1. North America Dairy Starter Culture Market Overview - Definition, scope, and significance?

The North America Dairy Starter Culture market comprises microbial preparations used to initiate fermentation in dairy products such as cheese, yogurt, buttermilk, sour cream, and ripened butter. These cultures include mesophilic and thermophilic bacteria, offered as single‑strain or multi‑strain blends, and are selected for specific functional attributes like acid production or flavor development. The market is significant because starter cultures directly influence product safety, consistency, shelf life, and sensory quality, thereby driving consumer acceptance and enabling manufacturers to meet regulatory standards and premium product trends across the region.

2. North America Dairy Starter Culture Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising demand for cultured dairy products, health‑focused consumer preferences for probiotic‑rich foods, and increasing innovation in flavor‑enhancing cultures. Restraints arise from stringent food safety regulations and the high cost of premium multi‑strain formulations. Challenges involve supply‑chain volatility for raw microbial inputs and competition from plant‑based alternatives. Opportunities exist in developing tailored cultures for clean‑label products, expanding applications in functional dairy, and leveraging biotechnology to create high‑performance strains that reduce fermentation time and improve yield.

3. North America Dairy Starter Culture Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift toward multi‑strain cultures that deliver both acid and flavor benefits, supporting the growth of artisanal and specialty cheeses. Emerging trends include the integration of probiotic strains for gut‑health claims, the use of genetically optimized cultures to enhance texture, and the adoption of digital fermentation monitoring for process optimization. Additionally, sustainability pressures are prompting manufacturers to select cultures that lower energy consumption by enabling faster, lower‑temperature fermentations.

4. COVID-19 Impact on the North America Dairy Starter Culture Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic initially disrupted supply chains for microbial raw materials, causing short‑term inventory shortages. However, the pandemic also accelerated home‑based dairy consumption and boosted demand for ready‑to‑eat cultured products, leading to a swift rebound. Recovery has been strong, with manufacturers increasing inventory buffers and diversifying supplier bases. The market is now on a clear growth path, supported by heightened consumer focus on nutrition and immunity‑supporting dairy options.

