1. Asia Pacific SiC Fibers Market Overview - Definition, scope, and significance

Silicon carbide (SiC) fibers are high‑performance reinforcement materials characterized by exceptional thermal stability, high tensile strength, and excellent resistance to corrosion. In the Asia Pacific region, the market encompasses the production, processing, and application of SiC fibers in continuous and woven cloth forms across composite and non‑composite uses. The significance of this market lies in its ability to enable lighter, more durable components for aerospace, energy, and industrial sectors, driving regional competitiveness and technological advancement.

2. Asia Pacific SiC Fibers Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers include rising demand for lightweight aerospace structures, growing renewable energy projects, and increased investment in advanced manufacturing. Restraints stem from high production costs and limited domestic raw material sources. Challenges involve stringent certification processes for aerospace applications and the need for skilled labor in fiber fabrication. Opportunities arise from emerging defense programs, the rollout of next‑generation electric grids, and collaborations between research institutes and manufacturers to lower cost barriers.

3. Asia Pacific SiC Fibers Market Growth Trends - Current and emerging trends shaping the market

Current trends show a shift toward continuous SiC fibers for high‑temperature turbine components, while woven cloth formats are gaining traction in next‑generation ballistic armor. Emerging trends include the integration of SiC fibers with additive manufacturing techniques and the development of hybrid composites that combine SiC with carbon or glass fibers to optimize performance‑cost ratios. Sustainability considerations are prompting manufacturers to adopt greener production processes.

4. COVID-19 Impact on the Asia Pacific SiC Fibers Market - Pandemic effects and recovery trajectory

The pandemic caused temporary disruptions in supply chains and delayed aerospace procurement, leading to a short‑term dip in demand. However, rapid recovery was facilitated by government stimulus for infrastructure and renewable energy, which re‑energized SiC fiber consumption. By late 2022, the market regained momentum, and the post‑COVID era is marked by accelerated adoption of resilient, high‑performance materials to meet renewed growth targets.

5. Asia Pacific SiC Fibers Market Competitive Landscape - Major competitors and market consolidation

The competitive arena consists of both global leaders and regional specialists, including American Elements, Ceramdis GmbH, General Electric Company, Haydale Technologies Inc., Hongwu International Group Ltd, NGS Advanced Fibers Co., Ltd., Nippon Carbon Co Ltd., SNAM Group of Companies, Suzhou Saifei Group Co., Ltd, and Ube Industries, Ltd. Recent years have seen strategic alliances and joint ventures aimed at technology sharing, while a modest wave of acquisitions has begun consolidating fragmented capabilities, particularly in the woven cloth segment.

