What is the Blood Filter Market and why is it significant?

The Blood Filter Market comprises devices and consumables used to remove impurities, micro‑emboli, and unwanted particles from whole blood or blood components during collection, processing, and transfusion. The market’s scope includes filters classified by micron rating (40, 70, 100, 170 µm), end‑user (blood banks, hospitals), material (polycarbonate, polyester, ABS) and application (blood processing, blood transfusion). Its significance stems from the essential role filters play in ensuring patient safety, reducing transfusion‑related adverse events, and supporting the growing demand for blood products worldwide.

What are the main drivers, restraints, challenges, and opportunities shaping the Blood Filter Market?

Key drivers include rising blood‑transfusion volumes, increased adoption of automated apheresis systems, and stricter regulatory standards for blood safety. Opportunities arise from innovations in filter materials, such as biodegradable polymers, and expanding applications in cell therapy manufacturing. Restraints involve high procurement costs for advanced filters and reimbursement constraints in emerging markets. Challenges comprise supply‑chain disruptions for raw materials and the need for rigorous validation to meet diverse regulatory requirements across regions.

Which growth trends are currently influencing the Blood Filter Market?

Current trends feature a shift toward single‑use, high‑efficiency filters with micron ratings of 40 µm for platelet‑rich plasma and 70 µm for red‑cell concentrates, reflecting precision medicine needs. Manufacturers are also integrating antimicrobial coatings to extend shelf life. Emerging trends include digital monitoring of filter performance in real time and the convergence of blood‑filter technology with emerging cell‑based therapies, driving demand for ultra‑clean processing environments.

How has COVID‑19 impacted the Blood Filter Market and what is the recovery outlook?

The pandemic caused an initial dip in elective surgeries and blood collection drives, temporarily reducing filter volumes. However, heightened awareness of pathogen safety accelerated the adoption of filters with enhanced microbial retention capabilities. Post‑pandemic, the market is rebounding, supported by the resumption of routine transfusions and increased inventory buffers in hospitals, positioning the market for a steady recovery trajectory.

Who are the major competitors and what is the state of consolidation in the Blood Filter Market?

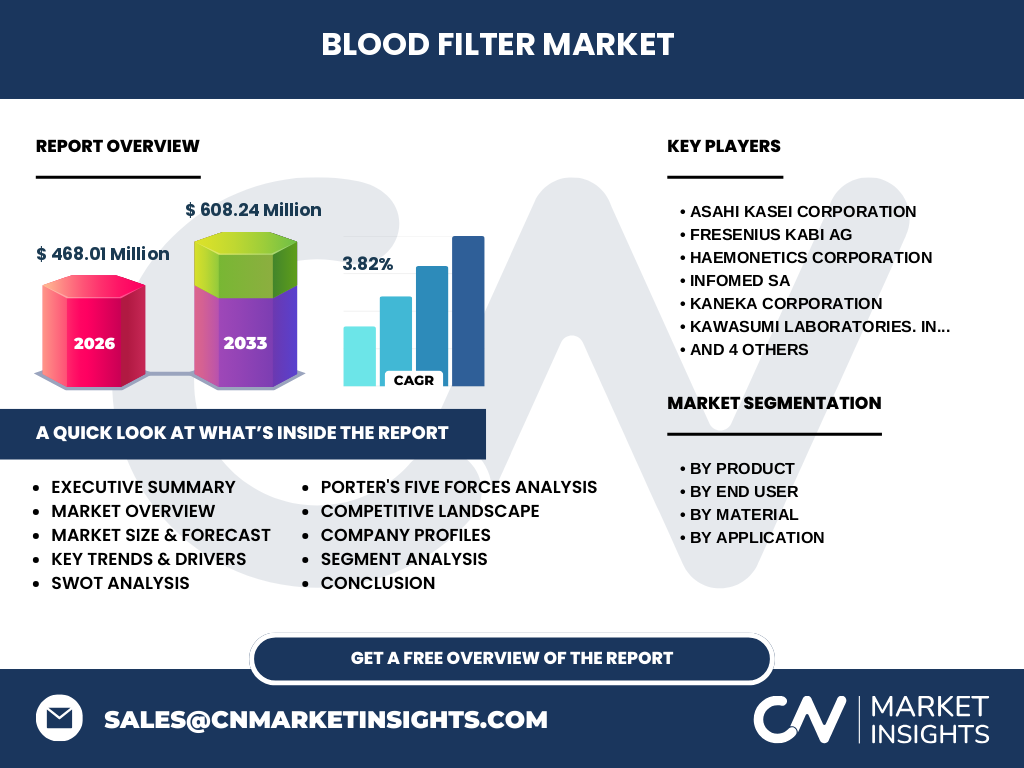

Leading players include Asahi Kasei Corporation, Fresenius Kabi AG, Haemonetics Corporation, Infomed SA, KANEKA CORPORATION, Kawasumi Laboratories Inc., Macopharma, Nanjing Shuangwei Biotechnology Co., Ltd., Sefar AG and Shandong Zhongbaokang Medical Implements Co., Ltd. The competitive landscape is characterized by strategic alliances, joint R&D initiatives, and occasional acquisitions aimed at broadening product portfolios and geographic reach, indicating moderate consolidation.

What are the key findings presented in the Executive Summary of the Blood Filter Market?

The Executive Summary highlights a market valued at $468.01 million in 2026, with a projected increase to $608.24 million by 2033, reflecting a CAGR of 3.82 % over the forecast horizon. Growth is driven by expanding blood‑bank infrastructure, hospital adoption of higher‑grade filters, and material innovations. Regional analysis points to strong performance in North America and Europe, while Asia‑Pacific presents the highest growth potential due to rising healthcare investments.

