North America Bread Market Overview - Definition, scope, and significance?

The North America Bread Market encompasses the production, distribution, and consumption of a broad range of baked grain products across the United States, Canada, and Mexico. It includes conventional and organic breads, various product types such as loaves, baguettes, rolls, burger buns, sandwich bread, and ciabatta, and distribution channels ranging from hypermarkets and supermarkets to convenience stores and online platforms. Bread remains a staple food, providing essential carbohydrates and serving as a versatile base for meals, which makes the market a cornerstone of the region’s food industry and a key indicator of consumer dietary trends.

North America Bread Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising disposable incomes, urbanization, and an increasing demand for convenient, ready‑to‑eat meals, which boost sales of pre‑sliced and specialty breads. Health‑conscious consumers spur growth in the organic segment, while innovation in functional ingredients (e.g., high‑fiber, protein‑enriched breads) creates new demand. Restraints stem from fluctuating wheat commodity prices and growing concerns over gluten‑related health issues, which can limit consumption of traditional wheat breads. Challenges involve supply‑chain disruptions and the need for sustainable packaging. Opportunities arise from expanding e‑commerce channels, product diversification into gluten‑free and low‑carb varieties, and strategic partnerships that enable broader market reach.

North America Bread Market Growth Trends - Current and emerging trends shaping the market?

Current trends feature a strong shift toward organic bread, driven by consumer preference for clean‑label products. Artisan and specialty breads such as ciabatta and sourdough are gaining traction in premium segments. Digital transformation is evident as online grocery sales accelerate, prompting bakeries to develop direct‑to‑consumer models. Additionally, functional breads fortified with vitamins, minerals, or probiotics are emerging, reflecting the intersection of nutrition and convenience. Seasonal and limited‑edition flavors also create buzz and drive trial purchases.

COVID-19 Impact on the North America Bread Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic initially disrupted supply chains, leading to temporary shortages of raw materials and labor. However, panic buying and increased home cooking sharply boosted demand for packaged bread, particularly loaves and sandwich bread sold through supermarkets. The convenience channel suffered as foot traffic declined, while online sales surged. Post‑pandemic, the market has stabilized with a sustained higher baseline for e‑commerce, and consumer habits have shifted toward healthier, longer‑shelf‑life products, supporting steady recovery.

North America Bread Market Competitive Landscape - Major competitors and market consolidation?

