What is the Utility Communication Market and why is it significant?

The Utility Communication Market encompasses technologies, services, and solutions that enable the exchange of data between utility providers—both private and public—and their customers, assets, and operational systems. It includes wired and wireless communication infrastructures that support smart grids, demand‑response programs, outage management, and real‑time monitoring. The market is significant because reliable, secure communication is the backbone of modern utility operations, driving efficiency, regulatory compliance, and the transition to renewable energy sources.

What are the main drivers, restraints, challenges, and opportunities shaping the Utility Communication Market?

Key drivers include the global push for smart grid deployment, increasing renewable integration, and the need for high‑speed data transmission to support IoT‑enabled devices. Restraints stem from high capital expenditures for infrastructure upgrades and stringent data‑security regulations. Challenges involve legacy system compatibility, cybersecurity threats, and varying standards across regions. Opportunities arise from the growth of 5G and low‑power wide‑area networks, edge‑computing adoption, and emerging services such as predictive maintenance and advanced analytics.

Which growth trends are currently influencing the Utility Communication Market?

Current trends feature a shift toward wireless solutions, driven by the flexibility of cellular and LPWAN technologies for remote asset monitoring. There is also a rise in hybrid communication architectures that combine wired reliability with wireless agility. The adoption of cloud‑based platforms for data aggregation and the integration of AI for grid optimization are emerging trends that are reshaping how utilities manage and analyze communication data.

How did COVID‑19 affect the Utility Communication Market and what is the recovery outlook?

The pandemic temporarily slowed new infrastructure projects due to supply‑chain disruptions and reduced capital spending. However, the crisis highlighted the importance of resilient communication networks for remote monitoring and emergency response. Post‑COVID recovery has been swift, with utilities accelerating digital transformation to improve operational continuity, leading to a rebound in investment and a continued upward trajectory.

Who are the major competitors in the Utility Communication Market and what is the level of market consolidation?

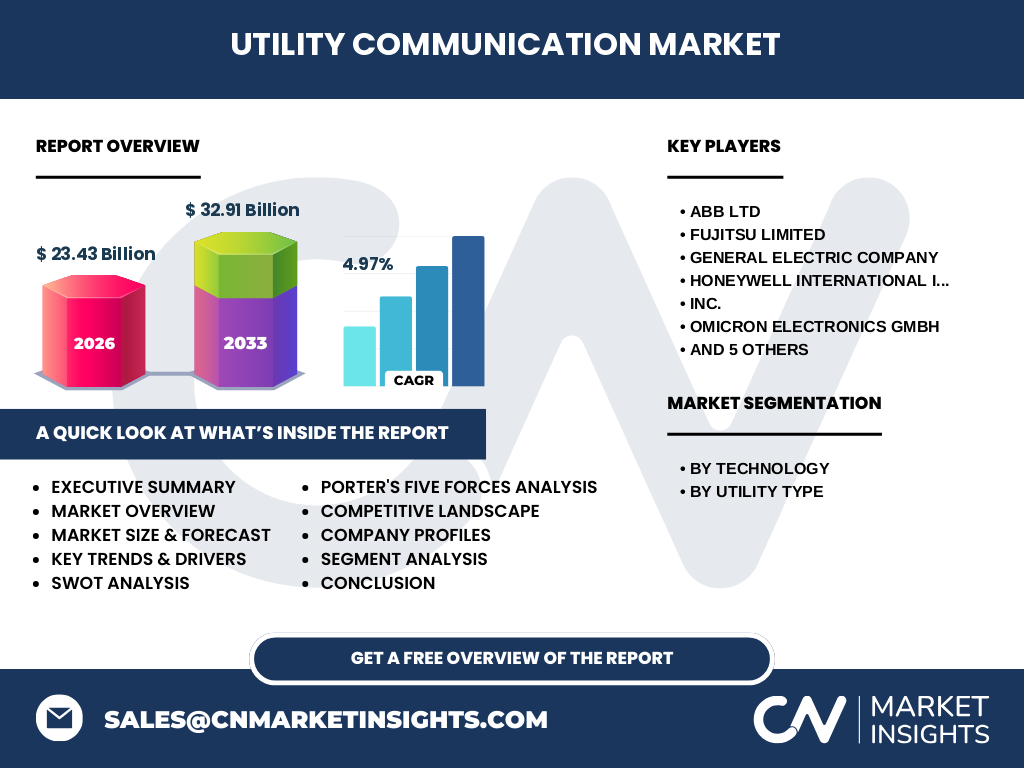

Key players include ABB Ltd, FUJITSU LIMITED, General Electric Company, Honeywell International Inc, OMICRON Electronics GmbH, Rockwell Automation, Schneider Electric SE, Siemens AG, Tejas Networks, and Telefonaktiebolaget LM Ericsson. The market exhibits moderate consolidation, as large multinational firms acquire niche technology providers to broaden their communication portfolios, while strategic partnerships are common for co‑development of standards‑compliant solutions.

What are the high‑level findings of the Utility Communication Market study?

The market is valued at $23.43 billion in 2026 and is projected to reach $32.91 billion by 2033, reflecting a CAGR of 4.97 %. Growth is driven by smart‑grid adoption, renewable integration, and the expansion of wireless communication technologies. While capital intensity and cybersecurity remain concerns, opportunities in 5G, edge computing, and AI‑driven analytics are expected to sustain long‑term expansion across both private and public utility segments.

What are the forecast expectations for the Utility Communication Market from 2025 to 2032?

