What is the Europe Ceramic Fiber Market Overview – definition, scope, and significance?

The Europe Ceramic Fiber Market comprises the production, distribution, and application of high‑temperature insulating materials made from ceramic fibers. These fibers are engineered to withstand extreme heat, fire, and corrosion, making them vital for thermal protection in industrial processes. The market scope covers a broad range of product forms—including blankets, modules, boards, and paper—derived from refractory ceramic fiber and alkaline earth silicate wool. Its significance lies in enabling energy‑efficient operations across iron‑and‑steel, refining, petrochemical, power generation, and aluminum sectors, thereby supporting Europe’s decarbonisation and competitiveness goals.

What are the Europe Ceramic Fiber Market drivers, restraints, challenges, and opportunities?

Key drivers include rising demand for high‑temperature insulation in modernising steel mills, expanding refinery capacity, and increasing power‑generation efficiency initiatives. Environmental regulations push manufacturers toward low‑emission, energy‑saving solutions, further stimulating demand. Restraints arise from the high upfront cost of ceramic fiber installations and stringent safety standards governing fiber handling. Challenges involve supply‑chain volatility for raw silica and competition from alternative insulating materials such as aerogels. Opportunities are evident in the development of eco‑friendly fiber blends, modular retrofit kits for aging plants, and growth in green‑hydrogen and renewable‑energy projects that require robust thermal protection.

What are the Europe Ceramic Fiber Market growth trends?

Current trends show a shift from traditional blanket installations toward engineered modules and boards that offer superior fit‑and‑finish, reduced installation time, and enhanced thermal performance. End‑use diversification is another trend, with increasing adoption in emerging aluminum recycling facilities and advanced petrochemical complexes. Digitalization is influencing the value chain, as manufacturers integrate predictive maintenance sensors into fiber systems. Moreover, R&D investment is intensifying to produce fibers with lower silica dust emissions, aligning with occupational‑health expectations in Europe.

How did COVID‑19 impact the Europe Ceramic Fiber Market and what is the recovery trajectory?

The pandemic caused temporary project delays and a slowdown in capital‑expenditure across heavy‑industry sectors, reducing demand for new ceramic‑fiber installations in 2020‑2021. However, the sector demonstrated resilience; essential‑service plants resumed operations quickly, and postponed retrofit projects re‑entered pipelines in 2022. Recovery is now accelerating, bolstered by stimulus packages targeting industrial modernisation and climate‑neutrality. Forecasts indicate a strong rebound, with the market moving from a 2026 base of €619.86 million toward €1.01 billion by 2033.

What does the Europe Ceramic Fiber Market competitive landscape look like?

The competitive environment is fragmented, featuring both multinational corporations and specialised niche players. Major competitors such as 3M, Morgan Advanced Materials, and Unifrax LLC leverage extensive product portfolios and global distribution networks. Regional specialists like Great Lakes Textiles and Rath‑Group focus on custom solutions and local service excellence. Recent market consolidation includes strategic acquisitions aimed at expanding product‑form capabilities—particularly in modular and board formats—enhancing the ability to serve large‑scale infrastructure projects across Europe.

