What is the North America Dental Implants Market Overview – definition, scope, and significance?

The North America Dental Implants Market encompasses the production, distribution, and clinical application of permanent tooth‑replacement solutions within the United States, Canada, and Mexico. It includes a broad range of products such as dental bridges, crowns, dentures, abutments, and implants made from titanium or zirconium, as well as the services provided by hospitals, dental clinics, and dental laboratories. The market is significant because it addresses the growing prevalence of tooth loss due to aging populations, periodontal disease, and lifestyle factors, while also reflecting advances in biomaterials and digital dentistry that improve patient outcomes and procedural efficiency.

What are the main drivers, restraints, challenges, and opportunities shaping the North America Dental Implants Market?

Key drivers include rising geriatric demographics, increasing disposable income, and heightened aesthetic awareness, all of which boost demand for permanent, natural‑looking tooth replacements. Technological progress—particularly in CAD/CAM and 3D printing—enhances precision and reduces treatment time, further stimulating adoption. Restraints stem from high procedural costs and limited insurance coverage, which can deter price‑sensitive patients. Regulatory compliance and the need for skilled clinicians present operational challenges. Opportunities arise from the expanding use of zirconium implants that combine strength with superior aesthetics, and from growing partnerships between implant manufacturers and dental laboratories that streamline supply chains and foster product innovation.

What growth trends are currently influencing the North America Dental Implants Market?

The market is experiencing a shift toward customized, patient‑specific solutions enabled by digital imaging and additive manufacturing. Growth in minimally invasive surgical techniques, such as flap‑less implant placement, is also notable. Alongside product innovation, there is increased adoption of bundled service models where manufacturers provide training, maintenance, and financing options, encouraging clinics to upgrade their offerings. The trend toward integrated digital workflows—combining intra‑oral scanning, virtual planning, and guided surgery—is reshaping clinical practice and driving higher implant success rates.

How did COVID‑19 affect the North America Dental Implants Market and what is the recovery trajectory?

The pandemic caused a temporary decline in elective dental procedures, including implant placements, due to lockdowns and patient concerns about aerosol‑generating treatments. However, the sector rebounded quickly as clinics adopted enhanced infection‑control protocols and tele‑consultation tools. Post‑COVID recovery is robust, supported by pent‑up demand and an accelerated interest in long‑term oral health solutions. The market’s resilience is underlined by a strong upward trajectory that aligns with the projected CAGR of 7.89% through 2032.

