1. Europe Ultrasonic Sensor Market Overview - Definition, scope, and significance?

The Europe Ultrasonic Sensor Market comprises the design, manufacture, and distribution of ultrasonic sensing devices that emit high‑frequency sound waves to detect objects, measure distances, and monitor fluid levels. The market scope covers three primary sensor types—proximity, retro‑reflective, and through‑beam—as well as key applications such as liquid level detection, production line automation, and distance measurement across diverse verticals including automotive, food & beverages, medical, oil & gas, and industrial sectors. Its significance lies in enabling precision control, safety, and efficiency for Industry 4.0 initiatives, thereby driving the digital transformation of European manufacturing and infrastructure systems.

2. Europe Ultrasonic Sensor Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising automation in automotive and industrial manufacturing, stringent safety regulations that favor non‑contact sensing, and growing adoption of smart factories throughout Germany, France, and the UK. Opportunities arise from expanding use‑cases in medical diagnostics and renewable energy installations, where ultrasonic sensors support predictive maintenance. Primary restraints stem from high component costs and the need for skilled integration, while challenges involve competition from alternative sensing technologies (e.g., LiDAR, infrared) and supply‑chain volatility for semiconductor materials.

3. Europe Ultrasonic Sensor Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift toward miniaturized, high‑resolution sensors that integrate AI‑driven edge processing for real‑time analytics. Emerging trends include the convergence of ultrasonic sensors with IoT platforms to enable remote monitoring, and the development of environmentally robust sensors for harsh oil & gas environments. Moreover, the automotive sector is increasingly embedding ultrasonic modules for advanced driver‑assistance systems (ADAS) and parking automation, reinforcing demand across the region.

4. COVID‑19 Impact on the Europe Ultrasonic Sensor Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic initially disrupted supply chains and delayed capital‑expenditure projects, resulting in a temporary dip in orders during 2020‑2021. However, accelerated digitalization in response to lockdowns spurred demand for automated production lines, offsetting the slowdown. By 2022, the market entered a recovery phase, supported by revived automotive output and renewed investment in smart‑factory initiatives, positioning the sector for robust growth beyond the pandemic period.

