What is the E‑House market and why is it important?

The E‑House market refers to the design, manufacture, and deployment of prefabricated, modular electrical substations—often called “e‑houses”—that integrate power equipment such as transformers, switchgear, busbars, and control systems within a single, factory‑built enclosure. The scope covers fixed and mobile substations, all major components (transformer, bus bar, power management system, variable frequency drive, switchgear, HVAC), and end‑use applications in industrial facilities and utility networks. E‑houses simplify on‑site construction, reduce commissioning time, and enhance safety, making them a critical enabler for the rapid expansion of power infrastructure worldwide.

What are the main drivers, restraints, challenges, and opportunities shaping the E‑House market?

Key drivers include the global push for grid modernization, increasing renewable energy integration, and the need for compact, quickly deployable substations in remote or urban sites. Growing industrial automation and the expansion of data‑center power capacity also boost demand. Restraints stem from high upfront capital costs and the specialized engineering expertise required for custom solutions. Challenges involve regulatory compliance across regions and the logistical complexity of transporting large modules. Opportunities arise from advances in digital monitoring, the adoption of modular HVAC and variable frequency drives, and the expanding market for mobile substations in mining and construction projects.

What current and emerging trends are influencing the growth of the E‑House market?

Current trends include a shift toward smart substations equipped with IoT sensors and advanced power management systems that enable real‑time condition monitoring and predictive maintenance. Manufacturers are increasingly offering integrated HVAC solutions that improve energy efficiency and reduce the footprint of the enclosure. Emerging trends feature the use of lightweight composite panels for mobile e‑houses, facilitating faster deployment in temporary sites. Additionally, there is a growing preference for modular designs that allow customers to add or upgrade components such as variable frequency drives without major retrofits.

How did COVID‑19 affect the E‑House market and what is the recovery trajectory?

The pandemic caused temporary project delays and supply‑chain disruptions, particularly for critical components like transformers and switchgear. However, the inherent advantages of prefabrication—reduced on‑site labor and accelerated installation—made e‑houses attractive during the recovery phase. As economies reopened, demand rebounded swiftly, especially in regions prioritizing resilient power infrastructure. The market is now on a clear upward trajectory, supported by renewed investment in utility upgrades and industrial expansions.

