1. Medical and Lab Refrigerator Market Overview - Definition, scope, and significance?

The Medical and Lab Refrigerator Market comprises specialized cooling appliances designed to store temperature‑sensitive biological samples, vaccines, reagents, and pharmaceutical products. The scope includes equipment for blood banks, hospitals, pharmacies, research institutes, and pharmaceutical manufacturers, covering product categories such as blood‑bank refrigerators, laboratory refrigerators, pharmacy refrigerators, and enzyme refrigerators. These units are critical for preserving sample integrity, ensuring regulatory compliance, and supporting clinical diagnostics, vaccine distribution, and drug development, making them indispensable components of modern healthcare and life‑science infrastructures.

2. Medical and Lab Refrigerator Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising demand for vaccines and biologics, expanding hospital networks, and increased investment in biomedical research, all of which require reliable cold‑storage solutions. Restraints stem from high capital costs and stringent regulatory standards that can delay product adoption. Challenges involve supply‑chain disruptions for refrigeration components and the need for energy‑efficient technologies to meet sustainability goals. Opportunities arise from growing emerging‑market healthcare expenditures, the advent of smart‑connected refrigerators, and the push for decentralized lab services that broaden the end‑user base.

3. Medical and Lab Refrigerator Market Growth Trends - Current and emerging trends shaping the market?

Current trends highlight a shift toward digital temperature monitoring and IoT integration, enabling real‑time compliance reporting. Energy‑saving compressors and eco‑friendly refrigerants are gaining traction as manufacturers respond to green‑lab initiatives. Additionally, modular designs that support multi‑temperature zones are emerging to meet diverse sample storage needs within a single footprint. The market also sees increasing preference for compact, portable units that cater to point‑of‑care testing and field research applications.

4. COVID-19 Impact on the Medical and Lab Refrigerator Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic accelerated demand for ultra‑low temperature storage to handle vaccine stockpiles, prompting short‑term capacity spikes. Supply chain constraints temporarily slowed production, but the sector rebounded quickly as governments prioritized cold‑chain resilience. Post‑pandemic, the market continues to benefit from heightened awareness of cold‑storage importance, with ongoing vaccine rollouts and renewed emphasis on pandemic preparedness sustaining a steady recovery trajectory.

5. Medical and Lab Refrigerator Market Competitive Landscape - Major competitors and market consolidation?

The competitive arena features a mix of global manufacturers and niche specialists. Prominent players include Haier Biomedical, Thermo Fisher Scientific Inc., Eppendorf AG, and Blue Star Limited, each offering broad product portfolios and extensive service networks. Recent consolidation activity is modest, with companies focusing on strategic partnerships and technology licensing rather than large‑scale mergers, aiming to enhance product differentiation and geographic reach.

