What is the Handheld Ultrasound Scanners Market Overview – definition, scope, and significance?

The Handheld Ultrasound Scanners Market comprises portable, battery‑operated imaging devices that deliver real‑time 2D, 3D/4D and Doppler ultrasound capabilities. These scanners are designed for point‑of‑care use across hospitals, clinics, ambulances and field settings, enabling rapid diagnostics without the infrastructure of traditional cart‑based systems. Their significance lies in improving access to imaging, reducing patient transport, and supporting tele‑medicine workflows, thereby expanding the reach of quality healthcare.

What are the Handheld Ultrasound Scanners Market drivers, restraints, challenges, and opportunities?

Key drivers include rising demand for point‑of‑care diagnostics, expanding applications in emergency medicine and primary care, and declining device costs due to advances in semiconductor and battery technology. Restraints involve regulatory complexities and the need for skilled operators to ensure image quality. Challenges stem from data security concerns in connected devices and competition from traditional ultrasound manufacturers. Opportunities arise from AI‑enhanced image analysis, integration with electronic health records, and growth in emerging markets seeking affordable imaging solutions.

What are the current Handheld Ultrasound Scanners Market growth trends?

Current trends feature a shift toward AI‑assisted interpretation, enabling less‑trained clinicians to obtain diagnostic‑grade images. Manufacturers are expanding portfolios to include 3D/4D and Doppler capabilities in handheld form factors. Another trend is the growing adoption of cloud‑based image storage and remote consultation, supporting tele‑ultrasound programs. Subscription‑based pricing models are also emerging, lowering upfront capital barriers for smaller practices.

How did COVID‑19 impact the Handheld Ultrasound Scanners Market and what is the recovery trajectory?

The pandemic accelerated demand for portable imaging that could be deployed at bedside while minimizing equipment contamination. Hospitals adopted handheld units for rapid lung assessment and cardiac monitoring, leading to a noticeable uptick in sales in 2020‑2021. Post‑pandemic, the market retained momentum as clinicians recognized the operational efficiencies and infection‑control benefits, supporting a steady recovery and continued growth trajectory.

What does the Handheld Ultrasound Scanners Market competitive landscape look like?

The market is moderately consolidated, with a mix of established OEMs and agile startups. Leading players such as GE HealthCare Technologies Inc., Philips, Siemens Healthineers AG, and FujiFilm SonoSite dominate traditional segments, while innovators like Butterfly Network Inc., Clarius Mobile Health Corp., and EchoNous Inc. focus on cloud‑enabled, AI‑driven handheld solutions. Recent M&A activity highlights strategic consolidation aimed at expanding product portfolios and geographic reach.

