1. What is the North America Medical Equipment Maintenance Market Overview – Definition, scope, and significance?

The North America Medical Equipment Maintenance Market encompasses all services required to keep medical devices operational, safe, and compliant with regulatory standards. This includes preventive, corrective, and operational maintenance performed by original equipment manufacturers (OEMs), independent service organizations, and in‑house teams. The scope covers a broad range of device categories such as electromedical equipment, endoscopic devices, surgical instruments, and other medical equipment used in hospitals, clinics, and ambulatory care settings. The market’s significance lies in its direct impact on patient safety, equipment uptime, and cost efficiency for healthcare providers, ensuring that high‑value assets deliver reliable performance throughout their lifecycle.

2. What are the key drivers, restraints, challenges, and opportunities in the North America Medical Equipment Maintenance Market?

Key drivers include rising healthcare expenditure, increasing adoption of advanced medical technologies, and stringent regulatory requirements mandating regular maintenance. The expanding network of outpatient facilities and the growing emphasis on preventive care further boost demand. Restraints stem from high service costs and budgetary pressures in some healthcare systems. Challenges involve a shortage of skilled technicians and complex regulatory compliance across device types. Opportunities arise from the digital transformation of maintenance services—such as predictive analytics, IoT‑enabled remote monitoring, and service contracts that bundle value‑added offerings, creating new revenue streams for providers.

3. What current and emerging growth trends are shaping the North America Medical Equipment Maintenance Market?

Current trends feature a shift toward contract‑based service models, with healthcare providers preferring long‑term agreements that guarantee equipment uptime. Emerging trends include the integration of artificial intelligence for condition‑based monitoring, the use of digital twins to simulate device performance, and the adoption of cloud‑based maintenance platforms that streamline scheduling and documentation. Additionally, a noticeable movement toward sustainability—through equipment refurbishment and eco‑friendly disposal—adds a new dimension to service strategies.

4. How has COVID‑19 impacted the North America Medical Equipment Maintenance Market and what is the recovery trajectory?

The COVID‑19 pandemic initially disrupted routine maintenance schedules due to lockdowns and redeployment of service staff to critical care. however, the crisis also highlighted the essential nature of reliable equipment, prompting hospitals to accelerate maintenance contracts and invest in remote monitoring capabilities. As the healthcare system stabilizes, the market is experiencing a strong recovery, driven by backlog mitigation, heightened awareness of equipment reliability, and continued investment in pandemic‑resilient service models.