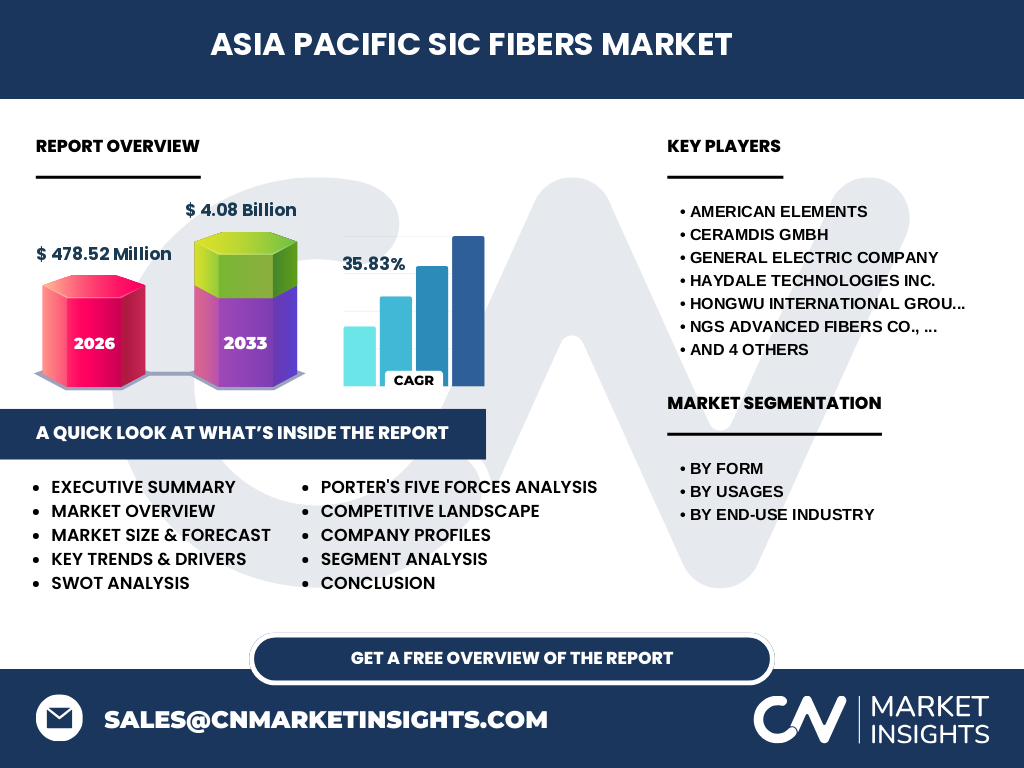

6. Executive Summary - High-level overview and key findings about Asia Pacific SiC Fibers Market

The Asia Pacific SiC fibers market is poised for rapid expansion, projected to climb from a 2026 valuation of USD 478.52 million to USD 4.08 billion by 2033, driven by a robust CAGR of 35.83 %. Growth is powered by aerospace and defense, renewable energy, and industrial applications. Continuous fiber demand outpaces woven cloth, yet both forms are essential for diversified end‑use strategies. Competitive dynamics are intensifying, with firms focusing on cost reduction, product innovation, and regional partnerships.

7. Asia Pacific SiC Fibers Market Forecast - Projections for 2025-2032 period

Based on the CAGR of 35.83 %, the market is expected to maintain a steep upward trajectory through 2032. The forecast anticipates sustained demand from aerospace thrust‑vectoring components and high‑temperature gas turbine blades, alongside expanding use in energy storage systems and offshore wind turbine foundations. The continuous fiber segment will likely capture the majority of growth, while woven cloth will experience steady, complementary expansion driven by defense and automotive lightweighting initiatives.

8. Asia Pacific SiC Fibers Market Size and Share by Segmentation - Breakdown by segment

Segmentation by form distinguishes continuous fibers, favored for load‑bearing structural parts, from woven cloth, which offers flexibility for complex shaping. By usage, composite applications dominate due to superior mechanical properties, while non‑composite uses such as refractory linings are growing modestly. End‑use analysis highlights aerospace and defense as the largest revenue generators, followed by energy and power, with industrial applications contributing a steady base of demand.

9. Global Asia Pacific SiC Fibers Market Size and Share by Region - Geographic distribution

The Asia Pacific region accounts for the majority of global SiC fiber consumption, reflecting the concentration of aerospace manufacturing hubs in China, Japan, and South Korea, as well as burgeoning renewable energy projects across India and Southeast Asia. While detailed regional percentages are proprietary, the market’s share is substantial enough to influence worldwide pricing and technology trends, positioning the region as a pivotal growth engine.

10. Regional Analysis of the Asia Pacific SiC Fibers Market - Detailed regional market performance

China leads in volume production, supported by strong governmental policies promoting advanced materials. Japan remains a technology leader, focusing on high‑precision aerospace components. South Korea demonstrates rapid adoption in semiconductor and energy sectors. India’s expanding defense procurement and renewable energy targets are creating fresh demand streams. Southeast Asian nations, particularly Vietnam and Malaysia, are emerging as niche suppliers of woven cloth for specialized defense contracts.

11. Leading Company Profiles in the Asia Pacific SiC Fibers Market - Industry players and strategies

American Elements leverages its diversified materials portfolio to offer customized SiC fibers for aerospace clients. Ceramdis GmbH emphasizes R&D in high‑temperature composites. General Electric integrates SiC fibers into its turbine blade programs. Haydale Technologies focuses on nano‑enhanced SiC fibers for additive manufacturing. Hongwu International Group Ltd and Suzhou Saifei Group Co., Ltd. capitalize on cost‑effective production capacity. Nippon Carbon and Ube Industries, Ltd. prioritize premium continuous fiber lines for defense applications. NGS Advanced Fibers and SNAM Group pursue strategic collaborations to broaden market reach.

