What is the Asia Pacific 3D Sensors Market Overview – definition, scope, and significance?

The Asia Pacific 3D sensors market comprises devices that capture depth information by employing technologies such as stereo vision, time‑of‑flight, structured light, and flood illumination. These sensors enable precise three‑dimensional mapping for applications ranging from automotive driver‑assistance to medical imaging and industrial automation. The market’s significance lies in its ability to enhance product safety, improve operational efficiency, and drive innovation across multiple high‑growth verticals throughout the rapidly digitising Asia Pacific region.

What are the primary drivers, restraints, challenges, and opportunities shaping the Asia Pacific 3D Sensors Market?

Key drivers include rising demand for advanced driver‑assistance systems, expanding smart‑factory initiatives, and growing adoption of 3D imaging in healthcare diagnostics. Restraints stem from high component costs and stringent regulatory requirements, especially in medical and aerospace sectors. Challenges involve integration complexity with legacy systems and the need for robust performance under diverse environmental conditions. Opportunities arise from emerging applications such as augmented reality, robotics, and the rollout of 5G‑enabled edge computing, which demand high‑resolution, low‑latency depth sensing.

What growth trends are currently influencing the Asia Pacific 3D Sensors Market?

Current trends feature a shift toward miniaturised, low‑power sensor modules suitable for consumer electronics, and the convergence of AI algorithms with time‑of‑flight technology to improve accuracy. There is also a noticeable increase in collaborative development between sensor manufacturers and automotive OEMs to embed 3D vision directly into vehicle platforms. Additionally, the rise of smart‑city projects is prompting wider deployment of structured‑light sensors for infrastructure monitoring and public‑safety applications.

How did COVID‑19 impact the Asia Pacific 3D Sensors Market and what is the recovery trajectory?

The pandemic initially slowed supply chains and postponed large‑scale capital projects, causing a temporary dip in demand for industrial‑grade sensors. However, the accelerated shift to remote diagnostics, tele‑medicine, and contact‑free interfaces boosted demand for healthcare‑focused 3D imaging solutions. Recovery has been robust, with manufacturers re‑establishing production capacities and leveraging heightened interest in automation to regain momentum, positioning the market for strong post‑pandemic growth.