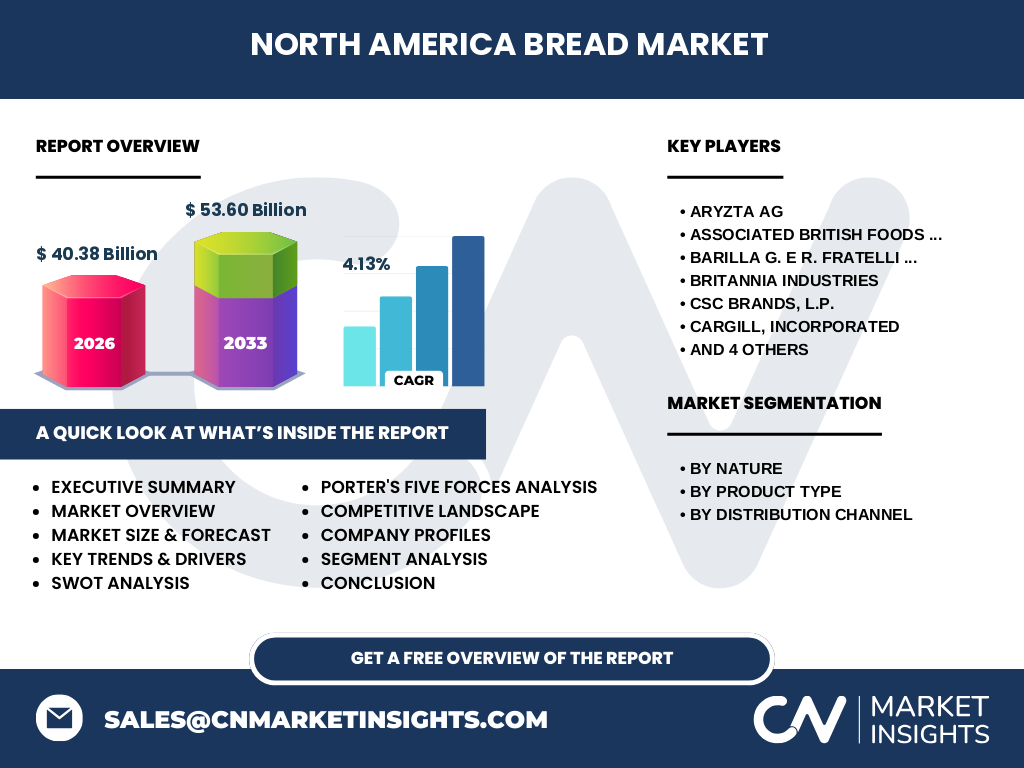

The market is moderately consolidated, featuring multinational players such as Aryllo AG, Associated British Foods plc, Barilla G. e R. Fratelli S.p.A, Britannia Industries, CSC Brands L.P., Cargill, Incorporated, Conagra Inc., Finsbury Food Group Plc, Premier Foods Group Limited, and Rich Products Corporation. These firms compete on product innovation, brand portfolio breadth, and distribution reach. Recent consolidation activities include strategic acquisitions of specialty bakeries to expand organic and specialty product lines, reinforcing the competitive pressure on smaller regional producers.

Executive Summary - High-level overview and key findings about North America Bread Market?

The North America Bread Market is valued at USD 40.38 billion in 2026 and is projected to reach USD 53.60 billion by 2033, registering a CAGR of 4.13% over the forecast period. Growth is propelled by consumer demand for convenience, health‑focused organic options, and functional breads. E‑commerce and premium artisan segments present significant upside, while raw material volatility and health‑related consumer concerns remain challenges. The competitive field is led by ten major multinational firms actively pursuing innovation and strategic acquisitions.

North America Bread Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 4.13%, the market is expected to expand from its 2026 base of USD 40.38 billion to approximately USD 53.60 billion by 2033. This steady growth reflects incremental gains each year, driven by expanding organic and functional product lines, continued strength in the hyper‑market and online distribution channels, and ongoing consumer shift toward healthier, convenient bread options.

North America Bread Market Size and Share by Segmentation - Breakdown by segment?

The market segmentation spans three dimensions. By nature, the conventional segment dominates, while organic breads capture a fast‑growing niche driven by health trends. By product type, loaves and sandwich bread hold the largest share due to everyday consumption, followed by rolls and burger buns that benefit from the fast‑food ecosystem. Baguettes and ciabatta cater to premium and artisan niches. Distribution channels are led by hypermarkets and supermarkets, with convenience stores and online channels gaining momentum, especially for specialty and organic lines.

Global North America Bread Market Size and Share by Region - Geographic distribution?

Geographically, the United States accounts for the majority of the market’s volume, reflecting its large population and extensive retail network. Canada contributes a significant share through strong demand for premium and organic products, while Mexico offers growth potential driven by urbanization and increasing middle‑class consumption. The regional distribution aligns with the overall market size of USD 40.38 billion in 2026, with each country’s share proportionate to its economic scale and bread consumption patterns.

Regional Analysis of the North America Bread Market - Detailed regional market performance?

In the United States, the hypermarket and supermarket channel leads, backed by robust e‑commerce penetration that accelerates online bread sales. The organic segment outperforms conventional growth rates, especially in health‑focused metro areas. Canada shows a higher per‑capita consumption of specialty breads like ciabatta and artisan loaves, reflecting premiumization trends. Mexico’s market is characterized by rapid expansion in convenience stores, driven by on‑the‑go lifestyles and a growing fast‑food sector that fuels demand for burger buns and rolls.

Leading Company Profiles in the North America Bread Market - Industry players and strategies?

Aryzta AG leverages its global bakery network to introduce organic product lines across North America. Associated British Foods plc focuses on premium brands and strategic acquisitions of artisanal bakeries. Barilla emphasizes product diversification, launching high‑fiber and gluten‑free breads. Britannia Industries expands its presence through partnerships with retail chains, while CSC Brands L.P. strengthens its private‑label offerings. Cargill, Incorporated utilizes its supply‑chain expertise to manage wheat sourcing cost‑effectively. Conagra Inc. integrates bread into its broader food portfolio, targeting convenience channels. Rich Products Corporation drives innovation in frozen bakery items, supporting the fast‑food segment.