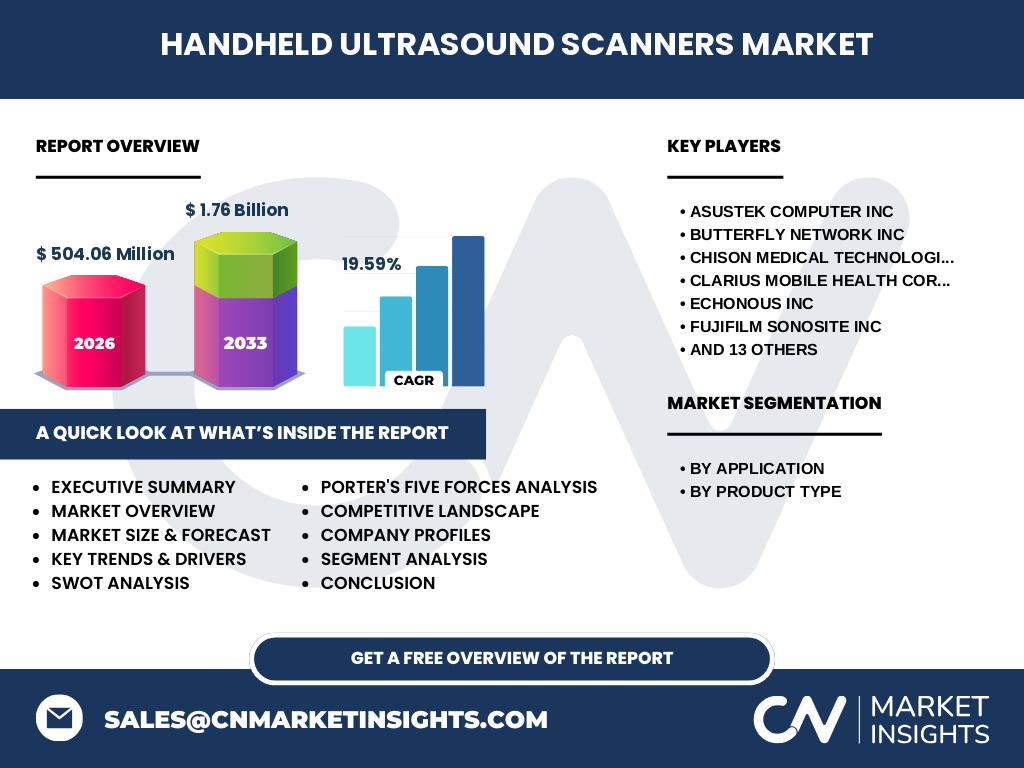

What are the key findings in the Executive Summary of the Handheld Ultrasound Scanners Market?

The market, valued at USD 504.06 million in 2026, is projected to reach USD 1.76 billion by 2033, delivering a robust CAGR of 19.59 %. Growth is driven by expanding clinical applications, technological advances, and heightened awareness of point‑of‑care imaging. Geographic uptake is strongest in North America and Europe, while Asia‑Pacific presents the fastest growth potential due to rising healthcare expenditures and large underserved populations.

What are the Handheld Ultrasound Scanners Market forecasts for 2025‑2032?

Based on the provided CAGR of 19.59 %, the market is expected to more than triple its 2026 size by 2033. Forecasts indicate sustained double‑digit expansion through 2032, underpinned by continuous product innovation, increasing reimbursement for bedside imaging, and broader adoption in specialty fields such as cardiology and musculoskeletal care.

What is the Handheld Ultrasound Scanners Market size and share by segmentation?

Segmentation by application includes Gynecology, Neurology, Cardiology, Urology, Aesthetics, Musculoskeletal, Veterinary and Other Applications. By product type, the market is divided into 2D Handheld Ultrasound Scanners, 3D/4D Handheld Ultrasound Scanners, and Doppler Ultrasound. While precise share percentages are not disclosed, the diversification across these segments reflects the technology’s adaptability to both clinical and veterinary settings, with cardiology and musculoskeletal applications gaining notable traction.

What is the global Handheld Ultrasound Scanners market size and share by region?

The global market totaled USD 504.06 million in 2026. Although regional split figures are not detailed, North America leads in adoption due to early technology uptake and favorable reimbursement policies, followed by Europe. Asia‑Pacific is emerging rapidly, driven by expanding healthcare infrastructure and cost‑sensitive demand, while Latin America and the Middle East present incremental growth opportunities.

What does the regional analysis of the Handheld Ultrasound Scanners market reveal?

North America’s high penetration stems from strong R&D ecosystems and large hospital networks. Europe benefits from unified regulatory frameworks and integrated health systems that favor portable imaging. Asia‑Pacific’s growth is propelled by government initiatives to improve rural healthcare access and increasing private‑sector investments. Emerging markets in Latin America and Africa exhibit nascent demand, primarily for basic 2D handheld units.

Which leading companies are profiled in the Handheld Ultrasound Scanners market and what are their strategies?