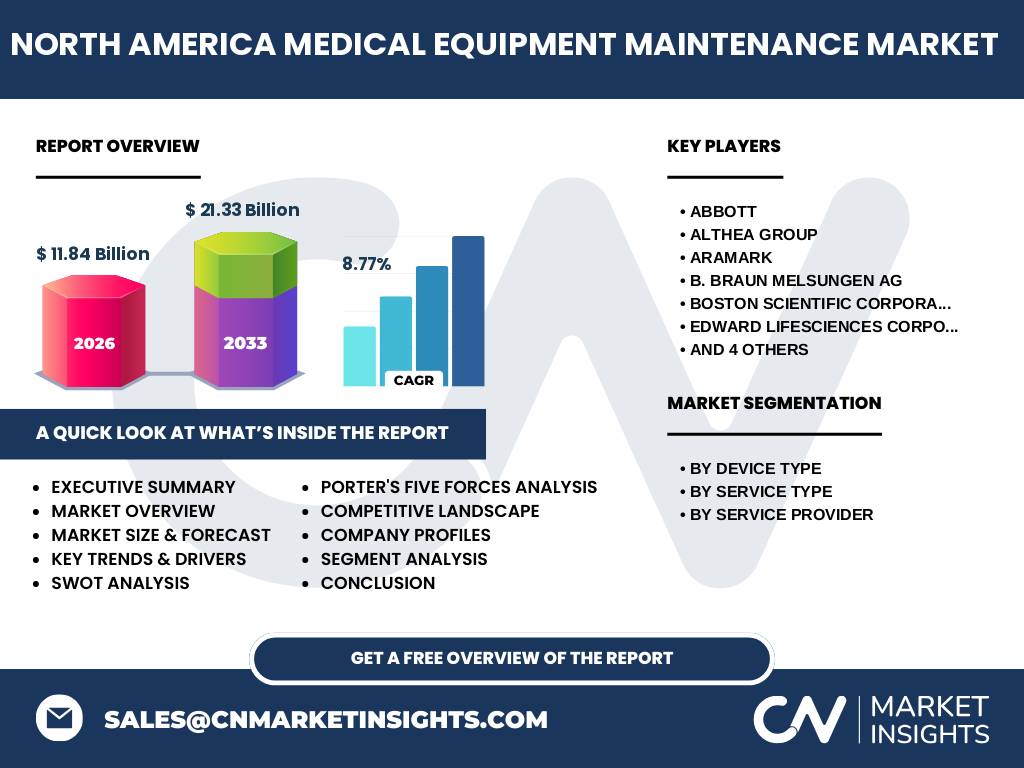

5. Who are the major competitors and what is the state of market consolidation in the North America Medical Equipment Maintenance Market?

Prominent players include Abbott, Althea Group, Aramark, B. Braun Melsungen AG, Boston Scientific Corporation, Edwards Lifesciences Corporation, Johnson & Johnson Services, Inc., Medtronic, Stryker, and Terumo Corporation. The market exhibits moderate consolidation, with OEMs leveraging their brand and technical expertise to capture service contracts, while independent service organizations compete on cost efficiency and flexibility. Strategic partnerships and acquisitions are common as firms aim to broaden service portfolios and geographical reach.

6. What are the high‑level findings presented in the Executive Summary of the North America Medical Equipment Maintenance Market?

The executive summary underscores a robust market size of $11.84 billion in 2026, with a projected increase to $21.33 billion by 2033, reflecting a CAGR of 8.77 %. Growth is anchored by expanding healthcare infrastructure, the adoption of complex medical devices, and a shift toward service‑oriented revenue models. Competitive dynamics are shaped by OEM dominance, the rise of independent service providers, and increasing digitization of maintenance processes. The outlook points to sustained expansion, driven by technology‑enabled services and evolving regulatory landscapes.

7. What are the forecasted market projections for the North America Medical Equipment Maintenance Market from 2025 to 2032?

Based on the provided figures, the market is expected to grow from its 2026 baseline of $11.84 billion to $21.33 billion by the end of the forecast horizon in 2033, delivering an average annual growth rate of 8.77 %. This trajectory suggests steady acceleration, with each successive year adding roughly $1.3‑$1.5 billion in incremental market value, driven by expanding service contracts, technology adoption, and continued investment in equipment reliability.

8. How is the North America Medical Equipment Maintenance Market sized and shared across its segmentation?

Segmentation by device type divides the market among electromedical equipment, endoscopic devices, surgical instruments, and other medical equipment. By service type, the split is between preventive maintenance and corrective/operational maintenance. Service provider segmentation includes OEMs, independent service organizations, and in‑house maintenance teams. While exact monetary shares are not disclosed, each segment reflects distinct demand patterns—preventive maintenance generally commands higher contract value due to its proactive nature, and OEMs typically hold a strong share in electromedical equipment services, whereas independent providers are active across endoscopic and surgical instrument segments.

9. What is the geographic distribution of the North America Medical Equipment Maintenance Market globally?

The market is centered in North America, which includes the United States, Canada, and Mexico. Within this region, the United States represents the largest contributor due to its extensive hospital network and advanced medical technology adoption. Canada and Mexico offer growing opportunities, supported by healthcare modernization initiatives and increasing private‑sector investment.

10. What does the regional analysis reveal about the performance of the North America Medical Equipment Maintenance Market?

Regional analysis highlights the United States as the primary growth engine, driven by high hospital density, strong reimbursement frameworks, and aggressive equipment upgrade cycles. Canada shows steady growth, propelled by public‑sector funding and a focus on maintaining equipment longevity. Mexico’s market is emerging, with rising private healthcare facilities seeking reliable maintenance solutions. Overall, the region benefits from a mature regulatory environment and a collaborative ecosystem among manufacturers, service firms, and healthcare providers.