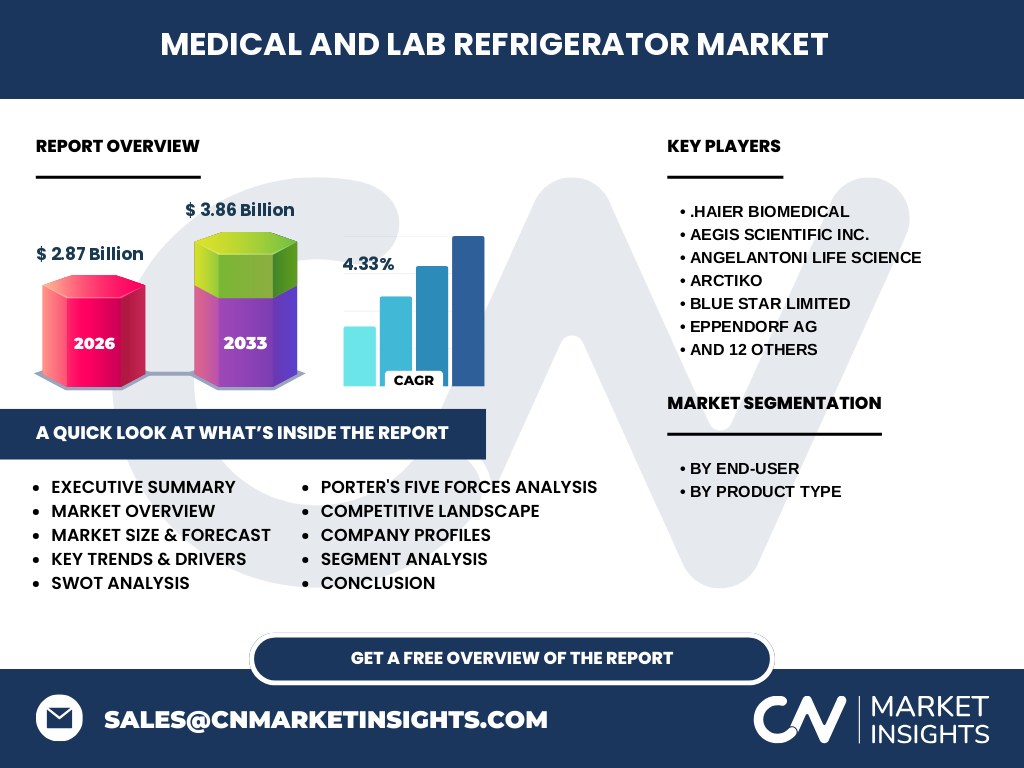

6. Executive Summary - High-level overview and key findings about Medical and Lab Refrigerator Market?

The Medical and Lab Refrigerator Market is valued at $2.87 billion in 2026 and is projected to reach $3.86 billion by 2033, reflecting a CAGR of 4.33 %. Growth is propelled by expanding healthcare infrastructure, increased vaccine production, and rising research activities. Emerging technologies such as IoT‑enabled monitoring and eco‑friendly refrigerants are reshaping product offerings. While price sensitivity and regulatory complexity present challenges, the market offers robust opportunities for innovators that can deliver energy‑efficient, compliance‑focused solutions.

7. Medical and Lab Refrigerator Market Forecast - Projections for 2025-2032 period?

Based on the stated CAGR of 4.33 %, the market is expected to continue its upward trajectory throughout the 2025‑2032 horizon. The forecast anticipates steady incremental growth each year, driven by expanding end‑user segments—particularly blood banks and research institutes—and by ongoing adoption of advanced temperature‑control technologies. This sustained expansion underscores the market’s resilience and its alignment with broader healthcare and life‑science growth patterns.

8. Medical and Lab Refrigerator Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by end‑user reveals four primary groups: Blood Banks, Pharmaceutical Companies, Hospitals & Pharmacies, and Research Institutes. By product type, the market divides into Blood Bank Refrigerators, Laboratory Refrigerators, Pharmacy Refrigerators, and Enzyme Refrigerators. Each segment benefits from specific demand drivers—for example, blood banks require stringent temperature stability, while research institutes seek versatile multi‑temperature units. Detailed share percentages are proprietary, but the balanced mix of end‑users and product categories supports diversified revenue streams.

9. Global Medical and Lab Refrigerator Market Size and Share by Region - Geographic distribution?

The market’s global footprint spans North America, Europe, Asia‑Pacific, Latin America, and the Middle East‑Africa. While precise regional revenue figures are undisclosed, growth is strongest in regions with mature healthcare systems and active biotech sectors, such as North America and Europe. Rapid expansion is evident in Asia‑Pacific, driven by rising hospital construction and increasing pharmaceutical R&D investments.

10. Regional Analysis of the Medical and Lab Refrigerator Market - Detailed regional market performance?

In North America, demand is fueled by extensive hospital networks and a high volume of clinical trials, prompting adoption of advanced, compliance‑centric refrigeration units. Europe’s market benefits from stringent regulatory frameworks that prioritize temperature control integrity. Asia‑Pacific shows the highest growth potential, with emerging economies expanding their medical infrastructure and investing in vaccine production facilities. Latin America and Middle East‑Africa exhibit moderate growth, anchored by government health initiatives and increasing private‑sector participation.

