What is the Asia Pacific Contract Research Organization (CRO) Market Overview – definition, scope, and significance?

The Asia Pacific Contract Research Organization (CRO) market comprises service firms that provide outsourced research and development support to pharmaceutical, biotechnology, and medical‑device companies throughout the region. Services span early‑phase development, clinical trial management, laboratory testing, and post‑approval activities. The market’s significance lies in its ability to accelerate drug pipelines, reduce R&D costs, and enable global sponsors to leverage the region’s diversified patient populations, cost‑effective talent base, and supportive regulatory environments.

What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific CRO market?

Key drivers include rising R&D spend by pharma and biotech firms, demand for faster clinical timelines, and increasing adoption of decentralized trial models. Restraints stem from complex regulatory heterogeneity across APAC nations and talent shortages in specialized therapeutic areas. Challenges involve data integrity concerns and heightened competition from low‑cost offshore providers. Opportunities arise from expanding precision‑medicine trials, growth of biosimilar development, and government incentives encouraging local CRO capabilities.

What growth trends are currently influencing the Asia Pacific CRO market?

Current trends feature a shift toward integrated end‑to‑end service platforms, incorporation of real‑world evidence and artificial‑intelligence analytics, and a surge in partnership models between global CROs and regional niche players. Additionally, the adoption of virtual and hybrid trial designs is accelerating, while demand for laboratory services tied to biomarker discovery and companion diagnostics continues to grow.

How did COVID‑19 impact the Asia Pacific CRO market, and what is the recovery trajectory?

The pandemic initially disrupted trial enrollment and site operations, prompting many sponsors to pause or redesign studies. However, the crisis also accelerated digital transformation, remote monitoring, and home‑based sampling, which have become permanent fixtures. Recovery is robust, with sponsors increasingly outsourcing to CROs that demonstrated agility during COVID‑19, driving a clear upward trajectory toward pre‑pandemic growth rates.

What does the competitive landscape of the Asia Pacific CRO market look like?

The market is fragmented yet consolidating, led by global giants such as IQVIA Inc., Charles River Laboratories, and Icon PLC, alongside strong regional specialists like Novotech and Parexel International Corporation. Recent M&A activity reflects strategic moves to broaden service portfolios and geographic reach, intensifying competition while creating opportunities for niche expertise to command premium pricing.

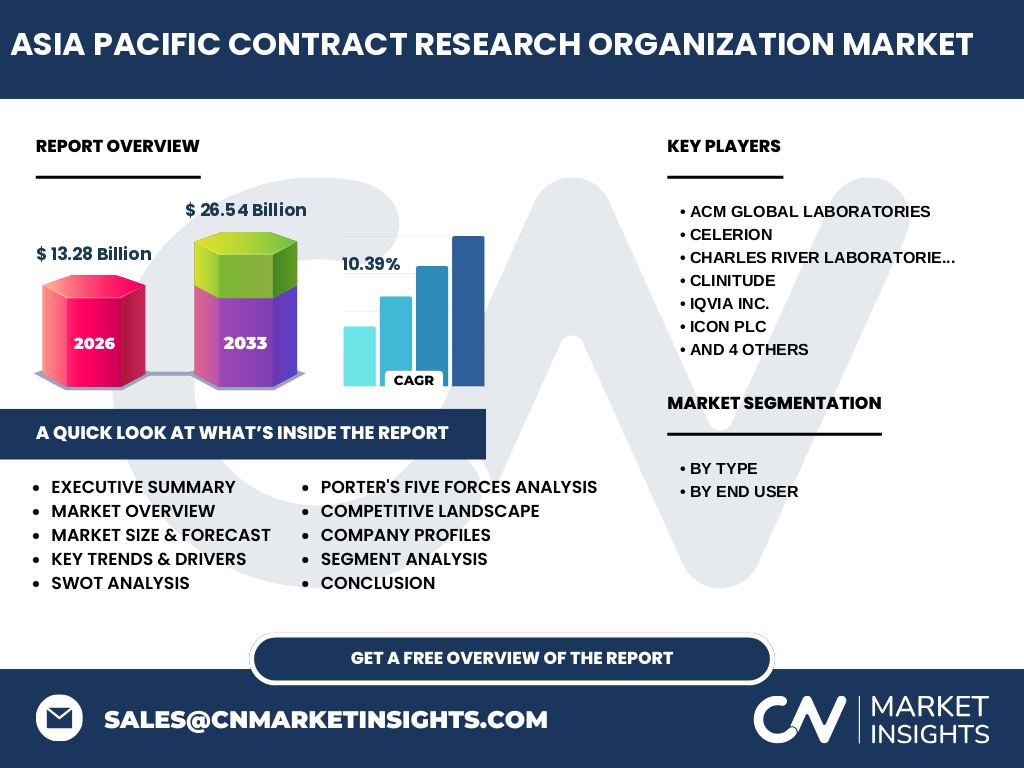

What are the key findings summarized in the executive summary of the Asia Pacific CRO market?

The Asia Pacific CRO market is valued at $13.28 billion in 2026 and is projected to reach $26.54 billion by 2033, delivering a CAGR of 10.39 % over the forecast horizon. Growth is propelled by expanding clinical research services, heightened demand for early‑phase development, and robust laboratory capabilities. Strategic partnerships and digital innovation are critical success factors, while regulatory harmonization remains a priority for sustained expansion.

