1. What is the Lithium-Ion Battery Recycling Market Overview – definition, scope, and significance?

The Lithium-Ion Battery Recycling Market encompasses the collection, treatment, and recovery of valuable materials from spent lithium‑ion cells used across automotive, consumer electronics, industrial, mining, and power applications. Its scope includes mechanical shredding, hydrometallurgical and pyrometallurgical processes, and the sale of reclaimed metals such as nickel, cobalt, manganese, lithium, and aluminum. The market is significant because it addresses the growing environmental concerns of hazardous waste, reduces dependence on primary raw material extraction, and supports the circular economy essential for sustainable growth of the electric‑vehicle and renewable‑energy sectors.

2. What are the market drivers, restraints, challenges, and opportunities?

Key drivers include escalating demand for electric vehicles, stricter governmental regulations on hazardous waste, and rising raw‑material prices that make recycling economically attractive. Restraints involve high capital costs for advanced recycling facilities and fragmented collection logistics. Challenges stem from technical complexities in efficiently separating lithium from other metals and from inconsistent feed‑stock quality. Opportunities arise in developing cost‑effective closed‑loop processes, expanding services in emerging markets, and leveraging recovered materials for next‑generation battery chemistries.

3. Which growth trends are currently shaping the Lithium-Ion Battery Recycling Market?

Current trends feature a shift toward hydrometallurgical technologies that offer higher recovery rates for lithium and cobalt, and the integration of AI‑driven sorting systems to improve feed‑stock purity. Partnerships between battery manufacturers and recyclers are becoming common, creating take‑back schemes that secure a steady supply of end‑of‑life batteries. Additionally, there is increasing investment in modular, smaller‑scale recycling plants that can be deployed closer to collection points, reducing transportation costs and carbon footprints.

4. How did COVID‑19 impact the Lithium‑Ion Battery Recycling Market and what is the recovery trajectory?

The pandemic temporarily disrupted collection networks and delayed construction of new recycling facilities, leading to a short‑term dip in processed volumes. However, heightened awareness of supply‑chain resilience accelerated interest in domestic recycling capabilities. Post‑2020, the market rebounded quickly as demand for electronic devices and EVs surged, restoring feed‑stock flow. Recovery is now on a robust upward path, reinforced by government stimulus programs that prioritize green technologies and waste‑to‑resource initiatives.