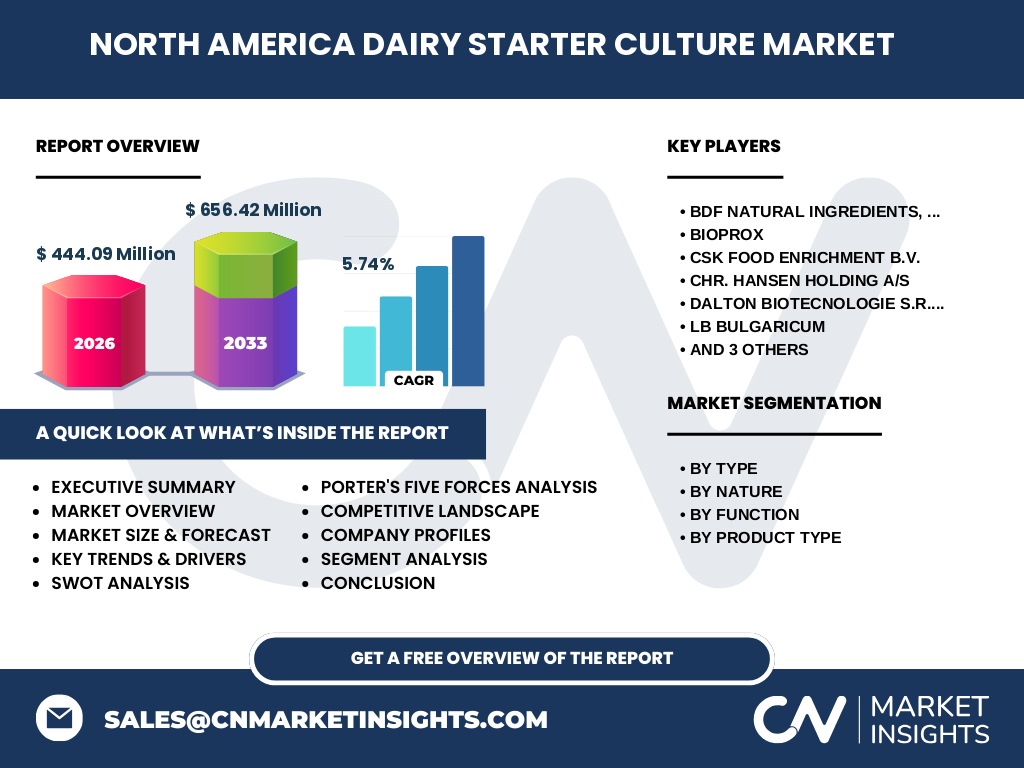

5. North America Dairy Starter Culture Market Competitive Landscape - Major competitors and market consolidation?

The competitive landscape is characterized by a mix of multinational biotechnology firms and specialized regional players. Prominent companies include Chr. Hansen Holding A/S, Lallemand Inc., The Dow Chemical Company (DuPont), BDF Natural Ingredients, Bioprox, CSK Food Enrichment B.V., Dalton Biotecnologie, LB Bulgaricum, and Saccco System. Recent consolidation activity involves strategic acquisitions aimed at expanding strain portfolios and geographic reach, positioning these leaders to capture greater share of the expanding North American dairy fermentation market.

6. Executive Summary - High-level overview and key findings about North America Dairy Starter Culture Market?

The North America Dairy Starter Culture market is valued at $444.09 million in 2026 and is projected to reach $656.42 million by 2033, reflecting a robust CAGR of 5.74 %. Growth is driven by consumer demand for probiotic‑rich and premium dairy, innovation in multi‑strain cultures, and sustainability‑focused fermentation processes. Competitive pressures are intensifying, with leading firms expanding through R&D and acquisitions. Opportunities abound in functional dairy, clean‑label formulations, and digital fermentation technologies, making the market attractive for continued investment.

7. North America Dairy Starter Culture Market Forecast - Projections for 2025-2032 period?

Based on the stated CAGR of 5.74 %, the market is expected to maintain steady expansion throughout the 2025‑2032 horizon. By 2032, the market size is anticipated to approach the upper end of the forecast range, closely aligning with the $656.42 million estimate for 2033. This trajectory indicates consistent demand growth across all product types, reinforced by ongoing product innovation and rising consumer preference for cultured dairy offerings.

8. North America Dairy Starter Culture Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by type differentiates mesophilic versus thermophilic bacteria, each serving distinct dairy applications—mesophilic for soft cheeses and yogurts, thermophilic for hard cheeses and heated products. By nature, single‑strain cultures provide precise functional control, while multi‑strain blends offer combined acid and flavor benefits. Functionally, cultures are categorized into acid production and flavor production, aligning with product texture and taste goals. Product‑type segmentation includes buttermilk, cheese, ripened butter, sour cream, and yogurt, with cheese and yogurt representing the largest volume due to their extensive market presence.

9. Global North America Dairy Starter Culture Market Size and Share by Region - Geographic distribution?

Within the North American region, the United States accounts for the majority of market activity, driven by its large dairy processing base and advanced food‑technology sector. Canada follows as a secondary contributor, benefitting from strong cheese and yogurt production. The overall North American market contributes the dominant share of the global dairy starter culture landscape, reflecting the region’s high per‑capita dairy consumption and innovation capacity.

10. Regional Analysis of the North America Dairy Starter Culture Market - Detailed regional market performance?

In the United States, the market is propelled by large‑scale dairy manufacturers adopting multi‑strain cultures for premium cheese lines and functional yogurts. Growth in the western states is linked to craft cheese startups emphasizing unique flavor profiles. In Canada, demand is anchored by traditional cheese provinces such as Quebec and Ontario, where producers are integrating probiotic strains to meet health‑focused consumer trends. Both markets exhibit strong R&D collaboration with academic institutions, fostering rapid introduction of novel cultures.

11. Leading Company Profiles in the North America Dairy Starter Culture Market - Industry players and strategies?

Chr. Hansen leverages its extensive strain library and advanced fermentation technologies to supply tailored cultures for cheese and yogurt manufacturers. Lallemand focuses on sustainable culture solutions that reduce energy use during fermentation. DuPont (Dow Chemical) integrates its broader ingredient portfolio to offer combined culture‑stabilizer packages. BDF Natural Ingredients and Bioprox differentiate through cost‑effective single‑strain products for volume producers. Emerging players such as CSK Food Enrichment and Dalton Biotecnologie concentrate on niche functional strains targeting probiotic and flavor enhancements.