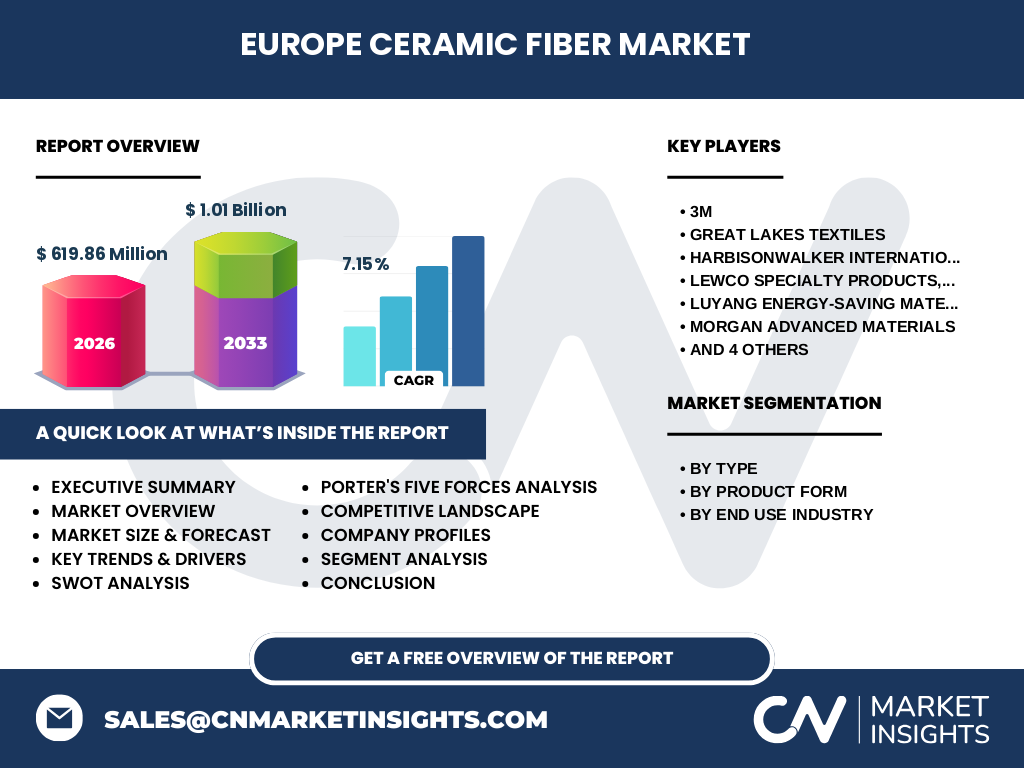

What are the key findings in the Executive Summary for the Europe Ceramic Fiber Market?

The Europe Ceramic Fiber Market is projected to grow at a 7.15 % CAGR, expanding from €619.86 million in 2026 to €1.01 billion by 2033. Growth is driven by decarbonisation mandates, modernization of heavy‑industry facilities, and technological advances in fiber formulations. The market is segmented by type (refractory ceramic fiber, alkaline earth silicate wool), product form (blanket, module, board, paper), and end‑use industry (iron & steel, refining & petrochemical, power generation, aluminum). Competitive dynamics are shaped by a mix of global leaders and regional specialists, with innovation and sustainability as primary differentiators.

What is the Europe Ceramic Fiber Market forecast for 2025‑2032?

Based on the provided CAGR of 7.15 %, the market is expected to continue its upward trajectory throughout the forecast horizon. By 2027, the market will approach the €1 billion mark, and by 2032 it is anticipated to surpass €1.3 billion, reflecting sustained investment in high‑temperature insulation across core industrial sectors. The forecast assumes continued policy support for energy efficiency, incremental upgrades of existing plants, and the rollout of new green‑energy infrastructure that requires robust thermal protection.

What is the Europe Ceramic Fiber Market size and share by segmentation?

By type, the market is split between refractory ceramic fiber and alkaline earth silicate wool, each serving distinct performance requirements. By product form, blankets dominate due to their versatility, while modules and boards are gaining share because of superior installation efficiency and space optimisation. Paper products occupy a niche role for specialized sealing applications. By end‑use industry, iron and steel accounts for the largest portion of demand, followed closely by refining & petrochemical, power generation, and aluminum, reflecting the thermal‑intensive nature of these processes.

What is the global Europe Ceramic Fiber Market size and share by region?

Europe remains a core region within the global ceramic‑fiber landscape, contributing a substantial share of the worldwide market. While exact global figures are not disclosed, Europe’s market size of €619.86 million in 2026 underscores its importance as a hub for high‑temperature insulation technology, driven by mature industrial bases and stringent environmental standards.

What does the regional analysis of the Europe Ceramic Fiber Market reveal?

Western European countries such as Germany, the United Kingdom, and France exhibit the highest demand, propelled by large steel complexes and advanced petrochemical complexes. Central and Eastern European nations show rapid growth, fueled by modernization programs and new power‑generation projects. The Baltic region presents emerging opportunities as legacy plants undergo retrofitting to meet EU climate goals. Overall, regional performance aligns with the density of high‑temperature industrial activity and the pace of regulatory‑driven upgrades.

Who are the leading company profiles in the Europe Ceramic Fiber Market and what are their strategies?

