North America SiC Fibers Market Overview - Definition, scope, and significance

Silicon carbide (SiC) fibers are high‑performance, ceramic‑based reinforcement materials known for exceptional tensile strength, high thermal conductivity, and excellent resistance to oxidation and corrosion. In the North American market, SiC fibers are employed across a broad range of applications, from aerospace structural components to power‑generation equipment and advanced industrial tooling. The market’s scope encompasses the entire value chain – raw material sourcing, fiber production (continuous and woven cloth forms), downstream processing, and end‑use integration. Its significance stems from the growing demand for lightweight, high‑temperature‑resilient composites that enable fuel‑efficient aircraft, more reliable turbines, and durable industrial systems, positioning SiC fibers as a strategic enabler of next‑generation technologies.

North America SiC Fibers Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

Key drivers include the rapid expansion of the aerospace and defense sector, which seeks weight‑reduction and higher‑temperature performance, and the rising investment in renewable energy and advanced power generation where SiC‑based composites improve efficiency and lifespan. Government incentives for clean energy and defense modernization further accelerate adoption. Restraints arise from the high manufacturing cost of SiC fibers and the limited number of qualified suppliers, which can delay project timelines. Technical challenges such as ensuring uniform fiber quality and integrating fibers into complex composite architectures also moderate growth. Opportunities exist in emerging markets like electric‑vehicle powertrain components and high‑temperature industrial processes, where SiC’s superior thermal properties can unlock new product designs and performance gains.

North America SiC Fibers Market Growth Trends - Current and emerging trends shaping the market

Current trends indicate a shift toward continuous‑form SiC fibers due to their superior load‑bearing capability and ease of automated lay‑up in aerospace structures. Simultaneously, woven cloth forms are gaining traction in niche industrial applications that demand flexible shaping. The market is also witnessing increased collaboration between fiber manufacturers and composite designers to develop proprietary resin systems optimized for SiC reinforcement. Emerging trends include the integration of SiC fibers in additive‑manufacturing (3D printing) of high‑temperature components, and the use of hybrid fiber systems that combine SiC with carbon or glass fibers to balance cost and performance.

COVID-19 Impact on the North America SiC Fibers Market - Pandemic effects and recovery trajectory

The COVID‑19 pandemic caused temporary disruptions in supply chains and delayed capital‑intensive projects, particularly in the aerospace sector. Manufacturing facilities faced workforce constraints, leading to reduced throughput in early 2020. However, the market demonstrated resilience; stimulus packages and the accelerated push for domestic defense production helped stabilize demand. By late 2021, recovery was evident as aerospace OEMs resumed production and energy projects regained momentum. The post‑pandemic period has seen a stronger emphasis on supply‑chain diversification, prompting North American firms to localize component sourcing, thereby supporting a robust rebound and setting the stage for accelerated growth.

North America SiC Fibers Market Competitive Landscape - Major competitors and market consolidation

The competitive arena is defined by a mix of established industrial players and specialized ceramics firms. Leading companies such as American Elements, COI Ceramics, Inc., and General Electric Company dominate the continuous‑fiber segment, leveraging extensive R&D capabilities and integrated manufacturing. Specialty Materials, Inc. and Haydale Technologies Inc. focus on niche woven‑cloth applications and custom composite solutions. Recent consolidation activity includes strategic partnerships aimed at expanding distribution networks across the United States and Canada, as well as joint development agreements to co‑create advanced resin‑fiber systems. While the market remains fragmented, a trend toward collaborative alliances is evident as firms seek to combine technical expertise and broaden market reach.