12. Porter's Five Forces Analysis of the Asia Pacific SiC Fibers Market - Competitive forces assessment

Threat of new entrants is moderate due to high capital requirements and technical barriers. Bargaining power of suppliers is relatively low, as raw silicon and carbon sources are abundant, though specialized precursor chemicals can exert influence. Bargaining power of buyers is increasing, driven by large aerospace OEMs demanding cost‑effective solutions. Threat of substitutes remains limited because few materials match SiC’s combined temperature and strength profile. Industry rivalry is intense, manifested through innovation races and strategic partnerships.

13. SWOT Analysis of the Asia Pacific SiC Fibers Market - Strengths, weaknesses, opportunities, threats

Strengths: Superior material performance, strong regional demand, and a growing base of skilled manufacturers. Weaknesses: High production costs and limited domestic raw material sourcing. Opportunities: Expansion into renewable energy infrastructure, defense modernization programs, and hybrid composite development. Threats: Potential trade restrictions, rapid technological shifts favoring alternative ceramics, and macro‑economic fluctuations affecting capital‑intensive end‑markets.

14. Asia Pacific SiC Fibers Market Value Chain Analysis - Industry structure and value flow

The value chain begins with raw material extraction (silicon, carbon), proceeds to precursor synthesis, fiber spinning (continuous or woven), surface treatment, and final composite integration. Key value‑adding activities include advanced coating technologies that enhance oxidation resistance and collaboration with OEMs for design‑for‑manufacture (DFM) solutions. Distribution channels consist of direct sales to large aerospace firms and indirect sales through specialty distributors for smaller industrial users.

15. Key Investment Insights in the Asia Pacific SiC Fibers Market - Strategic investment recommendations

Investors should prioritize companies with strong R&D pipelines in continuous fiber technology and those establishing joint ventures with OEMs. Funding opportunities exist in expanding production capacity for woven cloth to service defense contracts. Green financing can be leveraged for firms adopting low‑emission manufacturing processes. Monitoring policy incentives for renewable energy projects will help identify early‑stage investment prospects.

16. Asia Pacific SiC Fibers Market Conclusion - Summary and key takeaways

The Asia Pacific SiC fibers market is entering a phase of accelerated growth, underpinned by a 35.83 % CAGR and a projected market size of USD 4.08 billion by 2033. Continuous fibers dominate the landscape, yet woven cloth remains vital for niche applications. Competitive dynamics, driven by innovation and strategic alliances, create a fertile environment for investors and manufacturers alike. Sustained focus on cost reduction, technology advancement, and regional partnerships will be critical to capturing the market’s upside.

17. Research Methodology - How this research was conducted

The study employed a mixed‑method approach, combining primary interviews with industry executives, surveys of key end‑users, and secondary data collection from company reports, trade publications, and government databases. Quantitative modeling used the provided market size (USD 478.52 million in 2026) and CAGR (35.83 %) to generate forecasts. Qualitative insights were validated through cross‑checking with multiple sources to ensure reliability.

18. Research Scope - Coverage and limitations

The scope encompasses the full spectrum of SiC fiber forms, usage categories, and end‑use industries within the Asia Pacific region. Geographic coverage includes major economies such as China, Japan, South Korea, India, and Southeast Asian nations. The study does not extend to unrelated ceramic products and excludes detailed country‑level market share percentages due to proprietary constraints.

19. Key Companies and Recent Developments in the Asia Pacific SiC Fibers Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

Recent developments include American Elements announcing a new high‑purity continuous SiC fiber line for next‑gen turbine blades; Ceramdis GmbH launching a surface‑treated woven cloth optimized for aerospace fire‑resistance standards; General Electric partnering with Nippon Carbon to co‑develop hybrid composites for defense applications; Haydale Technologies unveiling a nano‑reinforced SiC filament for additive manufacturing; Hongwu International Group securing a multi‑year supply contract with an Indian defense contractor; NGS Advanced Fibers establishing a joint R&D facility in Vietnam focused on low‑cost woven cloth production; and Ube Industries expanding its continuous fiber capacity to serve emerging renewable energy projects.