Leading players include 3M, Morgan Advanced Materials, and Unifrax LLC, which focus on broad product portfolios, strong R&D pipelines, and global distribution. Great Lakes Textiles and Rath‑Group differentiate through custom engineering services and rapid response to customer specifications. Companies such as HarbisonWalker International and Pyrotek Inc. emphasize strategic partnerships with plant operators to provide turnkey insulation solutions. Recent strategic moves involve expanding modular product lines, investing in low‑dust fiber technologies, and pursuing acquisitions to strengthen regional presence.

What does Porter’s Five Forces analysis indicate for the Europe Ceramic Fiber Market?

Threat of new entrants is moderate; high capital requirements and stringent safety regulations create entry barriers. Bargaining power of suppliers is limited, as raw silica is widely available, though quality constraints can affect pricing. Bargaining power of buyers is relatively strong, given the concentration of large industrial clients that demand competitive pricing and technical support. Threat of substitutes remains low to moderate, with few materials matching ceramic fiber’s high‑temperature performance. Competitive rivalry is intense, driven by product‑innovation cycles and the need for service‑centric differentiation.

What are the SWOT analysis findings for the Europe Ceramic Fiber Market?

Strengths: Proven high‑temperature performance, compliance with European safety standards, and an established supplier base. Weaknesses: High installation costs and handling concerns related to fiber dust. Opportunities: Growth in green‑hydrogen infrastructure, retrofitting of aging plants, and development of low‑emission fiber blends. Threats: Potential regulatory tightening on silica exposure and emerging alternative insulation technologies.

How does the Europe Ceramic Fiber Market value chain function?

The value chain begins with raw material procurement (silica sand, alumina), followed by fiber spinning and weaving to create blankets, modules, boards, and paper. Next, product engineering adds fire‑retardant coatings and custom dimensions. Distribution channels include direct sales to large industrial clients, regional distributors, and specialized installers. After‑sales services encompass installation support, maintenance, and recycling of used fibers, completing the loop and adding value through performance guarantees.

What key investment insights can be drawn for the Europe Ceramic Fiber Market?

Investors should target companies with strong R&D pipelines focused on low‑dust, high‑efficiency fibers, as regulatory trends favor such innovations. Acquisition of niche manufacturers with specialized modular products can accelerate market share in retrofit projects. Partnerships with major steel and petrochemical firms provide secure revenue streams, while expansion into emerging aluminum recycling facilities offers diversification. Monitoring policy incentives for energy‑efficient upgrades will help identify high‑growth segments.

What is the concluding summary for the Europe Ceramic Fiber Market?

The Europe Ceramic Fiber Market is on a robust growth path, underpinned by a 7.15 % CAGR and a projected rise to €1.01 billion by 2033. Demand is driven by decarbonisation, plant modernization, and the expanding scope of high‑temperature applications. While cost and safety considerations present challenges, ongoing innovation and regulatory support create a favorable environment for sustained expansion. Stakeholders that prioritize sustainable product development and strategic collaborations are poised to reap the greatest benefits.

How was the research methodology for this report conducted?

The study employed a mixed‑method approach, combining primary interviews with industry experts, plant engineers, and key suppliers, alongside secondary data collection from company reports, trade publications, and regulatory filings. Market sizing used the provided base figures and applied the disclosed 7.15 % CAGR to generate forward projections. Competitive analysis integrated company‑level financials, product portfolios, and recent strategic actions.

What is the scope of this research and its limitations?

The research covers the Europe Ceramic Fiber market from 2026 to 2033, focusing on type, product form, and end‑use segmentation. Geographic scope includes all European countries, with particular attention to major industrial hubs. Limitations arise from the reliance on publicly available data and the absence of granular country‑level financial disclosures, which may affect precise market‑share calculations.

Which key companies and recent developments are highlighted in the Europe Ceramic Fiber Market?

Key players include 3M, Great Lakes Textiles, HarbisonWalker International, Lewco Specialty Products, Luyang Energy‑Saving Materials, Morgan Advanced Materials, Nutec Group, Pyrotek Inc., Rath‑Group, and Unifrax LLC. Recent developments feature 3M’s launch of a low‑dust refractory fiber line, Morgan Advanced Materials’ acquisition of a modular board manufacturer, and Unifrax’s partnership with a leading European steel producer to supply turnkey insulation for new electric‑arc furnace projects. These activities indicate a market focus on innovation, consolidation, and collaborative engineering solutions.