11. Which companies lead the North America Medical Equipment Maintenance Market and what are their core strategies?

Leading firms such as Abbott, Medtronic, and Johnson & Johnson Services leverage their OEM advantage to bundle maintenance with equipment sales, emphasizing integrated service contracts and digital support platforms. Independent players like Althea Group and Aramark focus on cost‑effective solutions, flexible service tiers, and rapid response capabilities. Companies such as Stryker and Boston Scientific expand their service footprints through strategic acquisitions and partnerships, while B. Braun Melsungen AG emphasizes high‑quality preventive programs for critical care devices.

12. How do Porter’s Five Forces shape the competitive environment of the North America Medical Equipment Maintenance Market?

Threat of new entrants is moderate; high capital requirements and regulatory expertise create barriers, yet niche independent service firms can enter specialized segments. Bargaining power of buyers is strong, as hospitals negotiate multi‑year contracts and demand cost transparency. Bargaining power of suppliers leans toward OEMs, who control proprietary parts and technical knowledge. Threat of substitutes is low, because equipment downtime cannot be replaced by alternatives. Rivalry among existing competitors is intense, driven by price competition, service differentiation, and technology integration.

13. What are the SWOT insights for the North America Medical Equipment Maintenance Market?

Strengths: Robust demand, high equipment value, regulatory mandates. Weaknesses: Skilled labor shortage, cost pressures for providers. Opportunities: Predictive maintenance, IoT integration, service contract bundling, sustainability initiatives. Threats: Economic fluctuations affecting capital spending, potential regulatory changes, and competitive price wars.

14. How does the value chain of the North America Medical Equipment Maintenance Market operate?

The value chain starts with equipment manufacturers supplying devices and technical documentation. Service providers—OEMs, independent firms, and in‑house teams—perform scheduled preventive work, emergency corrective repairs, and operational support. Supporting activities include parts logistics, training of technicians, and data analytics platforms that feed performance metrics back to manufacturers for product improvement. End‑users (hospitals, clinics) close the loop by providing usage data and feedback on service quality.

15. What key investment insights can be derived for stakeholders interested in the North America Medical Equipment Maintenance Market?

Investors should focus on companies that are advancing digital maintenance solutions, as predictive analytics promise cost savings and higher contract renewal rates. Partnerships between OEMs and technology firms can accelerate market penetration. Acquisitions of niche independent service providers offer immediate access to specialized expertise and customer bases. Moreover, targeting sustainable service models—such as equipment refurbishment—aligns with emerging regulatory incentives and can differentiate portfolios.

16. What are the main conclusions and takeaways from the North America Medical Equipment Maintenance Market analysis?

The market is on a clear growth path, moving from a $11.84 billion base in 2026 to $21.33 billion by 2033, driven by an 8.77 % CAGR. Demand is reinforced by technology adoption, regulatory pressures, and an evolving service mindset among healthcare providers. Competitive dynamics favor firms that combine technical expertise with digital tools. Strategic focus on predictive maintenance, sustainability, and flexible contract structures will be essential for capturing future value.

17. How was the research methodology designed for this market study?

The study employed a mixed‑method approach, combining primary interviews with industry executives, service technicians, and procurement leaders, together with secondary data from company filings, regulatory reports, and reputable market databases. Quantitative projections were derived using time‑series analysis anchored on the provided market size and CAGR, while qualitative insights stemmed from trend analysis and expert validation.

18. What is the scope of this research and its limitations?

The research covers the North America region, focusing on maintenance services for electromedical equipment, endoscopic devices, surgical instruments, and other medical equipment. It examines preventive, corrective, and operational maintenance across OEMs, independent service organizations, and in‑house teams. Limitations include the exclusion of detailed country‑level financial breakdowns beyond the United States, Canada, and Mexico, and the reliance on publicly available information for competitive positioning.

19. Which key companies have recent developments, and what are their notable announcements in the North America Medical Equipment Maintenance Market?

Recent developments include Abbott expanding its remote monitoring platform for cardiac devices, Medtronic launching a predictive maintenance service using AI‑driven analytics, and Johnson & Johnson Services signing multi‑year contracts with major hospital systems to integrate IoT sensors into equipment service plans. Stryker announced a strategic acquisition of a boutique endoscopic maintenance firm to strengthen its service capabilities, while Althea Group introduced a subscription‑based maintenance model that bundles parts, labor, and analytics for surgical instruments.