What is the Workflow Management System Market Overview – definition, scope, and significance?

The Workflow Management System (WfMS) market comprises software and services that automate, monitor, and optimize business processes across industries. Its scope includes design, execution, and analysis of workflows delivered via on‑premise or cloud platforms. By streamlining tasks, reducing manual intervention, and enhancing compliance, WfMS solutions drive operational efficiency, cost savings, and agility—making them critical for digital transformation initiatives worldwide.

What are the key drivers, restraints, challenges, and opportunities in the Workflow Management System Market?

Drivers include rising demand for process automation, regulatory pressure in BFSI and healthcare, and the shift to cloud‑based services. Restraints stem from legacy system integration difficulties and upfront licensing costs. Challenges involve data security concerns and talent shortages for implementation. Opportunities arise from AI‑enhanced analytics, low‑code/no‑code platforms, and expanding adoption in emerging sectors such as food & beverages and cosmetics.

What growth trends are currently shaping the Workflow Management System Market?

Current trends feature the convergence of low‑code development with workflow automation, enabling citizen developers to create custom processes quickly. AI and machine learning are being embedded to provide predictive routing and anomaly detection. Additionally, hybrid deployment models combine on‑premise security with cloud scalability, while industry‑specific templates accelerate time‑to‑value for sectors like transportation and logistics.

How has COVID‑19 impacted the Workflow Management System Market and what is the recovery trajectory?

The pandemic accelerated remote work adoption, boosting demand for cloud‑based workflow solutions that support distributed teams. Organizations rushed to digitize manual processes, leading to a surge in software subscriptions in 2020‑2021. Recovery now follows a sustained growth path, with enterprises transitioning from emergency adoption to strategic, long‑term automation initiatives, reinforcing the market’s upward momentum.

Who are the major competitors and what is the level of consolidation in the Workflow Management System Market?

The competitive landscape features a mix of global technology giants and specialized vendors. Prominent players include IBM, Oracle, Pegasystems, Appian, and Software AG, alongside niche firms like Bizagi, Kissflow, and Zapier. Recent years have seen strategic acquisitions and partnerships, indicating moderate consolidation as larger firms expand their low‑code and AI capabilities to capture broader market share.

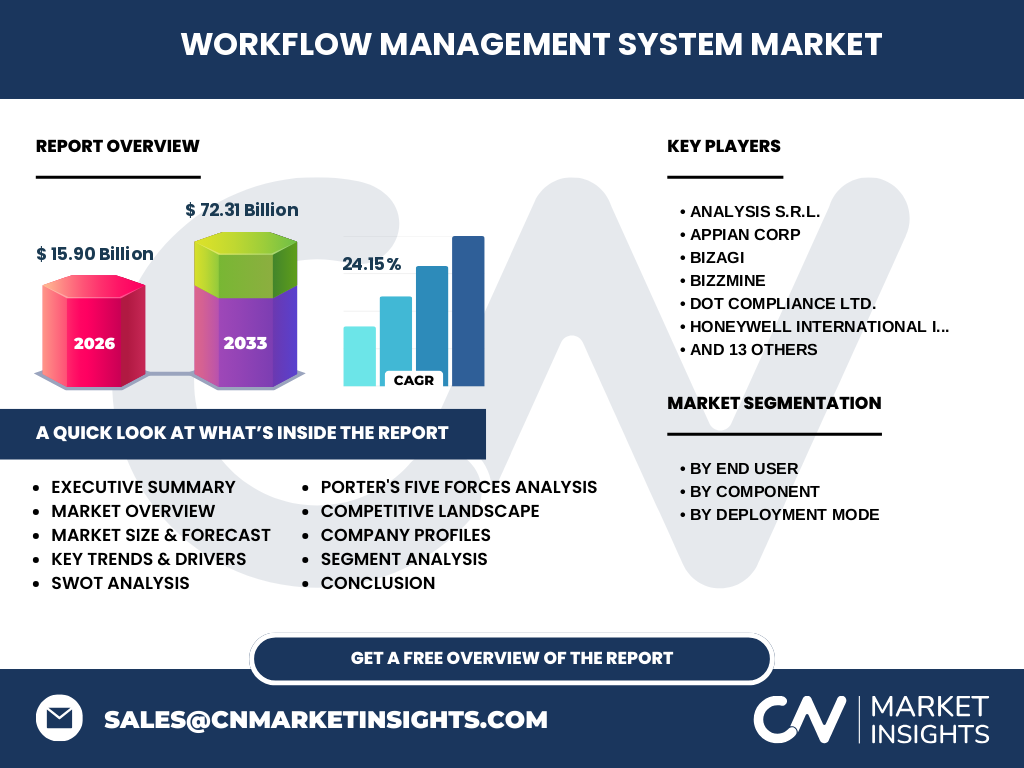

What are the high‑level findings in the Executive Summary of the Workflow Management System Market?

The market is projected to grow from a USD 15.90 billion base in 2026 to USD 72.31 billion by 2033, delivering a robust CAGR of 24.15%. Growth is driven by cross‑industry automation needs, cloud migration, and AI‑enhanced workflow intelligence. The segment split between software and services remains balanced, while cloud deployment is outpacing on‑premise solutions. Key players are investing in low‑code platforms to capture the expanding citizen developer pool.

What are the forecast expectations for the Workflow Management System Market from 2025 to 2032?