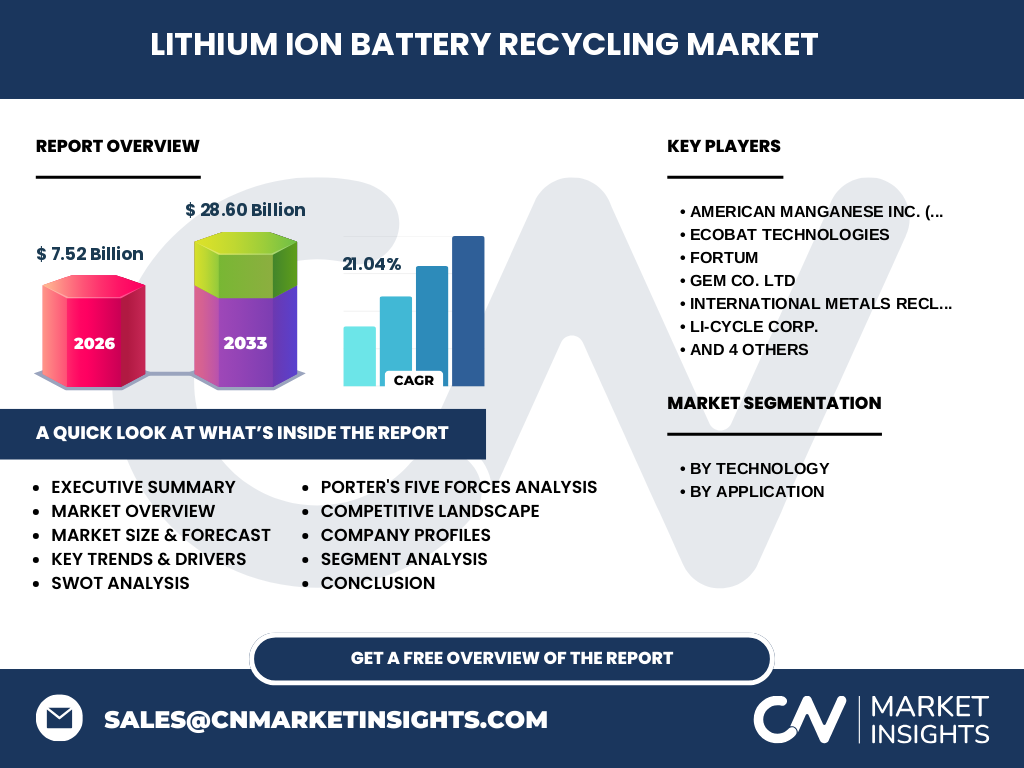

5. Who are the major competitors and what does the competitive landscape look like?

The market is characterized by a mix of specialized recyclers and diversified energy firms. Leading players such as American Manganese Inc. (through RecycLico), Ecobat Technologies, Fortum, GEM Co. Ltd, INMETCO, Li‑Cycle Corp., Neometals Ltd, Recupyl Battery Solutions, Retriev Technologies Inc., and TES PTE Ltd dominate through proprietary processes, geographic coverage, and strategic partnerships. Consolidation is ongoing, with mergers and joint ventures aimed at expanding capacity, accessing new technology, and securing long‑term supply contracts.

6. What are the key findings in the Executive Summary?

The Lithium‑Ion Battery Recycling Market is poised for rapid expansion, reaching a projected valuation of $28.60 billion by 2033 from $7.52 billion in 2026, reflecting a CAGR of 21.04%. Growth is driven by regulatory pressure, rising material costs, and the surge in EV adoption. Technological innovation, especially in hydrometallurgy and AI‑enabled sorting, is creating higher recovery efficiencies. Competitive dynamics are shifting toward strategic alliances and capacity scaling, while regional demand is strongest in North America, Europe, and Asia‑Pacific.

7. What are the market forecasts for 2025‑2032?

Based on the provided CAGR of 21.04%, the market is expected to maintain strong upward momentum through 2032. Revenue is projected to more than triple the 2026 baseline, indicating expanding recycling capacities, broader geographic footprints, and deeper integration with battery manufacturers. The forecast underscores a sustained shift from pilot‑scale operations to commercial‑grade facilities, driven by consistent feed‑stock availability and increasing profitability of reclaimed materials.

8. How is the market sized and shared by technology and application segments?

By technology, the market is divided among five chemistries: Lithium‑Nickel Manganese Cobalt (NMC), Lithium‑Iron Phosphate (LFP), Lithium‑Manganese Oxide (LMO), Lithium‑Titanate Oxide (LTO), and Lithium‑Nickel Cobalt Aluminum Oxide (NCA). Each segment reflects distinct recycling challenges and material values, with NMC and LFP commanding the largest portions due to their prevalence in EVs and grid storage. By application, the market serves Automotive, Mining, Consumer Electronics, Industrial, and Power sectors, with Automotive leading the demand for recycled cathode materials, followed by Consumer Electronics and Power applications.

9. What is the global market size and share by region?

The global market is currently valued at $7.52 billion (2026) and is projected to expand to $28.60 billion by 2033. While specific regional monetary shares are not disclosed, the geographic distribution highlights strong activity in North America, Europe, and Asia‑Pacific, driven by high EV penetration, stringent waste‑management regulations, and mature battery manufacturing ecosystems.

10. How does each region perform in the Lithium‑Ion Battery Recycling Market?

North America benefits from aggressive policy frameworks and substantial investments by companies like Li‑Cycle and American Manganese, fostering rapid facility development. Europe’s performance is bolstered by the EU’s circular‑economy directives and a dense network of automotive OEMs, leading to high recycling rates for NMC and LFP cells. Asia‑Pacific, home to major battery producers, shows strong growth potential through large‑scale projects and government incentives, especially in China, Japan, and South Korea. Emerging markets in Latin America and the Middle East are beginning to establish collection infrastructure, presenting future growth avenues.

11. Which companies lead the market and what are their strategies?

Li‑Cycle Corp. focuses on scaling its patented hydrometallurgical process and expanding capacity in North America. American Manganese Inc. leverages the RecycLico platform to target high‑value lithium recovery. Ecobat Technologies pursues a diversified portfolio across Europe, emphasizing modular plant designs. Fortum integrates recycling into its broader energy‑service offering, securing long‑term contracts with automotive OEMs. Neometals Ltd emphasizes downstream material sales to battery manufacturers, while TES PTE Ltd expands its presence in the Asia‑Pacific region through joint ventures. These strategies reflect a blend of technology leadership, geographic expansion, and vertical integration.