Porter's Five Forces Analysis of the North America Bread Market - Competitive forces assessment?

Threat of New Entrants: Moderate; high capital requirements and established distribution networks create barriers, yet niche organic and gluten‑free brands can enter through e‑commerce. Bargaining Power of Suppliers: High, due to reliance on wheat and other grains whose prices are volatile. Bargaining Power of Buyers: Strong, as retail giants negotiate tight margins and demand product differentiation. Threat of Substitutes: Low to moderate; alternative carbohydrate sources (e.g., wraps, rice cakes) exist but do not fully replace bread. Industry Rivalry: Intense, with ten major players competing on innovation, brand loyalty, and channel reach.

SWOT Analysis of the North America Bread Market - Strengths, weaknesses, opportunities, threats?

Strengths: Established consumer staple, diverse product portfolio, strong retail infrastructure.

Weaknesses: Sensitivity to wheat price fluctuations, limited differentiation in conventional segment.

Opportunities: Expansion of organic and functional breads, growth of online sales, product innovation (gluten‑free, high‑protein).

Threats: Health concerns over gluten and carbohydrates, increasing competition from alternative snack foods, regulatory pressures on labeling and nutrition.

North America Bread Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with agricultural suppliers providing wheat, oats, and alternative grains. Milling transforms raw grains into flour, which is then processed by bakeries into various bread types. Packaging firms add protective, often sustainable, packaging solutions. Distribution follows, with large retailers (hypermarkets, supermarkets) handling the majority of volume, while convenience stores and online platforms capture niche and fast‑moving segments. End‑consumers purchase through physical stores or digital channels, completing the chain. Key value‑adding activities include product formulation, branding, and logistics optimization.

Key Investment Insights in the North America Bread Market - Strategic investment recommendations?

Investors should prioritize companies with strong organic and functional product pipelines, as these segments demonstrate the highest growth potential. Acquiring or partnering with specialty bakeries can accelerate entry into premium niches. Funding e‑commerce capabilities and data‑driven demand forecasting will enhance market reach. Additionally, investments in sustainable packaging and supply‑chain resilience can mitigate raw‑material cost risks and align with consumer expectations for environmentally responsible brands.

North America Bread Market Conclusion - Summary and key takeaways?

The North America Bread Market is on a clear growth trajectory, moving from USD 40.38 billion in 2026 to an estimated USD 53.60 billion by 2033, fueled by a 4.13% CAGR. Health‑driven organic and functional breads, along with expanding online distribution, are the primary engines of expansion. While raw‑material volatility and health‑related consumer concerns pose challenges, strategic innovation, channel diversification, and consolidation among leading players position the market for sustained profitability.

Research Methodology - How this research was conducted?

The research combined primary interviews with industry executives, retailers, and supply‑chain experts with secondary data from company reports, government publications, and reputable market databases. Trend analysis leveraged historical sales data and pricing information, while forecasting applied the disclosed CAGR of 4.13% to extrapolate future market size. Segmentation and competitive assessments were validated through cross‑referencing multiple data sources to ensure accuracy.

Research Scope - Coverage and limitations?

The scope covers the North America Bread Market, including conventional and organic breads, a range of product types, and three primary distribution channels (hypermarkets & supermarkets, convenience & retail stores, online). Geographic coverage includes the United States, Canada, and Mexico. The study does not extend to adjacent bakery categories such as pastries or gluten‑free snacks, and it relies exclusively on the financial figures provided for market size and growth.

Key Companies and Recent Developments in the North America Bread Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Aryzta AG recently launched a line of certified organic sourdough loaves across major U.S. supermarket chains. Associated British Foods plc announced the acquisition of a boutique Canadian artisanal bakery to expand its premium portfolio. Barilla introduced high‑protein sandwich bread targeting fitness‑focused consumers. Britannia Industries entered into a strategic partnership with a leading online grocery platform to boost its digital presence. CSC Brands L.P. expanded its private‑label capabilities for convenience stores. Cargill, Incorporated announced a sustainability initiative to source 30% of its wheat from regenerative farms by 2028. Conagra Inc. rolled out a new frozen burger bun range for the food‑service sector. Rich Products Corporation debuted a line of gluten‑free frozen ciabatta for fast‑food operators.