What is the Computer Aided Engineering Market Overview – Definition, scope, and significance?

The Computer Aided Engineering (CAE) market comprises software and services that enable engineers to simulate, analyze, and optimize product designs across the product development lifecycle. It includes tools for finite element analysis, computational fluid dynamics, multi‑physics, and system‑level simulations. The scope extends from early concept modeling to detailed verification in industries such as automotive, aerospace, electronics, and medical devices. CAE is significant because it reduces physical prototyping cycles, cuts development costs, and accelerates time‑to‑market, thereby enhancing competitiveness for manufacturers worldwide.

What are the primary drivers, restraints, challenges, and opportunities shaping the Computer Aided Engineering Market?

Key drivers include rising demand for lightweight, high‑performance products, increasing regulatory scrutiny that mandates rigorous validation, and the growing adoption of digital twins and Industry 4.0 frameworks. Restraints arise from high upfront licensing costs and the steep learning curve associated with advanced simulation tools. Challenges involve data integration across legacy PLM systems and the need for skilled analysts. Opportunities are emerging in cloud‑based deployment models, AI‑enhanced optimization algorithms, and expanding usage in emerging sectors such as renewable energy and smart medical devices.

What are the current growth trends in the Computer Aided Engineering Market?

Current trends show a shift from traditional on‑premises installations toward cloud‑based platforms that offer scalability and subscription pricing. AI and machine learning are being embedded to automate mesh generation and result interpretation. Multi‑physics integration is becoming standard, enabling simultaneous structural, thermal, and fluid analyses. Additionally, the rise of low‑code simulation environments is democratizing CAE access for non‑specialist engineers, broadening the user base.

How has COVID‑19 impacted the Computer Aided Engineering Market and what is the recovery trajectory?

The pandemic initially disrupted hardware procurement and delayed large‑scale plant projects, causing a short‑term dip in new CAE license sales. However, remote collaboration tools and cloud solutions mitigated the impact, leading to accelerated adoption of virtual engineering. As supply chains recover, demand is rebounding strongly, supported by the need for rapid product redesign to meet post‑pandemic market shifts, positioning the market on a robust growth path.

What does the competitive landscape of the Computer Aided Engineering Market look like?

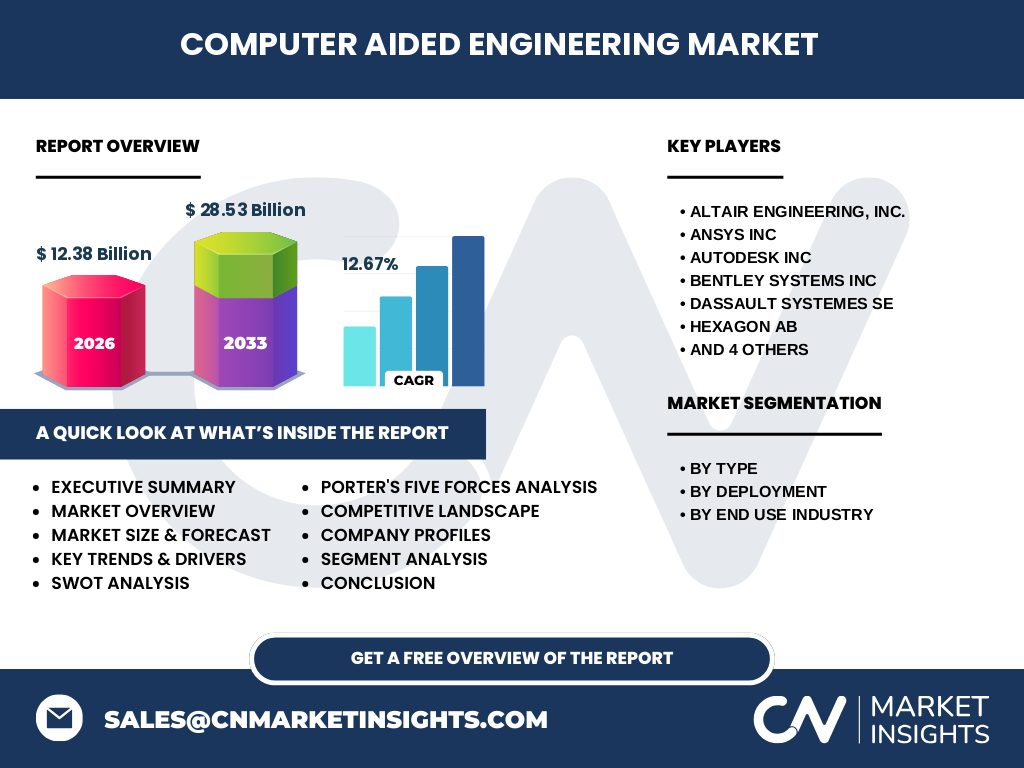

The market is highly concentrated, with major players such as Altair Engineering, Ansys, Autodesk, Bentley Systems, Dassault Systèmes, Hexagon, PTC, Siemens, Satven, and Technosoft Engineering Projects Ltd. competing across the product spectrum. Consolidation has intensified through strategic acquisitions that expand functionality (e.g., AI modules or cloud capabilities). Competitive differentiation focuses on breadth of simulation libraries, integration with PLM/IoT ecosystems, and flexible deployment options.

What are the key findings in the Executive Summary of the Computer Aided Engineering Market?

The CAE market is valued at $12.38 billion in 2026 and is projected to reach $28.53 billion by 2033, reflecting a robust CAGR of 12.67 %. Growth is propelled by cloud adoption, AI‑driven simulation, and expanding use in high‑growth end‑use industries. The market is globally diversified, with strong demand in North America, Europe, and Asia‑Pacific. Competitive pressures are heightened by ongoing M&A activity and the emergence of subscription‑based pricing models.