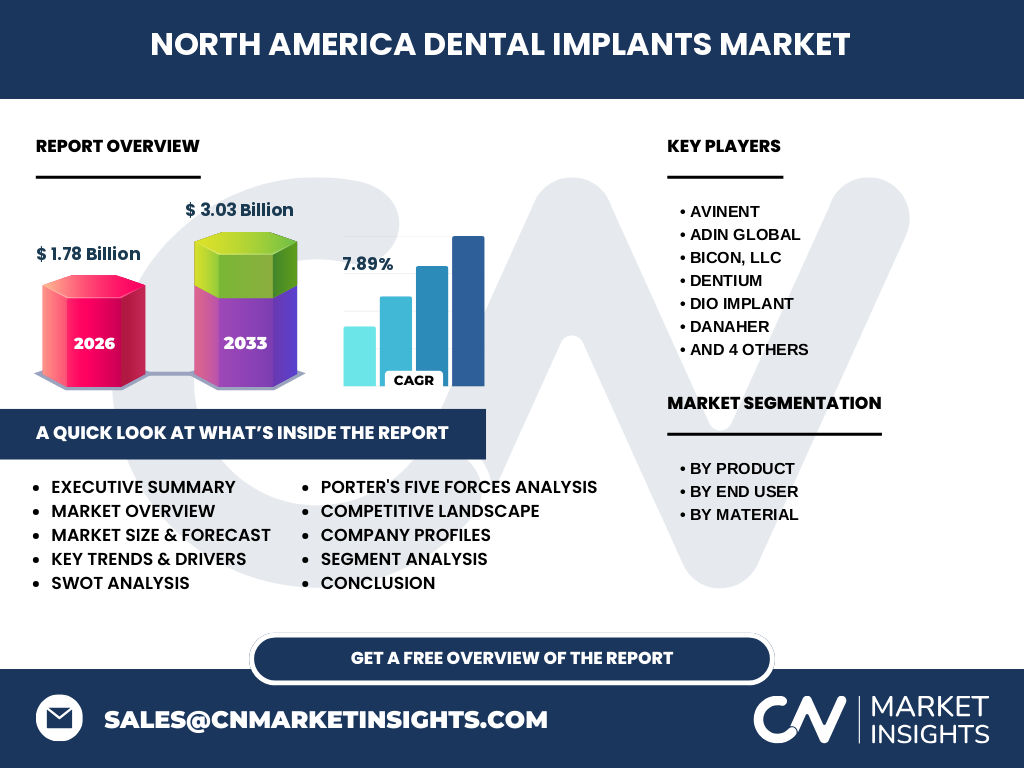

Who are the major competitors and what is the level of consolidation in the North America Dental Implants Market?

The competitive landscape features a mix of multinational corporations and specialized firms. Leading players include AVINENT, Adin Global, Bicon, LLC, DENTIUM, DIO IMPLANT, Danaher, Dentsply Sirona, Institut Straumann AG, OSSTEM IMPLANT, and Zimmer Biomet. These companies compete on product innovation, material science, and distribution networks. Recent years have seen moderate consolidation through strategic acquisitions and joint ventures aimed at expanding product portfolios and geographic reach, but the market remains sufficiently diverse to foster healthy competition.

What are the key takeaways in the Executive Summary of the North America Dental Implants Market?

The market is valued at USD 1.78 billion in 2026 and is projected to reach USD 3.03 billion by 2033, reflecting a compound annual growth rate of 7.89%. Growth is propelled by demographic trends, material innovation, and digital dentistry adoption. While cost and insurance coverage pose constraints, the rise of zirconium implants and integrated service models present substantial upside. The competitive arena is dynamic, with leading manufacturers investing heavily in R&D and strategic partnerships to capture market share.

What forecasts are available for the North America Dental Implants Market from 2025 to 2032?

Based on the provided CAGR of 7.89%, the market is expected to expand steadily, moving from its 2026 baseline of USD 1.78 billion to approximately USD 3.03 billion by 2033. This trajectory suggests incremental annual growth, with each year adding roughly 7–8% to the market size, driven by continued product diversification, increasing end‑user adoption, and ongoing technological advancements.

How is the North America Dental Implants Market sized and shared by product, end‑user, and material segments?

Segmentation is organized into three primary dimensions. By product, the market includes dental bridges, crowns, dentures, and abutments. By end‑user, hospitals & clinics and dental laboratories are the main consumers of implant solutions. By material, titanium implants and zirconium implants represent the core categories, with zirconium gaining traction for its aesthetic benefits. While exact revenue shares are not disclosed, the breadth of segmentation highlights multiple growth levers across product innovation, service delivery, and material science.

What is the geographic distribution of the North America Dental Implants Market on a global scale?

Within the global context, North America represents a leading region due to its advanced healthcare infrastructure, high per‑capita income, and early adoption of digital dental technologies. The market’s 2026 valuation of USD 1.78 billion underscores its prominence relative to other regions, while the forecasted rise to USD 3.03 billion by 2033 reflects continued regional dominance driven by sustained investment in dental research and clinical practice.

What insights does the regional analysis provide for the North America Dental Implants Market?

The United States accounts for the largest share of market activity, benefiting from a dense network of specialist clinics and robust insurance frameworks that support high‑value procedures. Canada contributes through a strong public‑health system that increasingly incorporates implantology into covered services. Mexico, while smaller, shows growth potential driven by expanding middle‑class demand and cross‑border dental tourism. Regional trends point toward greater adoption of digital workflows and a rising preference for zirconium implants across all three countries.

Which companies lead the North America Dental Implants Market and what strategies are they employing?

