What is the Security Advisory Services Market Overview – definition, scope, and significance?

The Security Advisory Services Market comprises professional consulting and managed services that help organizations assess, design, implement, and continuously improve their cybersecurity posture. It spans a wide range of offerings, including penetration testing, security program management, vulnerability management, incident response, compliance management, CISO advisory, and security risk management. The market serves enterprises of all sizes across multiple verticals such as IT & telecom, healthcare, energy, manufacturing, BFSI, and the public sector. Its significance lies in the growing complexity of cyber threats, stringent regulatory requirements, and the need for organizations to protect critical assets and maintain stakeholder trust.

What are the key drivers, restraints, challenges, and opportunities shaping the Security Advisory Services Market?

Primary drivers include rising cyber‑attack frequency, increasing regulatory pressure, digital transformation initiatives, and heightened awareness of cyber risk at the board level. Restraints stem from budget constraints in SMEs, talent shortages, and the high cost of advanced advisory services. Challenges involve integrating advisory insights into legacy IT environments and maintaining service quality amid rapid threat evolution. Opportunities arise from emerging technologies such as AI‑driven threat analytics, the growth of cloud security advisory, and the expanding need for remote incident‑response capabilities.

What growth trends are currently influencing the Security Advisory Services Market?

Current trends feature a shift toward managed advisory models that combine continuous monitoring with strategic guidance, the convergence of compliance and risk‑management services, and greater adoption of zero‑trust frameworks. Vendors are increasingly packaging penetration testing with automated remediation recommendations. Additionally, the market is seeing a rise in industry‑specific advisory solutions, especially for healthcare and critical infrastructure, to address sector‑specific threat landscapes.

How did COVID‑19 impact the Security Advisory Services Market and what is the recovery trajectory?

The pandemic accelerated digital adoption, expanding the attack surface as workforces moved remotely. This surge in exposure boosted demand for incident‑response and vulnerability‑management services. While many projects were delayed during lockdowns, the overall market experienced a net uplift, leading to a stronger post‑COVID recovery. Organizations now prioritize resilient security architectures, prompting sustained investment in advisory services as part of broader business continuity strategies.

Who are the major competitors in the Security Advisory Services Market and what is the state of market consolidation?

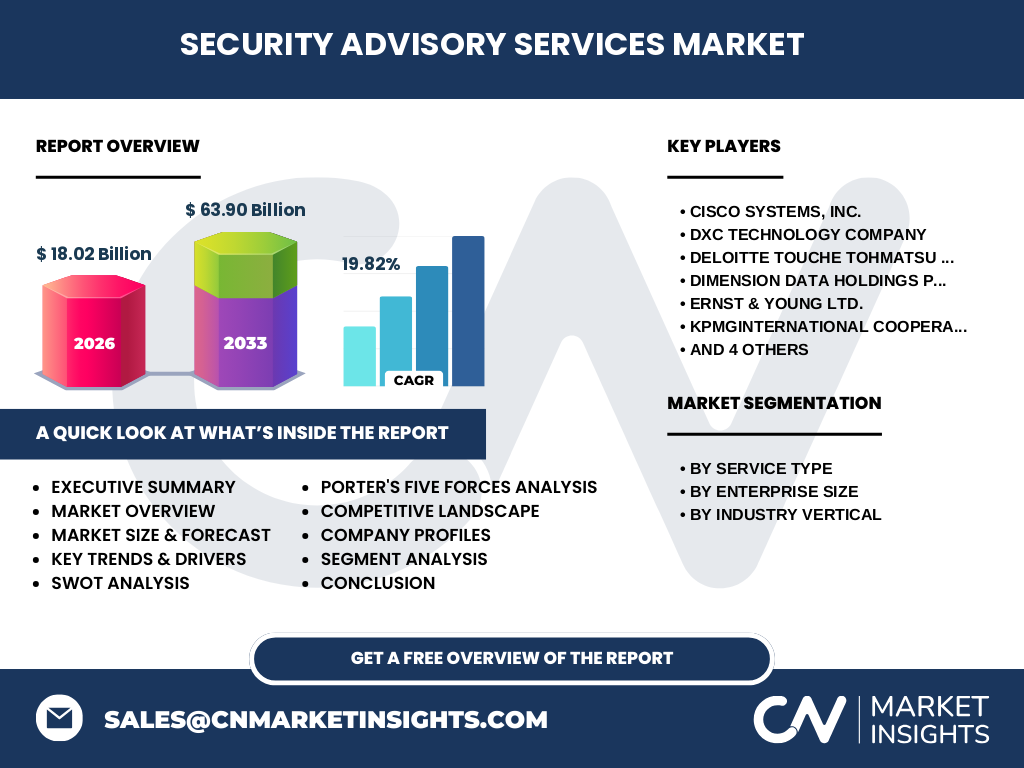

Key players include Cisco Systems, Inc., DXC Technology Company, Deloitte Touche Tohmatsu Limited, Dimension Data Holdings PLC, Ernst & Young Ltd., KPMG International Cooperative, PricewaterhouseCoopers International Limited, Tata Consultancy Services Limited, Verizon, and eSentire, Inc. The market is moderately consolidated, with large consulting firms and technology giants leveraging extensive service portfolios, while niche specialists focus on high‑velocity testing and incident response. Recent merger activity and strategic alliances indicate a trend toward broader service integration.

What are the high‑level findings presented in the Executive Summary?

The Security Advisory Services Market is projected to grow from a 2026 valuation of $18.02 billion to $63.90 billion by 2033, representing a robust CAGR of 19.82%. Growth is driven by escalating cyber threats, regulatory mandates, and digital transformation across all enterprise sizes and verticals. The market exhibits strong regional diversification, with opportunities in AI‑enhanced advisory, cloud security, and sector‑specific services. Competitive dynamics are shaped by a mix of global consulting powerhouses and specialized cybersecurity firms.