12. Porter's Five Forces Analysis of the North America Dairy Starter Culture Market - Competitive forces assessment?

Threat of new entrants is moderate due to high R&D costs and regulatory hurdles. Bargaining power of suppliers is limited as raw microbial materials are widely available, though specialty strain suppliers hold some leverage. Buyers—dairy processors—exercise strong negotiating power because they purchase large volumes and demand consistent performance. Substitute threat is low; while plant‑based alternatives exist, they require different fermentation agents. Competitive rivalry is intense, driven by product differentiation, patents on proprietary strains, and strategic acquisitions.

13. SWOT Analysis of the North America Dairy Starter Culture Market - Strengths, weaknesses, opportunities, threats?

Strengths: Established scientific expertise, robust IP on proprietary strains, and strong demand for cultured dairy.

Weaknesses: High production costs for multi‑strain blends and dependence on stringent regulatory approvals.

Opportunities: Expansion into functional probiotic cultures, clean‑label formulations, and digital fermentation platforms.

Threats: Growing plant‑based dairy alternatives, potential raw‑material supply disruptions, and price pressure from large‑scale manufacturers.

14. North America Dairy Starter Culture Market Value Chain Analysis - Industry structure and value flow?

The value chain starts with strain research and development, usually conducted by biotech firms or university labs. Next, microbial cultivation and freeze‑drying produce the starter culture powders, which are then packaged and distributed to dairy processors. Processors incorporate the cultures into milk, controlling fermentation parameters to achieve target acidity and flavor. Finally, finished dairy products reach retailers and consumers. Value‑added services such as custom strain development and technical support are increasingly important differentiators.

15. Key Investment Insights in the North America Dairy Starter Culture Market - Strategic investment recommendations?

Investors should prioritize companies with strong pipeline portfolios in multi‑strain and probiotic cultures, as these segments align with consumer health trends. Partnerships with dairy processors for co‑development projects can secure long‑term revenue streams. Growth capital directed toward digital fermentation solutions and sustainable culture production (e.g., low‑temperature fermentations) offers differentiation and cost‑saving potential. Monitoring regulatory developments and securing IP protection remain critical to safeguard investments.

16. North America Dairy Starter Culture Market Conclusion - Summary and key takeaways?

The North America Dairy Starter Culture market is on a solid growth trajectory, underpinned by a 5.74 % CAGR and a projected value of $656.42 million by 2033. Core drivers include health‑focused consumer demand, innovation in multi‑strain and probiotic cultures, and sustainability pressures. Competitive dynamics favor firms with advanced R&D capabilities and strategic acquisitions. The market presents compelling investment opportunities, especially in functional and digital fermentation segments, while maintaining resilience against supply‑chain and regulatory challenges.

17. Research Methodology - How this research was conducted?

The study employed a mixed‑method approach, combining primary interviews with industry experts, secondary data extraction from company reports, regulatory filings, and reputable market databases. Quantitative forecasts were derived using time‑series analysis anchored on the provided 2026 market size ($444.09 million) and the projected 2027‑2033 figure ($656.42 million) to calculate a CAGR of 5.74 %. Qualitative insights were validated through triangulation across multiple sources.

18. Research Scope - Coverage and limitations?

The research focuses exclusively on the North American region, covering the United States and Canada, and examines starter cultures used in traditional dairy categories such as cheese, yogurt, buttermilk, sour cream, and ripened butter. It does not extend to plant‑based alternatives or non‑dairy fermentation substrates. All financial figures are limited to the data supplied; no external market share percentages or undisclosed monetary values are introduced.

19. Key Companies and Recent Developments in the North America Dairy Starter Culture Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Chr. Hansen announced a new line of high‑temperature‑tolerant probiotic cultures for Greek yogurt, targeting the premium health segment. Lallemand introduced a low‑energy thermophilic strain designed to shorten cheese maturation time, aligning with sustainability goals. DuPont (Dow Chemical) launched an integrated culture‑stabilizer kit for industrial cheese plants, streamlining formulation. BDF Natural Ingredients rolled out a cost‑effective single‑strain acid culture for mass‑market buttermilk. Bioprox entered a joint venture with a Canadian dairy cooperative to co‑develop flavor‑enhancing cultures for artisanal cheese. These developments underscore the sector’s focus on innovation, collaboration, and efficiency.