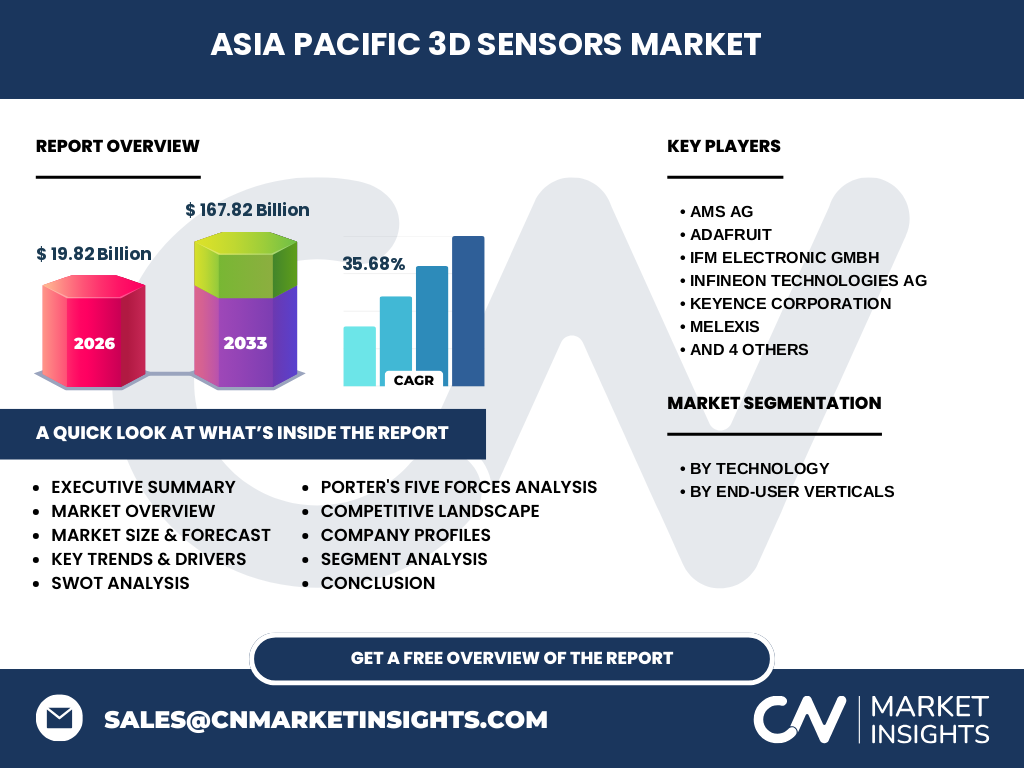

Who are the major competitors in the Asia Pacific 3D Sensors Market and what is the level of market consolidation?

Leading competitors include AMS AG, Adafruit, IFM Electronic GmbH, Infineon Technologies AG, Keyence Corporation, Melexis, STMicroelectronics, Sony Corporation, Teledyne, and Texas Instruments Incorporated. The market exhibits moderate consolidation, marked by strategic alliances and joint development agreements rather than large‑scale mergers. Companies are focusing on expanding technology portfolios and geographic reach to capture emerging opportunities across the region.

What are the key findings highlighted in the executive summary of the Asia Pacific 3D Sensors Market?

The executive summary underscores a rapidly expanding market valued at US$19.82 billion in 2026, with an aggressive forecast to reach US$167.82 billion by 2033, driven by a compound annual growth rate of 35.68 %. Growth is propelled by strong demand in automotive, industrial, and healthcare sectors, complemented by technological innovations such as AI‑enhanced TOF sensors. The region’s diverse economies and early adoption of advanced manufacturing further amplify market potential.

What are the forecast expectations for the Asia Pacific 3D Sensors Market from 2025 to 2032?

Projections indicate continued double‑digit expansion, maintaining the 35.68 % CAGR through 2032. The forecast reflects sustained investment in autonomous vehicle platforms, increased deployment of 3D sensors in smart factories, and broader acceptance of depth‑sensing solutions in consumer electronics. Market participants anticipate escalating volume shipments, especially for time‑of‑flight and structured‑light devices, as product cycles shorten and demand for high‑precision imaging intensifies.

How is the Asia Pacific 3D Sensors Market sized and shared across technology and end‑user segments?

Segmentation by technology comprises stereo vision, time‑of‑flight, structured light, and flood illumination, each catering to distinct application needs. End‑user verticals include healthcare, aerospace, industrial, and automotive sectors. While precise quantitative shares are proprietary, the market narrative points to time‑of‑flight and structured‑light technologies commanding the largest share due to their versatility, with healthcare and automotive representing the most lucrative end‑user categories.

What is the geographic distribution of the Asia Pacific 3D Sensors Market size and share by region?

The market is broadly distributed across key Asia Pacific economies, with Japan, China, South Korea, and India emerging as major contributors. These nations host significant manufacturing bases, strong R&D ecosystems, and early adoption of 3D sensing in automotive and consumer electronics. The regional landscape reflects a balanced mix of mature markets (e.g., Japan) and high‑growth emerging economies (e.g., India), collectively shaping overall market size.

What does the regional analysis reveal about performance within the Asia Pacific 3D Sensors Market?

Japan leads in advanced sensor integration for automotive and industrial robotics, leveraging its legacy in precision engineering. China drives volume manufacturing, offering cost‑competitive solutions that fuel adoption across consumer devices and smart‑city projects. South Korea contributes innovative semiconductor‑based sensor designs, while India shows rapid growth in healthcare imaging and low‑cost industrial automation. Each sub‑region displays unique strengths, creating a synergistic growth environment.

Which companies are leading in the Asia Pacific 3D Sensors Market and what are their strategic approaches?