What are the market forecasts for the Asia Pacific CRO market for 2025‑2032?

Based on the provided CAGR of 10.39 %, the market is expected to maintain double‑digit growth through 2032, effectively doubling its 2026 size. This trajectory underscores strong demand for outsourced research solutions, particularly in clinical and early‑phase services, and suggests a continued influx of investment into advanced trial technologies and capacity expansion across the region.

How is the Asia Pacific CRO market sized and shared by segmentation?

Segmented by service type, the market includes Early Phase Development Services, Clinical Research Services, Laboratory Services, and Post‑approval Services. By end user, it serves Pharmaceutical and Biotechnology Companies as well as Medical Device Companies. Each segment contributes to the overall market value of $13.28 billion in 2026, with Clinical Research Services typically commanding the largest share due to the volume of trial outsourcing, while Laboratory Services show rapid growth owing to biomarker and diagnostic needs.

What is the global Asia Pacific CRO market size and share by region?

The Asia Pacific region accounts for a substantial portion of the global CRO landscape, reflected in its $13.28 billion valuation in 2026. Although specific regional percentages are not disclosed, the forecasted rise to $26.54 billion by 2033 highlights the region’s expanding influence relative to other continents, driven by its cost‑effective infrastructure and growing patient pools.

What does the regional analysis reveal about performance within the Asia Pacific CRO market?

Key sub‑regional hubs include China, Japan, Australia, and India, each offering distinct advantages—China’s large patient base, Japan’s advanced regulatory framework, Australia’s mature clinical trial ecosystem, and India’s cost‑efficient talent pool. Performance varies, with China and India witnessing the fastest growth due to expanding biotech sectors, while Japan and Australia maintain stable, high‑quality service delivery that attracts premium contracts.

Which leading companies are operating in the Asia Pacific CRO market and what are their strategies?

Prominent players include ACM Global Laboratories, Celerion, Charles River Laboratories, Inc., Clinitude, IQVIA Inc., Icon PLC, Laboratory Corporation of America Holdings (Covance Inc.), Merck KGaA (Bio Reliance Corporation), Novotech, and Parexel International Corporation. Strategies focus on expanding geographic footprint, investing in digital trial platforms, broadening therapeutic expertise, and forming strategic alliances to enhance service depth and client reach.

How does Porter’s Five Forces analysis apply to the Asia Pacific CRO market?

• Threat of new entrants is moderate, given high capital requirements and regulatory expertise needed. • Bargaining power of buyers is strong, as sponsors can switch providers to negotiate better terms. • Bargaining power of suppliers (e.g., technology platforms, site networks) is moderate. • Threat of substitutes is low, because the specialized nature of CRO services is difficult to replace. • Industry rivalry is intense, driven by consolidation and the race to offer integrated digital solutions.

What are the SWOT insights for the Asia Pacific CRO market?

Strengths: Cost‑effective talent, diverse patient populations, growing R&D spend. Weaknesses: Regulatory fragmentation, variable data quality across sites. Opportunities: Precision‑medicine trials, AI‑driven data analytics, expansion of biosimilar programs. Threats: Increasing competition from low‑cost offshore providers and potential regulatory tightening.

What does the value‑chain analysis of the Asia Pacific CRO market reveal?

The value chain begins with sponsor demand generation, proceeds to study design and protocol development, followed by site selection, patient recruitment, data capture, clinical monitoring, laboratory analysis, and ends with regulatory submission and post‑approval support. CROs add value at each stage by offering specialized expertise, technology integration, and cost efficiencies, especially in the data management and laboratory testing nodes.

What key investment insights can be drawn for stakeholders in the Asia Pacific CRO market?

Investors should target CROs that demonstrate robust digital infrastructure, diversified service portfolios, and strong footholds in high‑growth sub‑regions like China and India. Partnerships with technology firms and acquisition of niche specialty providers can accelerate market penetration. Emphasis on regulatory compliance capabilities will mitigate risk and enhance long‑term profitability.

What conclusions can be drawn about the Asia Pacific CRO market?

The Asia Pacific CRO market is on a clear growth path, underpinned by a 10.39 % CAGR and a forecasted market size of $26.54 billion by 2033. Its evolution is shaped by digital transformation, expanding therapeutic pipelines, and strategic consolidation. Companies that adapt to hybrid trial models and strengthen regulatory expertise are poised to capture the expanding opportunity set.

How was the research for this market report conducted?

The study employed a mixed‑method approach, combining secondary data extraction from industry reports, regulatory filings, and company disclosures with primary insights gathered through expert interviews with CRO executives, sponsor representatives, and regulatory consultants across the Asia Pacific region. Data triangulation ensured consistency and reliability of the findings.

What is the scope of this research and its limitations?

The research covers the entire Asia Pacific CRO market, segmented by service type and end user, and includes regional performance insights for major sub‑markets. Limitations arise from the absence of publicly disclosed market share percentages for individual countries and from relying on projected growth figures rather than audited financial statements for the forecast period.

Which key companies have recent developments in the Asia Pacific CRO market?

Recent highlights include IQVIA’s launch of an AI‑enabled trial monitoring platform in Japan, Icon PLC’s acquisition of a niche laboratory service provider in Australia, Novotech’s partnership with a leading Chinese biotech firm to accelerate Oncology trials, and Parexel’s expansion of its decentralized trial capabilities across Southeast Asia. These moves underscore a strategic focus on technology integration and regional expansion.