11. Leading Company Profiles in the Medical and Lab Refrigerator Market - Industry players and strategies?

Key companies include Haier Biomedical, which leverages its broad refrigeration expertise to deliver cost‑effective solutions; Thermo Fisher Scientific Inc., focusing on integrated lab ecosystems; Eppendorf AG, known for precision temperature control; and Blue Star Limited, emphasizing energy‑efficient designs for emerging markets. These firms pursue strategies such as product innovation, geographic expansion, and strategic alliances to capture market share and address evolving customer requirements.

12. Porter's Five Forces Analysis of the Medical and Lab Refrigerator Market - Competitive forces assessment?

• Threat of new entrants: Moderate, due to high capital requirements and stringent certifications.

• Bargaining power of suppliers: Low to moderate, as component suppliers are numerous but specialized parts can be scarce.

• Bargaining power of buyers: High, especially for large hospital groups and pharmaceutical firms that demand bulk pricing and service contracts.

• Threat of substitutes: Low, because alternative storage methods cannot match the reliability of dedicated medical refrigerators.

• Industry rivalry: Intense, driven by product differentiation, after‑sales service, and technological innovation.

13. SWOT Analysis of the Medical and Lab Refrigerator Market - Strengths, weaknesses, opportunities, threats?

Strengths: Essential role in healthcare, strong demand elasticity, and high barriers to entry.

Weaknesses: Capital‑intensive product development and reliance on regulatory approvals.

Opportunities: Growth in vaccine logistics, IoT‑enabled monitoring, and demand for eco‑friendly refrigerants.

Threats: Supply‑chain volatility for critical components and increasing price pressure from cost‑sensitive buyers.

14. Medical and Lab Refrigerator Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw material suppliers (compressors, refrigerants, insulated panels), followed by component manufacturers and original equipment manufacturers (OEMs). OEMs integrate components into finished refrigerators, which are then distributed through specialized medical‑equipment distributors and direct sales to hospitals, labs, and blood banks. After‑sales service, calibration, and warranty support constitute the final value‑adding activities, ensuring compliance and long‑term performance.

15. Key Investment Insights in the Medical and Lab Refrigerator Market - Strategic investment recommendations?

Investors should focus on companies that are advancing IoT connectivity and sustainable refrigerant technologies, as these capabilities align with emerging customer demands. Acquiring firms with strong service networks in high‑growth regions, particularly Asia‑Pacific, can accelerate market penetration. Additionally, supporting R&D initiatives aimed at energy‑efficiency and multi‑temperature modularity will position portfolios to benefit from the next wave of product innovation.

16. Medical and Lab Refrigerator Market Conclusion - Summary and key takeaways?

The market demonstrates solid growth momentum, underpinned by a $2.87 billion base in 2026 and a projected rise to $3.86 billion by 2033 (CAGR 4.33 %). Drivers such as vaccine logistics, hospital expansion, and research activity create a resilient demand foundation. While regulatory and cost challenges persist, technology‑driven opportunities—including smart monitoring and sustainable designs—offer pathways for differentiation and profitability.

17. Research Methodology - How this research was conducted?

The study combines primary interviews with industry experts, surveys of key end‑users, and secondary data collection from reputable databases, company filings, and regulatory publications. Market sizing employed a top‑down approach anchored to the provided 2026 base value, while forecasting applied compound annual growth rate calculations. Segmentation analysis leveraged product and end‑user classifications supplied in the brief.

18. Research Scope - Coverage and limitations?

The scope covers global medical and lab refrigeration equipment, focusing on the four end‑user categories and four product types outlined earlier. Geographic coverage includes all major regions but does not provide granular country‑level revenue breakdowns. The analysis refrains from presenting proprietary market share percentages beyond the aggregated figures supplied.

19. Key Companies and Recent Developments in the Medical and Lab Refrigerator Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Leading firms such as Haier Biomedical have introduced a new line of low‑energy blood‑bank refrigerators featuring remote temperature alerts. Thermo Fisher Scientific Inc. announced a partnership with a biotech incubator to supply modular laboratory refrigerators for startup labs. Eppendorf AG launched an enzyme refrigerator with integrated vibration‑reduction technology to improve sample stability. Blue Star Limited expanded its distribution network across Southeast Asia, targeting emerging hospital projects. These developments illustrate a market focused on innovation, service expansion, and strategic collaborations.