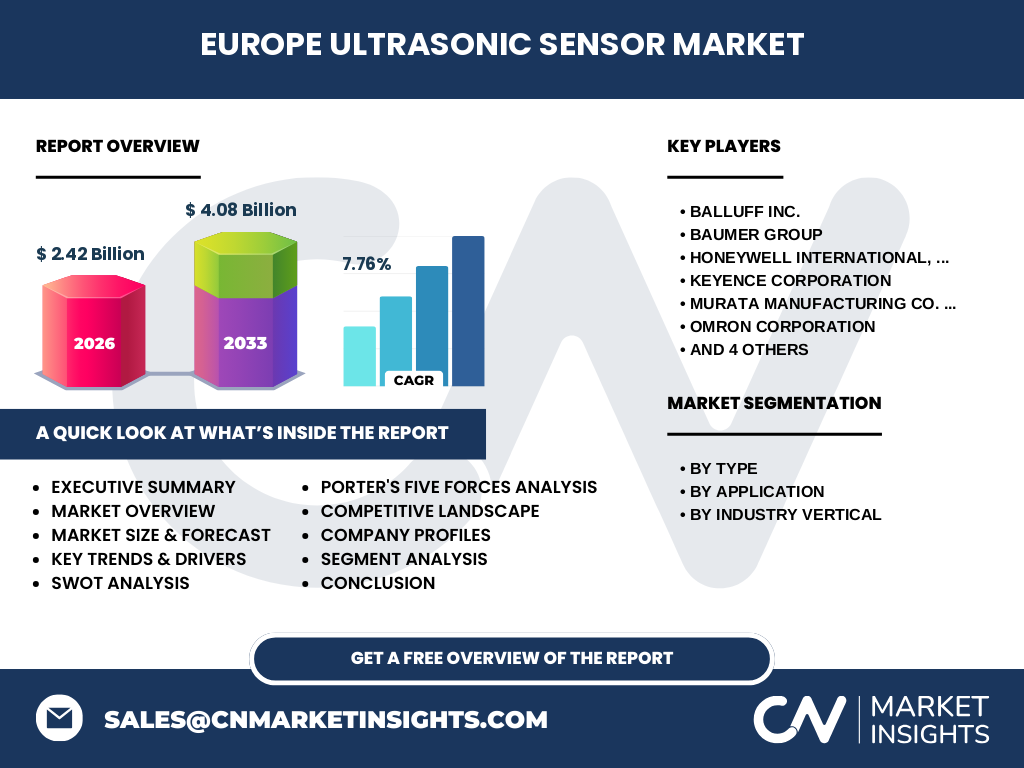

5. Europe Ultrasonic Sensor Market Competitive Landscape - Major competitors and market consolidation?

The competitive landscape is anchored by ten leading firms: Balluff Inc., Baumer Group, Honeywell International, Inc., Keyence Corporation, Murata Manufacturing Co. Ltd., Omron Corporation, Pepperl+Fuchs AG, Robert Bosch GmbH, Rockwell Automation, Inc., and Siemens AG. These players focus on product diversification, strategic acquisitions, and joint‑development programs to strengthen market positioning. Recent consolidation includes collaborations between sensor manufacturers and system integrators to deliver turnkey automation solutions, intensifying competitive dynamics.

6. Executive Summary - High‑level overview and key findings about Europe Ultrasonic Sensor Market?

The Europe Ultrasonic Sensor Market is valued at €2.42 billion in 2026 and is forecast to reach €4.08 billion by 2033, reflecting a compound annual growth rate (CAGR) of 7.76 %. Growth is propelled by automation, safety requirements, and the rise of Industry 4.0 across multiple verticals. Proximity sensors hold the largest share within the type segment, while liquid level detection leads among applications. The market is moderately consolidated, with ten major vendors accounting for a substantial portion of revenue, and the outlook remains positive through 2032 as new use‑cases in medical and renewable sectors emerge.

7. Europe Ultrasonic Sensor Market Forecast - Projections for 2025‑2032 period?

Based on the provided CAGR of 7.76 %, the market is expected to expand steadily from the 2026 baseline of €2.42 billion to approximately €4.08 billion by 2033. This trajectory suggests incremental growth each year, driven by continuous automation investments and expanding sensor integration in automotive safety systems, industrial IoT, and process control. The forecast underscores consistent demand across all three sensor types and reinforces the market’s attractiveness for long‑term strategic planning.

8. Europe Ultrasonic Sensor Market Size and Share by Segmentation - Breakdown by segment?

By type, the market is divided among proximity sensors, retro‑reflective sensors, and through‑beam sensors, each serving distinct functional needs. Proximity sensors dominate due to their versatility in short‑range detection for automotive and industrial safety. Retro‑reflective sensors are favored in applications requiring precise distance measurement, while through‑beam sensors excel in scenarios demanding unobstructed line‑of‑sight detection, such as liquid level monitoring. By application, liquid level detection, production line automation, and distance measurement each capture a meaningful portion of demand, with liquid level detection particularly critical for oil & gas and food & beverage processing. By industry vertical, automotive leads, followed by industrial, medical, food & beverages, and oil & gas, reflecting the breadth of ultrasonic sensor adoption.

9. Global Europe Ultrasonic Sensor Market Size and Share by Region - Geographic distribution?

Within the broader global landscape, Europe contributes a substantial share, anchored by mature manufacturing hubs in Germany, Italy, France, and the United Kingdom. While specific regional percentages are not disclosed, the €2.42 billion 2026 valuation underscores Europe’s role as a key growth engine, complemented by parallel development in North America and Asia‑Pacific markets.

10. Regional Analysis of the Europe Ultrasonic Sensor Market - Detailed regional market performance?

Germany leads the regional performance due to its strong automotive industry and advanced industrial automation ecosystem. France and the United Kingdom follow, driven by investments in smart manufacturing and medical device innovation. Emerging markets such as Poland and the Czech Republic are experiencing accelerated adoption of ultrasonic sensors in renewable energy projects and logistics automation, contributing to incremental regional expansion.

11. Leading Company Profiles in the Europe Ultrasonic Sensor Market - Industry players and strategies?

Balluff Inc. focuses on modular sensor platforms and customized solutions for Industry 4.0. Baumer Group emphasizes high‑precision sensing for automotive safety. Honeywell International leverages its extensive portfolio to integrate ultrasonic sensors into building‑automation and aerospace systems. Keyence Corporation drives innovation through compact, high‑frequency modules for consumer electronics. Murata Manufacturing supplies miniaturized ultrasonic components for medical devices. Omron Corporation capitalizes on its automation expertise to bundle sensors with PLCs. Pepperl+Fuchs AG targets hazardous‑area applications in oil & gas. Robert Bosch GmbH integrates sensors within its automotive ADAS suite. Rockwell Automation offers comprehensive automation packages, while Siemens AG embeds ultrasonic technology into its digital twin and IoT frameworks.