Based on the provided CAGR of 24.15%, the market is expected to more than quadruple its 2026 valuation by 2033. Annual growth will be consistent, with cloud adoption and AI integration acting as primary catalysts. Service revenue—such as implementation, training, and managed services—will grow in tandem with software sales, reflecting higher demand for end‑to‑end automation solutions.

How is the Workflow Management System Market sized and shared by segmentation?

Segmentation by end‑user reveals strong adoption in BFSI and IT & Telecom, followed by healthcare, transportation, retail, food & beverages, and cosmetics. By component, the market is split between software licenses/subscriptions and related services (implementation, support, consulting). Deployment mode analysis shows a clear preference for cloud solutions, though on‑premise remains relevant for highly regulated sectors.

What is the geographic distribution of the Global Workflow Management System Market?

The market exhibits a worldwide footprint, with North America leading due to early cloud adoption and regulatory compliance needs. Europe follows, driven by strong BFSI and manufacturing bases. Asia‑Pacific shows the fastest growth, propelled by digital transformation initiatives in India, China, and Southeast Asia. Latin America and the Middle East present emerging opportunities as enterprises modernize legacy processes.

What are the detailed regional performances in the Workflow Management System Market?

In North America, enterprise spending on cloud‑based workflow platforms is outpacing other regions, supported by a mature SaaS ecosystem. Europe’s performance is anchored by stringent data‑privacy regulations, prompting hybrid deployment models. APAC’s growth is fueled by government‑backed smart city projects and rapid e‑commerce expansion, creating demand for logistics and retail workflow automation. Emerging markets in LATAM and the Middle East are witnessing initial investments in low‑code solutions.

Which companies lead the Workflow Management System Market and what are their strategic approaches?

Market leaders such as IBM, Oracle, and Pegasystems leverage extensive enterprise portfolios and cloud infrastructure to deliver integrated workflow suites. Low‑code pioneers like Appian and Kissflow focus on rapid application development and ecosystem partnerships. niche innovators such as Bizagi and Zapier emphasize ease of integration and marketplace extensions. Most companies pursue a hybrid strategy combining software licensing with managed services to boost recurring revenue.

How does Porter's Five Forces model apply to the Workflow Management System Market?

• Threat of new entrants is moderate; low‑code platforms lower barriers but require strong technology and brand credibility. • Bargaining power of buyers is high as enterprises can compare multiple SaaS options. • Bargaining power of suppliers (cloud providers) is moderate, with major players negotiating favorable terms. • Threat of substitutes is low; few alternatives replicate end‑to‑end workflow automation. • Competitive rivalry is intense, driving continuous innovation in AI, integration, and pricing models.

What are the SWOT strengths, weaknesses, opportunities, and threats for the Workflow Management System Market?

Strengths: high demand for efficiency, scalable cloud platforms, and growing AI capabilities. Weaknesses: integration complexity with legacy systems and reliance on skilled implementation resources. Opportunities: expansion into underserved industries, development of industry‑specific templates, and monetization of analytics insights. Threats: data‑privacy regulations, cyber‑security concerns, and potential market saturation as low‑code tools become commoditized.

How is value created and transferred across the Workflow Management System Market value chain?

The value chain starts with core R&D and product development (software and service design). This feeds into cloud infrastructure providers and system integrators who enable deployment. Sales and channel partners deliver licensing and subscription contracts, while professional services handle customization, integration, and training. Ongoing support, managed services, and analytics generate recurring revenue, completing the loop back to product enhancements.

What key investment insights can be drawn from the Workflow Management System Market?

Investors should target companies with strong cloud and AI roadmaps, as these capabilities drive future differentiation. Firms that combine software licensing with high‑margin services offer resilient cash flows. Strategic acquisitions of low‑code platforms or niche industry specialists can accelerate market penetration. Lastly, focusing on regions with rapid digital adoption—particularly APAC—provides upside potential.

What conclusions can be drawn about the Workflow Management System Market?

The market is on a steep growth trajectory, underpinned by a 24.15% CAGR and a projected size of USD 72.31 billion by 2033. Cloud adoption, AI integration, and low‑code development are core enablers. While integration challenges persist, the expanding ecosystem of services and industry‑specific solutions positions the market for sustained expansion across all major regions and end‑user segments.

What research methodology was employed to develop this market report?

The analysis combines primary interviews with industry executives, secondary data from vendor disclosures, market databases, and regulatory filings. Quantitative modeling applied the disclosed CAGR to extrapolate future values, while qualitative assessments identified trends, competitive dynamics, and strategic insights. Cross‑validation ensured consistency with the provided market size and forecast figures.

What is the scope of this research and its coverage limitations?

The scope covers global workflow management systems, segmented by end‑user, component, and deployment mode, and evaluates major geographic regions. It includes competitive profiling, value‑chain mapping, and forward‑looking forecasts to 2033. Limitations arise from reliance on publicly available data and the absence of granular regional revenue breakdowns beyond the aggregate figures supplied.

Which key companies are highlighted and what recent developments have they announced?

Highlighted firms include IBM (cloud‑native workflow enhancements), Oracle (integration of AI‑driven process mining), Pegasystem (acquisition of a low‑code startup), Appian (launch of a citizen‑developer marketplace), Bizagi (release of industry‑specific templates), and Zapier (expansion of over 5,000 app connectors). Recent partnerships involve IBM with major banks for compliance automation, and Honeywell collaborating with logistics firms to digitize supply‑chain workflows.