What are the forecast expectations for the Computer Aided Engineering Market from 2025 to 2032?

Based on the provided CAGR of 12.67 %, the market is expected to continue expanding steadily through 2032, surpassing the $28 billion mark by the end of the forecast horizon. The forecast anticipates accelerated uptake of cloud‑based solutions, incremental revenue from AI‑enhanced modules, and increasing subscription‑type contracts that provide recurring revenue streams for vendors.

How is the Computer Aided Engineering Market sized and shared by segmentation?

Segmentation by type includes Online TDLS and Lab TDLS, reflecting two primary delivery models for testing and data logging services. By deployment, the market splits between On‑Premises installations and Cloud‑based offerings, with cloud gaining market share due to its flexibility. End‑use industry segmentation covers Automotive, Defense & Aerospace, Electronics, Medical Devices, Industrial Equipment, and Others, each leveraging CAE to meet sector‑specific performance and compliance requirements.

What is the geographic distribution of the Global Computer Aided Engineering Market?

The market exhibits a balanced global footprint. North America leads in early adoption of advanced simulation and cloud services, while Europe maintains strong demand driven by automotive and aerospace clusters. Asia‑Pacific shows the fastest growth rate, fueled by burgeoning manufacturing bases and increased investment in digital transformation. The overall geographic mix underscores a worldwide shift toward virtual engineering.

What does the regional analysis reveal about Computer Aided Engineering Market performance?

In North America, enterprise‑level integration with PLM and strong R&D spending sustain high market penetration. Europe’s automotive heritage drives extensive use of structural and crash simulation tools. Asia‑Pacific’s rapid industrialization and cost‑sensitive manufacturers accelerate cloud adoption, especially for small‑to‑medium enterprises. Emerging markets in Latin America and the Middle East present nascent but growing opportunities as local industries modernize.

Which companies lead the Computer Aided Engineering Market and what are their strategies?

Leading firms—Altair, Ansys, Autodesk, Bentley Systems, Dassault Systèmes, Hexagon, PTC, Siemens, Satven, and Technosoft—pursue strategies such as expanding cloud platforms, integrating AI/ML capabilities, forging partnerships with OEMs, and acquiring niche technology providers. Many focus on subscription licensing to create predictable revenue, while others emphasize vertical solutions tailored to automotive, aerospace, or medical device regulations.

How does Porter’s Five Forces framework apply to the Computer Aided Engineering Market?

Threat of new entrants is moderate due to high development costs and established brand equity. Bargaining power of buyers is rising as customers demand flexible, subscription‑based pricing and interoperability. Supplier power is low because most software components are internally developed. Rivalry among existing firms is intense, driven by innovation cycles and frequent acquisitions. The threat of substitutes remains limited, as few alternatives match the fidelity of dedicated CAE tools.

What are the SWOT insights for the Computer Aided Engineering Market?

Strengths: High technical barriers, strong demand across multiple verticals, and proven ROI for manufacturers.

Weaknesses: Complex licensing structures and steep learning curves.

Opportunities: Cloud migration, AI‑driven automation, and expansion into emerging industries such as renewable energy.

Threats: Economic downturns affecting capital‑intensive sectors and potential commoditization of basic simulation functions.

What does the value chain of the Computer Aided Engineering Market look like?

The value chain starts with research and development of algorithms, followed by software engineering, licensing, and distribution (on‑premises or cloud). Next are implementation services, training, and technical support. Downstream, users integrate CAE outputs into product design, testing, and compliance processes, creating feedback loops that drive further software enhancements.

What key investment insights can be drawn for the Computer Aided Engineering Market?

Investors should prioritize companies with strong cloud portfolios and AI integration, as these align with the market’s growth trajectory. Firms demonstrating recurring revenue models and strategic acquisitions of niche technology providers present lower risk. Additionally, targeting vendors with deep vertical expertise—especially in automotive and medical devices—offers exposure to sectors with high regulatory‑driven simulation demand.

What are the concluding takeaways for the Computer Aided Engineering Market?

The CAE market is on a pronounced expansion path, underpinned by a 12.67 % CAGR and a projected valuation of $28.53 billion by 2033. Cloud adoption, AI‑enhanced tools, and sector‑specific solutions are the primary growth engines. While competitive pressures are high, firms that innovate in deployment flexibility and user experience will capture the greatest share of future revenues.

How was the research for this report conducted?

The methodology combined primary interviews with industry executives, secondary analysis of company filings, market reports, and reputable databases. Trend extrapolation used the provided CAGR and market size figures, while qualitative insights were derived from expert commentary and recent product announcements.

What is the scope of this research?

The scope covers global CAE market size, segmentation by type, deployment, and end‑use industry, as well as regional performance, competitive dynamics, and forward‑looking forecasts through 2033. It excludes detailed financial breakdowns beyond the provided aggregate figures and does not quantify market share percentages for individual vendors.

Which key companies have announced recent developments in the Computer Aided Engineering Market?

Altair Engineering released a cloud‑native simulation platform that integrates AI‑based mesh optimization. Ansys introduced an expanded suite for electronic thermal analysis. Autodesk launched a subscription model for its Fusion 360 simulation tools. Dassault Systèmes announced a partnership with a leading automotive OEM to co‑develop digital twin workflows. Siemens unveiled a new Industrial Edge solution that brings CAE analytics to the shop floor. These initiatives illustrate a market-wide push toward cloud, AI, and industry collaboration.