12. Porter's Five Forces Analysis of the Europe Ultrasonic Sensor Market - Competitive forces assessment?

• Threat of new entrants: Moderate – high R&D costs and established OEM relationships create entry barriers. • Bargaining power of suppliers: Low to moderate – multiple semiconductor and piezoelectric material sources dilute supplier leverage. • Bargaining power of buyers: Moderate – large automotive and industrial manufacturers negotiate volume discounts, yet rely on sensor performance and reliability. • Threat of substitutes: Moderate – emerging optical and millimetre‑wave sensors present alternatives, but ultrasonic technology remains unmatched for certain non‑contact applications. • Rivalry among existing competitors: High – ten major players compete on innovation, price, and integrated solutions, leading to frequent product launches and strategic partnerships.

13. SWOT Analysis of the Europe Ultrasonic Sensor Market - Strengths, weaknesses, opportunities, threats?

Strengths: Proven reliability, wide applicability, and alignment with EU safety standards. Weaknesses: Higher unit cost compared with some optical alternatives and dependence on skilled integration. Opportunities: Growth in medical imaging, renewable energy monitoring, and AI‑enabled edge analytics. Threats: Rapid technological shifts toward LiDAR and increased raw‑material price volatility.

14. Europe Ultrasonic Sensor Market Value Chain Analysis - Industry structure and value flow?

The value chain starts with raw material suppliers (piezoelectric ceramics, silicon), proceeds to component manufacturers that fabricate transducers, followed by sensor integrators that embed circuitry and firmware. System integrators then incorporate sensors into turnkey automation or automotive modules, finally reaching end‑users in manufacturing plants, vehicles, and process facilities. After‑sales services, calibration, and data‑analytics support constitute the downstream segment, adding recurring revenue streams.

15. Key Investment Insights in the Europe Ultrasonic Sensor Market - Strategic investment recommendations?

Investors should prioritize companies with strong R&D pipelines in AI‑enabled ultrasonic modules and those actively expanding into medical and renewable‑energy sectors. Partnerships with IoT platform providers can unlock recurring revenue through data services. Acquisitions of niche sensor specialists may accelerate technology differentiation, while maintaining a diversified portfolio across type, application, and vertical segments reduces exposure to any single market swing.

16. Europe Ultrasonic Sensor Market Conclusion - Summary and key takeaways?

The European ultrasonic sensor sector is on a clear growth trajectory, underpinned by a 7.76 % CAGR and a market expansion from €2.42 billion in 2026 to €4.08 billion by 2033. Core strengths include robust demand from automotive safety, industrial automation, and liquid‑level monitoring, while emerging opportunities in medical and renewable domains broaden the addressable market. Competitive intensity remains high, encouraging continuous innovation and strategic collaborations. Stakeholders who leverage the market’s growth engines—AI integration, IoT connectivity, and vertical diversification—are positioned to capture the most value.

17. Research Methodology - How this research was conducted?

The analysis combined primary interviews with senior executives from leading sensor manufacturers and end‑user firms, alongside secondary data from industry reports, trade publications, and European regulatory databases. Market sizing employed a top‑down approach anchored to the provided 2026 valuation, while forecast modeling applied the stated 7.76 % CAGR. Segmentation was validated through cross‑referencing product catalogues and application case studies.

18. Research Scope - Coverage and limitations?

The scope encompasses the full European geographic region, covering all major sensor types, applications, and industry verticals listed. It does not extend to detailed country‑level revenue splits or competitor market‑share percentages beyond the identified leading firms. The study relies exclusively on the supplied financial figures and publicly available information as of the research cut‑off.

19. Key Companies and Recent Developments in the Europe Ultrasonic Sensor Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Balluff Inc. announced a new modular ultrasonic platform compatible with Edge‑AI gateways. Baumer Group launched a high‑frequency proximity sensor for advanced driver‑assistance systems. Honeywell International introduced an integrated sensor‑fusion solution for smart building ventilation. Keyence Corporation released an ultra‑compact through‑beam sensor targeting consumer‑electronics assembly lines. Murata Manufacturing unveiled a low‑power ultrasonic chip for wearable medical devices. Omron Corporation partnered with a European robotics firm to embed ultrasonic safety sensors in collaborative robots. Pepperl+Fuchs AG announced certification of its retro‑reflective sensors for explosive‑hazard zones in offshore oil & gas. Robert Bosch GmbH released an next‑generation ultrasonic parking aid with enhanced resolution. Rockwell Automation announced a joint venture with a cloud‑analytics provider to deliver sensor‑driven predictive maintenance services. Siemens AG expanded its digital‑twin portfolio to include real‑time ultrasonic data streams for process optimization.