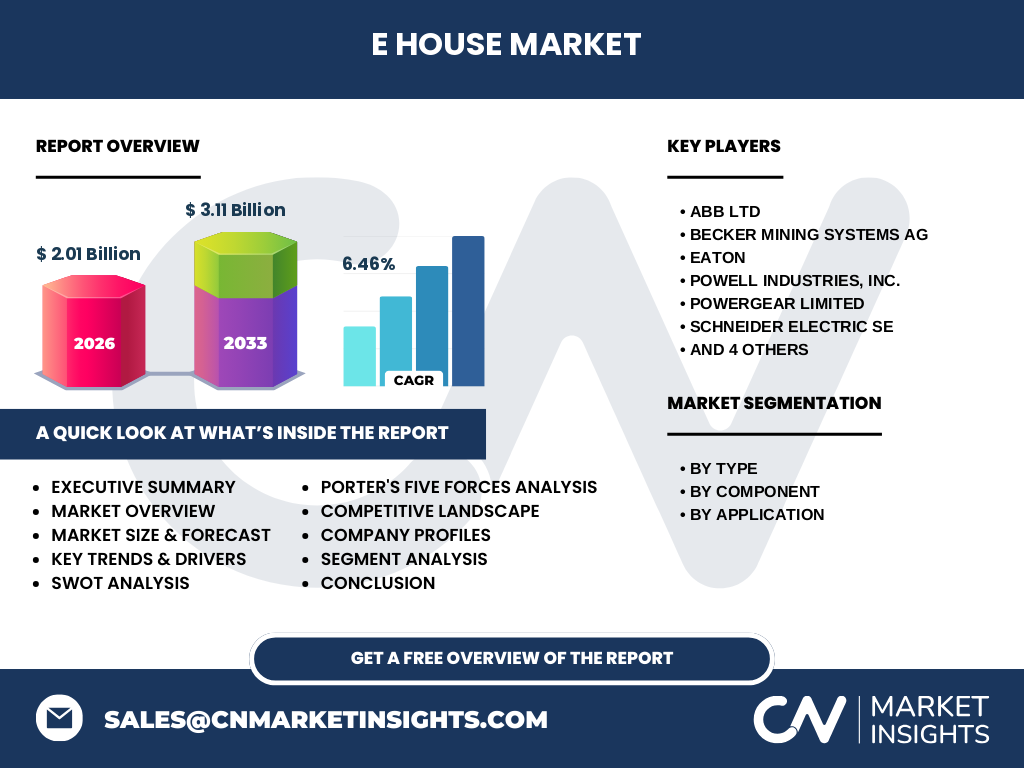

Who are the major competitors in the E‑House market and how is consolidation evolving?

The competitive landscape is dominated by established electrical equipment manufacturers and specialized e‑house providers. Leading players include ABB Ltd, Siemens AG, Schneider Electric SE, Eaton, Becker Mining Systems AG, Powell Industries, Inc., Powergear Limited, StarFlite Systems, S√©cheron, and WEG. These firms compete on engineering expertise, product breadth, and global service networks. Recent years have seen strategic partnerships and acquisitions aimed at expanding component portfolios—particularly in digital controls and HVAC—indicating a moderate level of consolidation as companies seek end‑to‑end solutions.

What are the high‑level findings of the E‑House market research?

The market is valued at $2.01 billion in 2026 and is projected to reach $3.11 billion by 2033, delivering a compound annual growth rate (CAGR) of 6.46 % over the forecast period. Fixed substations hold the larger share due to steady utility upgrades, while mobile substations are gaining momentum in mining and construction. Transformer and switchgear remain the most critical components, complemented by growing demand for integrated power management systems and HVAC. Geographic growth is strongest in regions with intensive infrastructure investment, and leading vendors continue to broaden their digital and modular capabilities.

What are the forecast expectations for the E‑House market from 2025 to 2032?

Based on the provided CAGR of 6.46 %, the market is expected to maintain steady expansion through 2032. The forecast reflects continued adoption of smart, modular substations, reinforced by utility modernization programs and the need for resilient power solutions in industrial sites. The growth trajectory suggests that by the end of the forecast horizon, the market will have surpassed the $3 billion mark, reinforcing the attractiveness of the sector for investors and technology developers.

How is the E‑House market sized and shared across key segments?

Segmentation by type shows two primary categories: Fixed Substation and Mobile Substation. By component, the market is divided among Transformer, Bus Bar, Power Management System, Variable Frequency Drive, Switchgear, and HVAC. Application segmentation includes Industrial and Utilities. While exact monetary shares are not disclosed, the prominence of transformers and switchgear across both fixed and mobile e‑houses indicates they command the largest portion of component spend, with HVAC and variable frequency drives representing emerging growth pockets, especially in mobile configurations.

What is the geographic distribution of the global E‑House market?

The market exhibits a worldwide footprint with strong demand in regions pursuing grid upgrades and industrial expansion. Although precise regional figures are not provided, the presence of multinational vendors such as ABB, Siemens, and Schneider Electric—each with extensive global operations—suggests balanced participation across North America, Europe, and Asia‑Pacific, with emerging opportunities in Latin America and the Middle East driven by renewable integration projects.

What are the key performance highlights for each major region?

In North America, utility modernization and the growth of data‑center clusters drive fixed‑substation sales, while mobile e‑houses support mining and offshore projects. Europe benefits from stringent grid reliability standards and strong regulatory support for modular substations, fostering both fixed and mobile deployments. The Asia‑Pacific region leads in volume due to rapid industrialization, large‑scale renewable integration, and extensive infrastructure programs, creating robust demand for all component categories. Latin America and the Middle East are witnessing early‑stage adoption, primarily in utility‑driven projects aiming to improve power quality and resiliency.

Which companies are leading the E‑House market and what strategies are they employing?

ABB Ltd leverages its extensive transformer and switchgear portfolio to offer integrated e‑house solutions, emphasizing digital connectivity. Siemens AG focuses on modular design and advanced HVAC integration, targeting industrial customers. Schneider Electric SE promotes IoT‑enabled power management systems, enhancing remote monitoring capabilities. Eaton differentiates through flexible financing and aftermarket services. Becker Mining Systems AG specializes in mobile substations for the mining sector, while Powell Industries, Inc. and Powergear Limited expand their presence through strategic partnerships with local system integrators. StarFlite Systems and S√©cheron concentrate on niche applications, and WEG capitalizes on its expertise in variable frequency drives to add value to mobile e‑houses.