Key players such as Sony Corporation and Texas Instruments focus on high‑performance TOF and structured‑light modules, emphasizing integration with AI and edge computing. AMS AG and Infineon target automotive safety systems through robust, automotive‑grade sensor suites. Keyence and STMicroelectronics prioritize industrial automation, offering ruggedized solutions for factory floor deployment. Strategic moves include joint ventures, expanded R&D centers in the region, and portfolio diversification to address emerging verticals.

How does Porter’s Five Forces framework assess competition in the Asia Pacific 3D Sensors Market?

• Threat of new entrants: Moderate, due to high capital requirements and technological barriers. • Bargaining power of suppliers: Low to moderate, as multiple semiconductor and optics suppliers exist. • Bargaining power of buyers: Increasing, driven by OEM demand for cost‑effective, high‑spec solutions. • Threat of substitutes: Low, because few alternative technologies match the depth‑accuracy of 3D sensors. • Industry rivalry: High, with intense competition among established players to innovate and secure key automotive and healthcare contracts.

What are the strengths, weaknesses, opportunities, and threats identified in the SWOT analysis of the Asia Pacific 3D Sensors Market?

Strengths: Strong R&D ecosystem, diverse application base, and rapid adoption in high‑growth sectors. Weaknesses: High component costs and sensitivity to supply‑chain disruptions. Opportunities: Expansion into AR/VR, robotics, and 5G‑enabled edge devices; rising demand for contact‑less healthcare solutions. Threats: Regulatory hurdles in aerospace and medical domains, and potential market saturation in lower‑margin consumer segments.

How is the value chain structured for the Asia Pacific 3D Sensors Market?

The value chain begins with raw material suppliers (silicon wafers, optics), progresses to component manufacturers that fabricate sensor chips, followed by system integrators that embed sensors into modules. Next are OEMs and system designers who incorporate modules into final products across automotive, industrial, and healthcare lines. Distribution channels include specialized distributors and direct sales to large manufacturers, while after‑sales services and software updates complete the chain.

What key investment insights does the Asia Pacific 3D Sensors Market offer to investors?

Investors should target companies with strong AI‑sensor integration capabilities and those expanding into high‑margin verticals such as autonomous vehicles and medical imaging. Partnerships with automotive OEMs and participation in government‑backed smart‑city initiatives provide strategic leverage. Additionally, funding R&D efforts around low‑power, miniaturised sensors can capture emerging consumer‑electronics demand, offering diversified growth pathways.

What conclusions can be drawn from the Asia Pacific 3D Sensors Market analysis?

The market is poised for explosive growth, underpinned by a 35.68 % CAGR and a projected rise from US$19.82 billion in 2026 to US$167.82 billion by 2033. Technological innovation, strong regional manufacturing capabilities, and expanding end‑user applications collectively drive this trajectory. Companies that align product development with AI, edge computing, and sector‑specific regulations are likely to secure the most advantageous market positions.

What research methodology was employed to produce this market report?

The study combined primary interviews with industry experts, secondary data collection from reputable databases, and quantitative modeling using the provided market size, forecast, and CAGR figures. Trend analysis, competitive benchmarking, and scenario planning were applied to validate forecasts and assess strategic implications.

What is the scope of the research, including coverage and limitations?

The research covers the Asia Pacific region, focusing on technology (stereo vision, TOF, structured light, flood illumination) and end‑user verticals (healthcare, aerospace, industrial, automotive). It evaluates major players listed in the source data. Limitations include reliance on publicly available information and the exclusion of unreleased proprietary financial metrics beyond the provided figures.

Which key companies and recent developments are notable in the Asia Pacific 3D Sensors Market?

Notable players such as Sony Corporation announced a new high‑resolution TOF sensor optimized for autonomous driving, while Texas Instruments introduced a low‑power structured‑light module aimed at AR devices. AMS AG launched a healthcare‑focused 3D imaging platform, and Infineon secured a partnership with a leading Chinese automaker to supply automotive‑grade sensors. These developments illustrate ongoing product innovation and strategic collaborations across the region.