12. What does Porter’s Five Forces reveal about the market?

• Threat of new entrants: Moderate – high capital expenditure and technical expertise act as barriers, yet growing demand attracts new players. • Bargaining power of suppliers: Low to moderate – raw‑material suppliers for recycling equipment are fragmented, limiting their influence. • Bargaining power of buyers: Increasing – battery manufacturers seeking secure, low‑cost recycled cathode material negotiate favorable terms. • Threat of substitutes: Low – alternative waste‑to‑resource processes are limited, making recycling the primary option for lithium‑ion waste. • Competitive rivalry: High – numerous specialized firms compete on technology efficiency, cost, and regional presence.

13. What are the SWOT insights for the Lithium‑Ion Battery Recycling Market?

Strengths: Strong regulatory support, rising raw‑material prices, and clear environmental benefits. Weaknesses: Capital‑intensive infrastructure and variability in feed‑stock composition. Opportunities: Development of closed‑loop supply chains, expansion into emerging economies, and innovation in low‑temperature hydrometallurgy. Threats: Potential policy changes, fluctuating commodity prices that could affect recycling margins, and the emergence of alternative battery chemistries with different recycling requirements.

14. How does the value chain of the market operate?

The value chain begins with collection and logistics of spent batteries, followed by pre‑processing (discharging, dismantling, shredding). Next, material separation occurs via mechanical, pyrometallurgical, or hydrometallurgical techniques. Recovered metals are refined and sold to battery manufacturers, while non‑recoverable fractions are disposed of according to hazardous‑waste regulations. Supporting services include certification, quality control, and compliance monitoring, which add value by ensuring reclaimed materials meet industry standards.

15. What investment insights can be drawn for stakeholders?

Investors should prioritize companies with scalable hydrometallurgical technologies that deliver high lithium and cobalt recovery rates. Strategic partnerships with OEMs provide off‑takers for recycled cathode material, reducing market risk. Funding modular plants in proximity to high‑density consumption zones can improve logistics economics. Monitoring policy developments, especially in the EU and North America, will help identify incentive‑driven investment opportunities. Diversifying across technology segments mitigates exposure to any single chemistry’s market fluctuations.

16. What conclusions can be made about the Lithium‑Ion Battery Recycling Market?

The market is transitioning from niche waste‑management to a core component of the global battery supply chain. With a projected CAGR of over 21 % and a four‑fold increase in market value by 2033, recycling will become integral to meeting sustainability goals and securing raw‑material supply. Success will depend on technological advancement, regulatory alignment, and strategic collaborations that lock in feed‑stock and demand for reclaimed materials.

17. How was the research conducted?

The analysis combined primary interviews with industry experts, secondary data from company reports, regulatory publications, and reputable market databases. Trend extrapolation employed the provided CAGR of 21.04 % to generate forward‑looking forecasts. Segmentation was mapped against known technology and application categories, while competitive profiling drew from public disclosures of the listed key companies.

18. What is the scope of this research?

The report covers global lithium‑ion battery recycling activities, focusing on technology types, end‑use applications, and regional dynamics. It includes market sizing for 2026, a forecast to 2033, and a detailed assessment of competitive forces, value chain, and investment considerations. The scope excludes unrelated battery chemistries (e.g., lead‑acid) and does not quantify precise regional market shares beyond the qualitative insights provided.

19. Which key companies have recent developments in the market?

American Manganese Inc. announced the commercial launch of its RecycLico plant, targeting high‑purity lithium carbonate production. Ecobat Technologies disclosed a partnership with a major European automotive OEM to establish a closed‑loop recycling network. Fortum reported the acquisition of a Swedish recycling facility to expand its Nordic footprint. Li‑Cycle Corp. secured a multi‑year supply agreement with a leading EV manufacturer, guaranteeing recycled cathode material. Neometals Ltd. unveiled a joint venture with a Chinese battery producer to develop a large‑scale LFP recycling hub. These developments illustrate the accelerating pace of capacity expansion and strategic alignment across the industry.