How does Porter's Five Forces model apply to the E‑House market?

• Threat of new entrants is moderate; high capital requirements and technical expertise create barriers, yet modular construction trends lower entry costs for specialized firms.

• Bargaining power of suppliers is relatively low because component manufacturers (transformer, switchgear) are numerous, though shortages can temporarily elevate power.

• Bargaining power of buyers is moderate; large utilities and industrial clients can negotiate volume discounts, but they depend on the specialized integration capabilities of vendors.

• Threat of substitutes is low; traditional on‑site substations are less competitive due to longer lead times and higher labor costs.

• Rivalry among existing firms is high, driven by innovation in digital monitoring, HVAC efficiency, and modular flexibility.

What are the SWOT insights for the overall E‑House market?

Strengths: Rapid deployment, reduced on‑site labor, high safety standards, and integrated digital monitoring.

Weaknesses: High initial investment, dependence on specialized engineering talent, and logistical challenges for large modules.

Opportunities: Expansion of renewable energy grids, growing demand for mobile substations in mining and construction, and advancements in IoT‑based power management.

Threats: Supply‑chain volatility for critical components, regulatory divergence across regions, and potential saturation in mature utility markets.

How is value created and transferred within the E‑House value chain?

The value chain begins with raw material sourcing for steel enclosures and electrical steel for transformers, followed by component manufacturing (transformers, switchgear, busbars). These components are then assembled into modular units within a factory setting, where integration of power management systems, HVAC, and control software occurs. After rigorous factory testing, the complete e‑house is shipped to the customer site, where installation and commissioning are carried out by specialized service teams. Post‑sale services—including monitoring, maintenance, and upgrade pathways—complete the cycle, generating recurring revenue for manufacturers.

What investment insights should stakeholders consider when entering the E‑House market?

Investors should prioritize companies with strong digital platforms and proven integration capabilities, as these attributes differentiate offerings in a competitive market. Funding projects that couple e‑houses with renewable energy sites can capture policy‑driven incentives. Partnerships with logistics providers can mitigate transportation challenges for mobile units. Finally, allocating capital to R&D in lightweight materials and advanced HVAC systems can unlock new market segments and improve profit margins.

What are the concluding takeaways from the E‑House market analysis?

The E‑House market is on a robust growth path, underpinned by a $2.01 billion base in 2026 and a projected $3.11 billion valuation by 2033, reflecting a steady 6.46 % CAGR. Fixed substations dominate, yet mobile solutions are gaining traction across mining and temporary industrial projects. Digital integration, modular design, and HVAC efficiency are the primary levers of competitive advantage. Geographic expansion remains a key driver, especially in Asia‑Pacific, while mature markets continue to upgrade existing infrastructure.

What research methodology was used to compile this market report?

The study combined primary interviews with industry experts, OEM technical teams, and key end‑users, together with secondary data extraction from company annual reports, press releases, and reputable industry databases. Trend analysis, CAGR calculations, and qualitative assessments were applied to synthesize the findings. All financial figures reflect the latest available data and are presented in US dollars.

What is the scope of this research and its limitations?

The scope covers global E‑House market dynamics, segmented by type, component, and application, with a regional overview for major geographic zones. It includes competitive profiling of ten leading manufacturers and a forward‑looking forecast to 2033. Limitations stem from the reliance on publicly disclosed information; proprietary sales data and confidential pricing structures were not accessible, so the analysis focuses on qualitative insights and the provided quantitative benchmarks.

Which key companies have announced recent developments in the E‑House market?

ABB Ltd launched a next‑generation digital substation platform featuring AI‑based fault detection. Siemens AG introduced a lightweight composite enclosure for mobile e‑houses, reducing transport weight by 15 %. Schneider Electric SE announced a partnership with a leading cloud provider to deliver remote monitoring-as-a-service for utility customers. Eaton released an integrated variable frequency drive with built‑in predictive maintenance analytics. Becker Mining Systems AG secured a multi‑year contract to supply mobile substations for a South American copper mine, highlighting the growing demand for mobile solutions.