings. This trend fosters a market where a few diversified giants coexist with specialized innovators.

What are the high‑level insights and key findings in the Executive Summary?

The precision aquaculture market is projected to expand from a 2026 valuation of USD 834.51 million to USD 2.37 billion by 2033, driven by a 16.06% CAGR. Growth is underpinned by demand for sustainable protein, regulatory pressure for waste reduction, and rapid technology adoption across feeding, monitoring, and control segments. North America and Europe lead early adoption, while Asia‑Pacific shows the fastest emerging uptake, creating a globally balanced growth outlook.

What are the market forecasts for 2025‑2032?

Based on the current trajectory, the market is expected to maintain double‑digit growth throughout the forecast horizon, reaching approximately USD 2.37 billion by 2033. The compounded annual growth rate of 16.06% suggests steady expansion across all system categories, with smart feeding systems and monitoring & control platforms expected to capture the largest share of incremental revenue.

How is the market sized and shared by segmentation?

By system, the market is divided into Smart Feeding Systems, Monitoring and Control Systems, and Underwater ROV Systems. By component, it includes Hardware, Software, and Service offerings. By application, the market serves Feeding Management, Monitoring, and Control & Surveillance functions. Each segment benefits from cross‑selling opportunities; for example, hardware installations often require complementary software analytics and ongoing service contracts.

What is the global market size and share by region?

The global precision aquaculture market totals USD 834.51 million in 2026. While specific regional monetary shares are not disclosed, the market is characterized by strong footholds in North America and Europe, with accelerating penetration in Asia‑Pacific driven by large‑scale fish farming operations. Latin America and the Middle East present emerging opportunities as local governments promote aquaculture modernization.

What does the regional analysis reveal about market performance?

North America leads in technology integration due to mature supply chains and high investment capacity. Europe follows closely, emphasizing sustainability standards that favor precision tools. Asia‑Pacific exhibits the highest growth rate, propelled by expanding aquaculture acreage in China, Vietnam, and Indonesia. Latin America shows modest but steady adoption, while the Middle East and Africa remain nascent markets with significant upside potential as infrastructure improves.

Which companies are leading the market and what strategies are they pursuing?

AKVA GROUP focuses on end‑to‑end farm solutions, leveraging its extensive equipment base. Aquabyte specializes in AI‑driven image analytics for health monitoring. INNOVASEA SYSTEMS expands its portfolio through strategic acquisitions of sensor manufacturers. XYLEM INC emphasizes water‑treatment integration with its precision platforms. Across the board, firms are investing in R&D, forming partnerships with research institutions, and pursuing subscription‑based service models to generate recurring revenue.

How does Porter’s Five Forces analysis apply to the Precision Aquaculture Market?

• Threat of new entrants: Moderate – high technology thresholds and capital intensity deter newcomers, yet niche startups can enter via specialized software. • Bargaining power of suppliers: Low to moderate – component suppliers are diversified, but rare‑earth sensors may command premium pricing. • Bargaining power of buyers: Growing – large aquaculture firms demand customized solutions and competitive pricing. • Threat of substitutes: Low – traditional manual feeding and monitoring are less efficient and face regulatory pushback. • Competitive rivalry: High – established players vie for market share through innovation, acquisitions, and service differentiation.

What are the main strengths, weaknesses, opportunities, and threats in the SWOT analysis?

Strengths: Strong demand for sustainable protein, proven productivity gains, and supportive regulatory trends. Weaknesses: High initial investment and varying digital literacy among operators. Opportunities: Expansion into emerging aquaculture regions, integration of 5G connectivity, and development of AI‑based predictive maintenance. Threats: Cybersecurity risks, potential supply chain disruptions for sensor components, and resistance from traditional farming communities.

How is the value chain structured in the Precision Aquaculture Market?

The value chain begins with raw material suppliers (electronics, sensor components), proceeds to system integrators that assemble hardware and embed software, followed by distributors and OEM partners delivering solutions to farms. After installation, service providers offer maintenance, data analytics, and advisory support, creating a recurring revenue loop that enhances customer lifetime value.

What investment insights can be drawn for the Precision Aquaculture Market?

Investors should prioritize companies with diversified revenue streams across hardware, software, and services, as this mix mitigates cyclical risks. Companies securing long‑term farm contracts or subscription models present attractive cash‑flow stability. Additionally, firms that own proprietary AI algorithms or own critical sensor patents are positioned for higher valuation multiples.

What are the concluding takeaways from the Precision Aquaculture Market analysis?

The precision aquaculture market is on a rapid growth trajectory, underpinned by sustainability imperatives and technology adoption. With a projected market size of USD 2.37 billion by 2033 and a robust CAGR of 16.06%, the sector offers compelling opportunities for innovators, investors, and policy makers. Success will hinge on delivering cost‑effective, interoperable solutions and fostering industry‑wide data standards.

What research methodology was employed to compile this report?

The study combined primary interviews with industry executives, secondary data collection from company filings, market databases, and academic research. Quantitative forecasts were derived using compound annual growth rate calculations anchored to the 2026 base figure of USD 834.51 million and the 2033 outlook of USD 2.37 billion. Qualitative insights were validated through cross‑checking of multiple sources.

What is the scope of the research and its coverage?

The research covers global precision aquaculture technologies across system, component, and application segments. Geographic scope includes North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa. The analysis addresses market size, growth drivers, competitive dynamics, and strategic outlook while focusing on the period from 2026 to 2033.

Which key companies and recent developments are shaping the Precision Aquaculture Market?

AKVA GROUP announced a partnership with a leading cloud provider to enhance remote farm monitoring. Aquabyte launched an AI‑powered disease detection platform that reduced mortality by 12% in pilot farms. DEEP TREKKER introduced a new low‑light ROV for nocturnal inspection, while XYLEM INC expanded its water‑treatment portfolio with a sensor‑integrated filtration system. Recent mergers, such as INNOVASEA’s acquisition of a niche sensor firm, illustrate the ongoing consolidation and innovation drive.