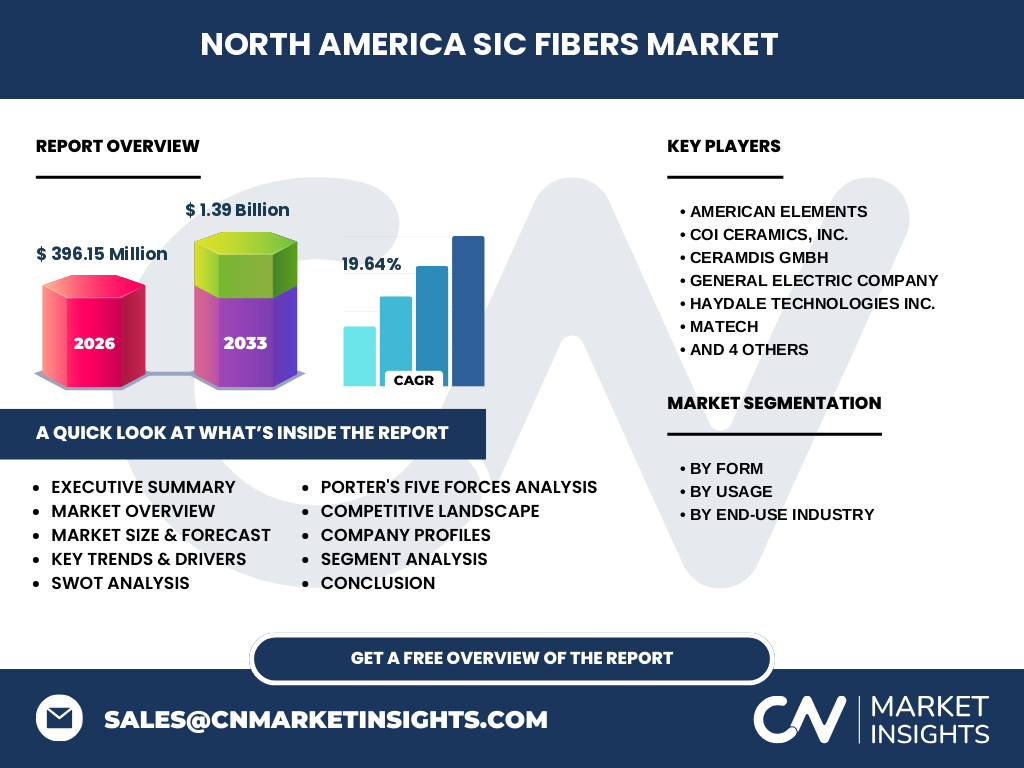

Executive Summary - High-level overview and key findings about North America SiC Fibers Market

The North America SiC Fibers market is valued at USD 396.15 million in 2026 and is projected to reach USD 1.39 billion by 2033, achieving a CAGR of 19.64 %. Growth is propelled by strong demand from aerospace & defense, energy & power, and industrial sectors, with continuous fibers leading the segment mix. Market dynamics reveal robust opportunities in high‑temperature composites and hybrid material systems, while cost and supply‑chain constraints remain focal challenges. Competitive intensity is marked by technology‑driven differentiation and strategic collaborations, positioning the market for sustained expansion throughout the forecast horizon.

North America SiC Fibers Market Forecast - Projections for 2025-2032 period

Building on the 2026 baseline, the market is expected to maintain a high growth trajectory through 2032, driven by escalating aerospace programs, renewable‑energy infrastructure roll‑outs, and industrial modernization initiatives. The forecast anticipates continued double‑digit compound annual growth, reinforcing the projected USD 1.39 billion market size by 2033. Continuous‑form fibers are forecasted to capture the majority of incremental demand, while woven‑cloth applications will experience modest yet steady expansion, especially in specialized industrial niches.

North America SiC Fibers Market Size and Share by Segmentation - Breakdown by segment

By form, the market divides into continuous and woven cloth fibers. Continuous fibers hold a larger share owing to their superior mechanical properties and prevalence in aerospace composite lay‑up processes. By usage, the composites category dominates, reflecting the primary role of SiC fibers as reinforcement in high‑performance matrix systems; the non‑composites segment includes applications such as thermal management and wear‑resistant coatings. End‑use industry segmentation shows aerospace and defense as the leading sector, followed by energy and power, with industrial applications representing a growing but smaller portion of the market.

Global North America SiC Fibers Market Size and Share by Region - Geographic distribution

While the report focuses on North America, the region contributes a substantial portion of global SiC fiber consumption, driven by the concentration of aerospace OEMs, defense contractors, and advanced energy projects in the United States and Canada. The market’s growth aligns with broader global trends, positioning North America as a key demand hub that influences worldwide production planning and capacity expansion.

Regional Analysis of the North America SiC Fibers Market - Detailed regional market performance

Within North America, the United States accounts for the lion’s share of demand, underpinned by major aerospace programs (e.g., next‑generation fighter jets and commercial airliners) and significant defense spending. Canada, while smaller, exhibits steady growth driven by its renewable‑energy sector and participation in joint defense procurement initiatives. Regional performance is bolstered by supportive government policies, robust research institutions, and a well‑established supply chain ecosystem that together sustain market momentum.

Leading Company Profiles in the North America SiC Fibers Market - Industry players and strategies

Key players include:

American Elements – focuses on high‑purity SiC fiber production for aerospace composites, leveraging advanced powder‑processing technologies.

COI Ceramics, Inc. – offers a broad portfolio of continuous SiC fibers, emphasizing custom length and diameter specifications to meet specific OEM requirements.

General Electric Company – integrates SiC fibers into its gas‑turbine and power‑generation products, highlighting performance benefits in high‑temperature environments.

Haydale Technologies Inc. – specializes in functionalized SiC woven fabrics, targeting niche industrial applications and partnering with resin manufacturers for optimized composite systems.