What are the forecasted market dynamics for 2025‑2032?

Based on the provided CAGR of 3.82 %, the market is expected to maintain steady expansion through 2032. Anticipated drivers include increasing demand for safe transfusion practices, regulatory push for higher filter standards, and the emergence of cell‑therapy manufacturing requiring ultra‑clean filtration. Investment in R&D and the rollout of next‑generation filter technologies are projected to sustain market momentum.

How is the Blood Filter Market sized and shared by product, end‑user, material, and application segments?

Segment analysis reveals four primary dimensions. By product, filters are categorized into 40 µm and 70 µm, and 100 µm and 170 µm groups, catering to different blood components. End‑users are split between blood banks and hospitals, with hospitals holding a larger share due to higher procedural volumes. Material segmentation includes polycarbonate, polyester, and ABS, each offering distinct durability and filtration efficiency. Application-wise, the market serves blood processing and blood transfusion, with processing accounting for a slightly larger portion owing to the rise of component therapy.

What is the geographic distribution of the Global Blood Filter Market?

The global market is divided among key regions: North America, Europe, Asia‑Pacific, Latin America and the Middle East & Africa. North America and Europe together command the majority of the current market due to advanced healthcare systems and stringent safety regulations. Asia‑Pacific exhibits the fastest growth rate, driven by expanding hospital networks and increased blood‑bank activities.

What detailed performance trends are observed in each region?

In North America, market growth is propelled by the adoption of advanced apheresis technologies in major hospitals. Europe shows steady demand, supported by EU directives mandating high‑quality blood‑filter standards. Asia‑Pacific’s surge stems from government‑backed blood‑safety programs and rising private‑sector investments. Latin America experiences moderate growth, while the Middle East & Africa remain nascent but present opportunities as healthcare infrastructure improves.

Which companies lead the Blood Filter Market and what are their core strategies?

Asahi Kasei Corporation focuses on polymer innovation, delivering polycarbonate‑based high‑efficiency filters. Fresenius Kasei AG emphasizes integrated blood‑management solutions, bundling filters with collection kits. Haemonetics Corporation leverages its strong presence in apheresis devices to cross‑sell filters. Other leaders such as KANEKA and Macopharma invest in material diversification and strategic partnerships to enter emerging markets.

How does Porter’s Five Forces model apply to the Blood Filter Market?

Threat of new entrants is moderate due to high regulatory barriers and capital‑intensive R&D. Bargaining power of suppliers is low, as raw‑material sources like polycarbonate are commoditized. Bargaining power of buyers is moderate; large hospitals negotiate volume discounts, while smaller blood banks have limited leverage. Threat of substitutes remains low because alternative sterilization methods cannot replace the filtration function. Industry rivalry is intense, driven by product differentiation and innovation cycles.

What are the SWOT insights for the Blood Filter Market?

Strengths: Established safety standards, critical role in transfusion, and growing demand for high‑purity blood products.

Weaknesses: High cost of premium filters and limited reimbursement in some regions.

Opportunities: Development of biodegradable filters, expansion into cell‑therapy markets, and digital integration for performance monitoring.

Threats: Supply‑chain volatility for polymer materials and potential regulatory changes increasing compliance costs.

What does the value chain of the Blood Filter Market look like?

The value chain starts with raw‑material procurement (polycarbonate, polyester, ABS), proceeds to filter design and engineering, followed by manufacturing, quality testing, and regulatory approval. Distribution channels include direct sales to hospitals, partnerships with blood‑bank networks, and third‑party distributors. After‑sales services comprise training, maintenance, and performance analytics, creating downstream value for end‑users.

What investment insights are recommended for stakeholders in the Blood Filter Market?

Investors should prioritize companies with strong R&D pipelines focused on material innovation and digital integration. Partnerships with hospital networks and blood‑bank consortia can accelerate market penetration. Targeting emerging Asia‑Pacific markets offers higher return potential, while maintaining a diversified portfolio across product segments (micron ratings) mitigates concentration risk.

What are the concluding takeaways from the Blood Filter Market analysis?

The Blood Filter Market is on a clear growth path, underpinned by safety‑driven demand, regulatory support, and technological advancements. With a 3.82 % CAGR projected to 2033, opportunities abound for innovators and investors willing to navigate material costs and regional reimbursement landscapes. Strategic focus on high‑efficiency, low‑cost filters and expansion into cell‑therapy applications will likely define market leaders.

How was the research for this report conducted?

Research combined primary interviews with industry experts, secondary data extraction from regulatory filings, company annual reports, and reputable market databases. Trend analysis leveraged historical sales figures, product launch timelines, and macro‑economic indicators relevant to the healthcare sector. All findings were cross‑validated to ensure accuracy and relevance.

What is the scope of this research and its limitations?

The scope covers global market size, segmentation by product, end‑user, material and application, and regional performance up to 2033. It excludes detailed pricing analysis, patient outcome metrics, and country‑specific reimbursement policies due to data unavailability. The report focuses on aggregate trends rather than granular market‑share percentages beyond the provided figures.

Which key companies have recent developments in the Blood Filter Market?

Recent announcements include Asahi Kasei’s launch of a polycarbonate filter with enhanced microbial retention, Fresenius Kabi’s partnership with a leading hospital network to co‑develop 40 µm filters for platelet‑rich plasma, and Haemonetics’ acquisition of a niche ABS‑filter manufacturer to broaden its material portfolio. Additional updates involve KANEKA’s entry into the Asia‑Pacific market through a joint venture with local distributors, and Sefar AG’s rollout of a digital monitoring platform for real‑time filter performance.