Based on the provided CAGR of 4.97 %, the market is anticipated to continue expanding at a steady rate through 2032, moving from its 2026 base of $23.43 billion toward the forecast horizon of $32.91 billion by 2033. This growth suggests consistent demand for both wired and wireless solutions, with increasing investment in digital infrastructure by utilities worldwide.

How is the Utility Communication Market sized and shared by technology and utility type segments?

The market is segmented by technology into wired and wireless categories, each addressing distinct operational needs. Wired solutions remain essential for high‑capacity, low‑latency backbone networks, while wireless offerings are gaining traction for distributed assets and remote monitoring. By utility type, the market serves private utilities—often focused on industrial or campus‑scale operations—and public utilities that manage larger, region‑wide grids. Both segments benefit from advances in communication standards, though the share distribution reflects the complementary role of each technology in meeting diverse utility requirements.

What is the geographic distribution of the Utility Communication Market?

The market exhibits a global footprint, with significant activity in North America, Europe, and Asia‑Pacific. These regions host the majority of utility digitalization projects and infrastructure upgrades, driven by regulatory support and mature electricity markets. While specific regional revenue figures are not disclosed, the overall market growth is underpinned by coordinated investments across these key geographies.

How does the Utility Communication Market perform across different regions?

In North America, utilities prioritize grid modernization and cybersecurity, fostering strong demand for both wired and wireless solutions. Europe emphasizes renewable integration and regulatory compliance, driving adoption of advanced communication platforms. Asia‑Pacific leads in rapid infrastructure development, with emerging economies investing heavily in smart‑grid deployments. Each region’s performance is shaped by local policy frameworks, technology readiness, and the scale of utility networks.

Which companies lead the Utility Communication Market and what strategies are they employing?

Leading firms such as Siemens AG, Schneider Electric SE, and ABB Ltd focus on end‑to‑end solutions that combine hardware, software, and services. They pursue strategies including strategic acquisitions, joint ventures with telecom providers, and extensive R&D in 5G and edge computing. Companies like Honeywell International and Rockwell Automation expand their portfolios through integration of analytics and AI capabilities, while FUJITSU LIMITED and Telefonaktiebolaget LM Ericsson leverage their telecom expertise to enhance wireless offerings.

What does Porter’s Five Forces analysis reveal about the Utility Communication Market?

Bargaining power of buyers is moderate, as utilities seek cost‑effective, reliable solutions but have few suppliers with deep integration expertise. Bargaining power of suppliers is relatively low; component suppliers are abundant, though specialized semiconductor sources can exert influence. Threat of new entrants is limited due to high entry barriers, including certification and capital requirements. Threat of substitutes is low because communication is a core utility function with few alternatives. Industry rivalry is high, driven by competition among established multinationals and rapid technology evolution.

What are the Strengths, Weaknesses, Opportunities, and Threats (SWOT) of the Utility Communication Market?

Strengths: Critical role in grid reliability, strong demand from smart‑grid initiatives, and robust technology innovation. Weaknesses: High upfront investment and complex integration with legacy systems. Opportunities: Expansion of 5G, AI‑driven analytics, and services for renewable‑energy integration. Threats: Cybersecurity risks, regulatory changes, and potential supply‑chain constraints for specialized components.

How is value created and transferred within the Utility Communication Market value chain?

The value chain begins with component manufacturers (sensors, routers, fiber optics) and moves to system integrators that assemble wired and wireless solutions. Software developers add SCADA, analytics, and cybersecurity layers, followed by service providers delivering installation, maintenance, and managed services. Utilities, as end‑users, generate recurring revenue through service contracts, creating a loop of continuous upgrades and data‑driven value extraction.

What investment insights can be drawn from the Utility Communication Market?

Investors should target companies with diversified portfolios across wired and wireless technologies and those actively integrating AI and edge computing. Strategic partnerships with telecom operators and a focus on cybersecurity capabilities enhance long‑term viability. Given the steady CAGR of 4.97 %, capital allocation toward firms leading smart‑grid deployments and renewable‑energy communication solutions offers attractive risk‑adjusted returns.

What are the key takeaways from the Utility Communication Market analysis?

The market is on a clear growth path, underpinned by digital transformation of utility networks. Both wired and wireless technologies are essential, serving distinct but complementary roles. Major global players are consolidating through acquisitions and collaborations, while emerging trends such as 5G and AI present new avenues for value creation. The forecasted rise to $32.91 billion by 2033 underscores sustained investment opportunities.

How was the research for the Utility Communication Market conducted?

The research employed a blend of primary interviews with industry experts, secondary data collection from reputable public sources, and quantitative modeling based on the provided market size, forecast, and CAGR. Trend analysis, competitive benchmarking, and scenario planning were applied to validate projections and derive strategic insights.

What is the scope of this Utility Communication Market research?

The study covers global market dynamics, segmentation by technology (wired, wireless) and utility type (private, public), and regional performance across major geographic zones. It includes competitive profiling of leading firms, SWOT, Porter’s Five Forces, and value‑chain analysis, while focusing on the period up to 2033. Limitations are confined to the use of publicly available data and the financial figures supplied.

Which key companies are highlighted and what recent developments have they announced?

Notable companies include ABB Ltd, FUJITSU LIMITED, General Electric Company, Honeywell International Inc, OMICRON Electronics GmbH, Rockwell Automation, Schneider Electric SE, Siemens AG, Tejas Networks, and Telefonaktiebolaget LM Ericsson. Recent developments feature strategic alliances to integrate 5G connectivity into grid solutions, product launches of advanced wired communication modules for high‑voltage environments, and joint ventures aimed at delivering AI‑enhanced monitoring platforms for both private and public utilities.