These companies pursue strategies such as R&D investment, strategic partnerships, and expansion of production capacity to capture emerging demand.

Porter's Five Forces Analysis of the North America SiC Fibers Market - Competitive forces assessment

Threat of new entrants: Moderate – high capital requirements and specialized expertise create barriers, but emerging niche players could enter via innovative manufacturing approaches.

Bargaining power of suppliers: High – limited number of raw‑material suppliers for high‑purity silicon carbide increases supplier leverage.

Bargaining power of buyers: Moderate – large aerospace and defense customers negotiate volume contracts, yet the unique performance of SiC fibers limits substitute options.

Threat of substitutes: Low – alternative reinforcement materials (e.g., carbon fiber) cannot match the high‑temperature capability of SiC in many applications.

Industry rivalry: High – competitive differentiation is driven by product quality, customization, and value‑added services, leading to intense rivalry among established firms.

SWOT Analysis of the North America SiC Fibers Market - Strengths, weaknesses, opportunities, threats

Strengths: Superior material performance, strong demand from high‑value aerospace and energy sectors, and a well‑developed technical ecosystem.

Weaknesses: High production costs, limited supplier base, and complex processing requirements.

Opportunities: Expansion into electric‑vehicle powertrain components, hybrid fiber systems, and additive‑manufacturing of high‑temperature parts.

Threats: Potential supply‑chain disruptions, price pressure from emerging low‑cost alternatives, and regulatory changes affecting defense procurement.

North America SiC Fibers Market Value Chain Analysis - Industry structure and value flow

The value chain begins with raw‑material extraction (silicon and carbon sources) followed by high‑temperature synthesis of SiC powders. These powders are then processed into continuous filaments or woven cloths through chemical vapor deposition and subsequent drawing or weaving steps. Mid‑stream activities include surface treatments and functionalization to enhance fiber–matrix bonding. Downstream, OEMs incorporate the fibers into composite lay‑ups, cure them into final structures, and perform testing and certification. Support functions such as engineering services, logistical support, and after‑market technical assistance add further value.

Key Investment Insights in the North America SiC Fibers Market - Strategic investment recommendations

Investors should consider allocating capital toward companies expanding continuous‑fiber capacity, as this segment commands the largest market share and benefits from economies of scale. Funding joint development projects that pair SiC fibers with next‑generation resin systems can unlock higher‑margin composite solutions. Additionally, strategic stakes in firms pursuing hybrid fiber technologies or additive‑manufacturing capabilities can diversify exposure and capture emerging application niches.

North America SiC Fibers Market Conclusion - Summary and key takeaways

The North America SiC Fibers market is on a rapid growth trajectory, moving from a USD 396.15 million base in 2026 to an estimated USD 1.39 billion by 2033, driven by a 19.64 % CAGR. Continuous fibers dominate, powered by aerospace, defense, and energy demands, while woven cloths serve specialized industrial roles. Despite cost and supply challenges, the market offers compelling opportunities through hybrid materials, additive manufacturing, and expanding renewable‑energy infrastructure. Stakeholders who invest in capacity, innovation, and strategic collaborations are well‑positioned to capture value in this high‑growth segment.

Research Methodology - How this research was conducted

The study employed a mixed‑method approach, combining primary interviews with industry executives, technical experts, and key buyers, alongside secondary data collection from company reports, trade publications, and governmental databases. Quantitative data were validated through triangulation, and forecasting employed compound annual growth rate (CAGR) calculations based on historic trends and projected demand drivers. Competitive analysis incorporated Porter’s Five Forces and SWOT frameworks to contextualize market dynamics.

Research Scope - Coverage and limitations

The scope covers the North American SiC fibers market, focusing on product forms (continuous, woven cloth), usage (composites, non‑composites), and end‑use industries (aerospace & defense, energy & power, industrial). Geographic coverage includes the United States and Canada. While the study leverages the most recent data available, it does not extend to detailed country‑level breakdowns beyond the two primary markets due to data availability constraints.

Key Companies and Recent Developments in the North America SiC Fibers Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

Recent developments include American Elements announcing a new line of ultra‑high‑purity continuous SiC fibers tailored for next‑generation hypersonic vehicles. COI Ceramics, Inc. launched a customized short‑length fiber product to address niche defense applications. General Electric Company disclosed a partnership with a leading turbine manufacturer to integrate SiC‑reinforced composites into its latest gas‑turbine series, promising efficiency gains. Haydale Technologies Inc. introduced a functionalized woven‑cloth platform designed for rapid‑cure resin systems, targeting the industrial wear‑resistant market. These activities underscore the sector’s focus on product innovation, strategic alliances, and market expansion.