Key players include ASUSTek Computer Inc., Butterfly Network Inc., CHISON Medical Technologies Co., Clarius Mobile Health Corp., EchoNous Inc., FUJIFILM SonoSite Inc., GE HealthCare Technologies Inc., Guangzhou SonoHealth Medical Technologies Co., Healcerion Co., Koninklijke Philips NV, Nipro Medical Corp., Shenzhen Mindray Bio‑Medical Electronics Co. Ltd., Siemens Healthineers AG, Sonoscanner, TERASON DIVISION TERATECH CORPORATION, Vave Health, and FUKUDA DENSHI. Strategies focus on AI integration, expanding 3D/4D capabilities, leveraging cloud platforms for remote diagnostics, and pursuing strategic partnerships to broaden distribution channels.

How does Porter’s Five Forces analysis apply to the Handheld Ultrasound Scanners market?

Threat of new entrants is moderate; low entry barriers exist for software‑centric startups, but hardware development requires significant capital. Bargaining power of buyers is high as clinicians demand superior image quality and cost efficiency. Bargaining power of suppliers is moderate, centered on semiconductor and battery components. Threat of substitutes is low; alternative imaging modalities cannot match the portability of handheld ultrasound. Industry rivalry is intense, with innovation and pricing driving competition.

What are the SWOT highlights for the Handheld Ultrasound Scanners market?

Strengths: portability, rapid diagnostics, and decreasing device cost.

Weaknesses: limited penetration in low‑resource settings due to training needs.

Opportunities: AI‑driven decision support, tele‑ultrasound expansion, and emerging market demand.

Threats: regulatory hurdles and potential data‑privacy concerns in connected devices.

What does the Handheld Ultrasound Scanners market value chain look like?

The value chain starts with semiconductor and sensor component suppliers, followed by hardware assembly and software development firms that embed AI algorithms. Manufacturers then distribute devices through medical device distributors, direct sales teams and online platforms. Post‑sale services include training, maintenance contracts, and cloud‑based image storage solutions, creating recurring revenue streams for vendors.

What key investment insights can be drawn from the Handheld Ultrasound Scanners market?

Investors should prioritize companies that combine robust hardware with AI‑enhanced software, as this synergy drives clinical adoption. Firms with subscription‑based service models and strong cloud ecosystems are positioned for recurring income. Geographically, allocating capital toward players expanding in Asia‑Pacific offers upside due to the region’s rapid adoption curve.

What conclusions can be drawn about the Handheld Ultrasound Scanners market?

The handheld ultrasound sector is experiencing a transformative growth phase, underpinned by a 19.59 % CAGR and a projected market size of USD 1.76 billion by 2033. Technological innovation, expanding clinical use cases, and favorable reimbursement environments collectively suggest a durable, high‑growth trajectory that will continue reshaping point‑of‑care diagnostics.

What research methodology was employed for this Handheld Ultrasound Scanners market report?

The study combined primary interviews with industry experts, surveys of key opinion leaders, and secondary data collection from company filings, regulatory databases, and reputable market intelligence sources. Quantitative analysis utilized compound annual growth rate calculations and trend extrapolation, while qualitative insights were derived from expert consensus and competitive benchmarking.

What is the scope of this Handheld Ultrasound Scanners market research?

The research covers global market dimensions, segmentation by application and product type, regional performance, competitive dynamics, and forward‑looking forecasts to 2033. It excludes detailed financial statements of individual companies and does not quantify market share percentages beyond the provided aggregate figures.

Which key companies and recent developments are highlighted in the Handheld Ultrasound Scanners market?

Notable developments include Butterfly Network’s launch of a cloud‑native AI imaging platform, GE HealthCare’s acquisition of a micro‑electronics firm to enhance sensor resolution, Philips’ partnership with tele‑health providers to integrate handheld units into remote care pathways, and Siemens Healthineers’ introduction of a 3D/4D handheld model targeting cardiology. These initiatives illustrate the sector’s focus on software integration, advanced imaging modes, and ecosystem expansion.