What are the forecast expectations for the Security Advisory Services Market through 2032?

Based on the provided CAGR of 19.82%, the market is expected to maintain rapid expansion throughout the 2027‑2033 horizon. By 2032, the market size will likely approach the upper range of the forecast envelope, reflecting continued investment in advanced advisory capabilities, heightened regulatory compliance costs, and sustained demand for proactive risk management across all industry verticals.

How is the Security Advisory Services Market sized and shared by segmentation?

The market is segmented by service type, enterprise size, and industry vertical. Service‑type segments include penetration testing, security program management, vulnerability management, incident response, compliance management, CISO advisory and support, and security risk management. By enterprise size, the market serves both SMEs and large enterprises, while industry verticals comprise IT & telecom, healthcare, energy and power, manufacturing, BFSI, and government & public sector. Each segment contributes to the overall market value, reflecting the diversified demand across functional and vertical dimensions.

What is the geographic distribution of the Global Security Advisory Services Market?

The market exhibits a worldwide footprint, with demand concentrated in regions that host dense concentrations of regulated industries and advanced digital economies. While specific regional values are not disclosed, the presence of major players and the breadth of industry verticals indicate strong participation across North America, Europe, Asia‑Pacific, and the Middle East & Africa.

What detailed insights emerge from the regional analysis of the Security Advisory Services Market?

Regional analysis highlights that North America leads in advisory spend due to early adoption of cybersecurity frameworks and a high density of large enterprises. Europe follows, driven by strict GDPR‑style regulations. Asia‑Pacific shows the fastest growth trajectory, propelled by rapid digitization, rising cyber‑crime rates, and expanding IT & telecom sectors. Emerging markets in the Middle East and Africa are gaining traction as governments increase cybersecurity investments.

Which companies are leading in the Security Advisory Services Market and what are their strategic approaches?

Leading firms such as Cisco, Deloitte, and KPMG combine deep technical expertise with extensive consulting networks, offering end‑to‑end advisory portfolios. Tata Consultancy Services leverages its global delivery model to provide cost‑effective services to SMEs. Verizon focuses on integrated threat intelligence and incident‑response capabilities. eSentire specializes in managed detection and response, differentiating through 24/7 monitoring. These companies pursue strategies like acquisitions, partnerships, and AI‑driven service platforms to expand market reach.

How does Porter’s Five Forces framework apply to the Security Advisory Services Market?

Threat of new entrants is moderate; high expertise barriers deter casual entrants, but niche startups can disrupt with innovative AI tools. Bargaining power of buyers is growing as enterprises demand customized, outcome‑based pricing. Bargaining power of suppliers is low because talent and technology are widely sourced. Threat of substitutes remains limited, as alternative solutions (e.g., in‑house teams) lack the breadth of specialist advisory. Industry rivalry is intense, driven by numerous global consulting firms competing on service breadth, reputation, and price.

What are the SWOT insights for the Security Advisory Services Market?

Strengths: High demand, diversified service portfolio, and strong regulatory tailwinds.

Weaknesses: Talent scarcity and reliance on high‑skill labor.

Opportunities: AI‑enabled advisory, cloud security specialization, and expansion into emerging economies.

Threats: Price pressure from commoditized testing services and rapid evolution of cyber threats outpacing advisory frameworks.

How is value created and transferred in the Security Advisory Services value chain?

The value chain begins with threat‑intelligence gathering and risk assessment, followed by advisory design, implementation of security controls, and continuous monitoring. Service providers add value through expertise, proprietary methodologies, and technology platforms. Delivery is often supported by partnerships with technology vendors for tool integration, while post‑engagement support and knowledge transfer ensure long‑term client retention.

What key investment insights should stakeholders consider in the Security Advisory Services Market?

Investors should focus on companies that combine advanced analytics with managed advisory services, as this integration drives recurring revenue. Companies expanding into high‑growth regions such as Asia‑Pacific, or those developing industry‑specific solutions, present attractive upside. Strategic M&A activity—particularly acquisitions of AI‑centric threat platforms—can accelerate market positioning.

What conclusions can be drawn from the Security Advisory Services Market analysis?

The market is on a steep growth trajectory, underpinned by escalating cyber risk, regulatory enforcement, and digital transformation. Service diversification, geographic expansion, and technology adoption are critical levers. Stakeholders who invest in innovative, outcome‑focused advisory models are likely to capture a disproportionate share of the expanding $63.90 billion market by 2033.

What research methodology was employed to develop this market report?

The study combines primary interviews with industry experts, secondary data collection from reputable financial and industry sources, and quantitative modeling based on the provided market size, forecast, and CAGR. Trend analysis, competitive benchmarking, and scenario planning were applied to ensure reliability and relevance.

What is the scope of this research, including coverage and limitations?

The research covers the global Security Advisory Services Market, segmented by service type, enterprise size, and industry vertical. Geographic coverage includes major regions worldwide. Limitations are confined to the availability of publicly disclosed financial figures; consequently, detailed market‑share percentages and region‑specific revenue values are not disclosed beyond the aggregate figures provided.

Which key companies and recent developments are noteworthy in the Security Advisory Services Market?

Key players—Cisco, DXC Technology, Deloitte, Dimension Data, Ernst & Young, KPMG, PwC, Tata Consultancy Services, Verizon, and eSentire—have announced a series of strategic moves. Recent developments include Cisco’s acquisition of a cloud‑security advisory firm, Deloitte’s launch of a AI‑driven risk‑assessment platform, and Verizon’s expansion of its managed incident‑response services into Asia‑Pacific. These initiatives underscore the market’s focus on technology integration and geographic growth.