Key players such as Dentsply Sirona, Zimmer Biomet, and Institut Straumann AG leverage extensive R&D pipelines to launch next‑generation titanium and zirconium products. Companies like AVINENT and OSSTEM IMPLANT focus on cost‑effective solutions for emerging clinics, while Danaher and Bicon, LLC emphasize integrated service offerings and clinician training programs. Strategic moves include acquisitions of niche manufacturers, collaborations with dental laboratories for customized prosthetics, and investments in digital imaging platforms to enhance surgical precision.

How does Porter’s Five Forces framework evaluate the competitive environment of the North America Dental Implants Market?

Threat of new entrants is moderate due to high regulatory barriers and the need for substantial R&D investment. Bargaining power of suppliers is limited, as raw material sources (titanium, zirconium) are relatively commoditized. Buyers—primarily hospitals, clinics, and laboratories—exert significant influence, demanding cost‑effective yet high‑quality solutions. The threat of substitutes is low because alternatives such as removable dentures lack the functional and aesthetic benefits of permanent implants. Competitive rivalry is intense, driven by product differentiation, material innovation, and service integration.

What are the strengths, weaknesses, opportunities, and threats identified in the SWOT analysis for the North America Dental Implants Market?

Strengths: Advanced technological base, strong demand from aging populations, and high clinical success rates. Weaknesses: Elevated procedural costs and uneven insurance reimbursement. Opportunities: Expansion of zirconium implant lines, growth of digital and guided‑surgery platforms, and emerging market segments such as dental tourism. Threats: Potential regulatory changes, economic fluctuations affecting discretionary healthcare spending, and competition from low‑cost overseas manufacturers.

What does the value chain of the North America Dental Implants Market look like?

The value chain begins with raw‑material sourcing (titanium, zirconium), followed by component manufacturing (implants, abutments). Next comes product development, which incorporates R&D, design, and regulatory approval. Distribution channels involve wholesale distributors and direct sales to hospitals, clinics, and laboratories. The final stage encompasses clinical implantation, post‑operative care, and follow‑up services, often supported by manufacturer‑provided training and maintenance programs.

What key investment insights can be drawn for stakeholders interested in the North America Dental Implants Market?

Investors should focus on companies that are expanding zirconium product lines and integrating digital dentistry solutions, as these segments are poised for the highest growth. Partnerships with dental laboratories and service‑oriented business models can accelerate market penetration. Given the projected 7.89% CAGR, long‑term capital allocation toward R&D, strategic acquisitions, and geographic expansion—particularly in Canada and Mexico—offers a compelling risk‑adjusted return profile.

What conclusions can be drawn about the future of the North America Dental Implants Market?

The market is on a clear upward trajectory, with a 2026 value of USD 1.78 billion expected to more than double by 2033. Core growth drivers—demographic shifts, material innovation, and digital workflow adoption—are robust and likely to sustain momentum. While cost and reimbursement remain challenges, the sector’s resilience, supported by technological advances and strategic corporate initiatives, positions it as a lucrative segment of the broader dental industry.

What research methodology was employed to develop this market report?

The analysis combines primary interviews with industry experts, secondary data collection from reputable sources such as industry publications, company annual reports, and regulatory filings, and quantitative modeling to apply the stated CAGR of 7.89% for forecasting. Segmentation frameworks were applied to product, end‑user, and material categories, and competitive mapping was performed using publicly disclosed information on key players.

What is the scope of this research and its coverage limitations?

The study covers the North American region (U.S., Canada, Mexico) and focuses on dental implant products, end‑users, and material types as defined in the segmentation. It does not extend to ancillary dental technologies outside the implant scope, nor does it provide granular market shares beyond the aggregate figures supplied. The forecast period runs from 2025 to 2032, based on the provided CAGR.

Which key companies have made recent developments in the North America Dental Implants Market?

Recent activities include Dentsply Sirona’s launch of a next‑generation zirconium implant system, Zimmer Biomet’s acquisition of a digital imaging startup to enhance guided‑surgery capabilities, and Institut Straumann AG’s partnership with leading dental laboratories for rapid‑prototyping of customized abutments. AVINENT announced a cost‑reduction program targeting mid‑size clinics, while OSSTEM IMPLANT introduced a bundled financing option for hospitals to ease cash‑flow constraints. These developments illustrate the market’s focus on technology integration and value‑added services.