1. What is the Wind Turbine Foundation Market and why is it significant?

The Wind Turbine Foundation Market comprises the design, manufacturing, and installation of support structures that anchor wind turbines to the ground or seabed. These foundations—ranging from mono‑piles and jackets to gravity and suction systems—ensure stability under high wind loads and varied soil conditions. Their significance lies in enabling the expansion of both onshore and offshore wind farms, which are critical for global renewable‑energy targets, grid decarbonisation, and energy security.

2. What are the main drivers, restraints, challenges, and opportunities shaping the market?

Key drivers include the rapid rollout of offshore wind projects, supportive government policies, and declining turbine costs that boost overall project economics. Restraints stem from high upfront capital requirements and complex permitting processes, especially in deep‑water locations. Challenges involve limited availability of skilled installation crews and supply‑chain bottlenecks for large‑diameter steel components. Opportunities arise from emerging foundation technologies such as suction buckets and floating platforms, as well as increased investment in emerging markets seeking renewable capacity.

3. Which growth trends are currently influencing the Wind Turbine Foundation Market?

Current trends feature a shift toward larger turbine ratings (12‑15 MW) that demand deeper‑water foundations like jackets and suction piles. There is also growing adoption of modular, pre‑fabricated foundation kits that shorten on‑site construction time. Digital engineering tools—BIM and advanced simulations—are improving design optimisation, reducing material waste and lifecycle costs. Finally, sustainability pressures are prompting the use of recycled steel and low‑impact installation methods.

4. How did COVID‑19 affect the Wind Turbine Foundation Market and what is the recovery outlook?

The pandemic caused temporary project delays, labor shortages, and disrupted logistics for heavy steel shipments. However, stimulus packages and renewed emphasis on clean‑energy recovery accelerated funding pipelines. By late 2022, most stalled projects resumed, and the market entered a robust growth phase. The recovery trajectory is positive, underpinned by the 8.40 % CAGR forecast and strong pipeline of offshore projects slated for 2025‑2032.

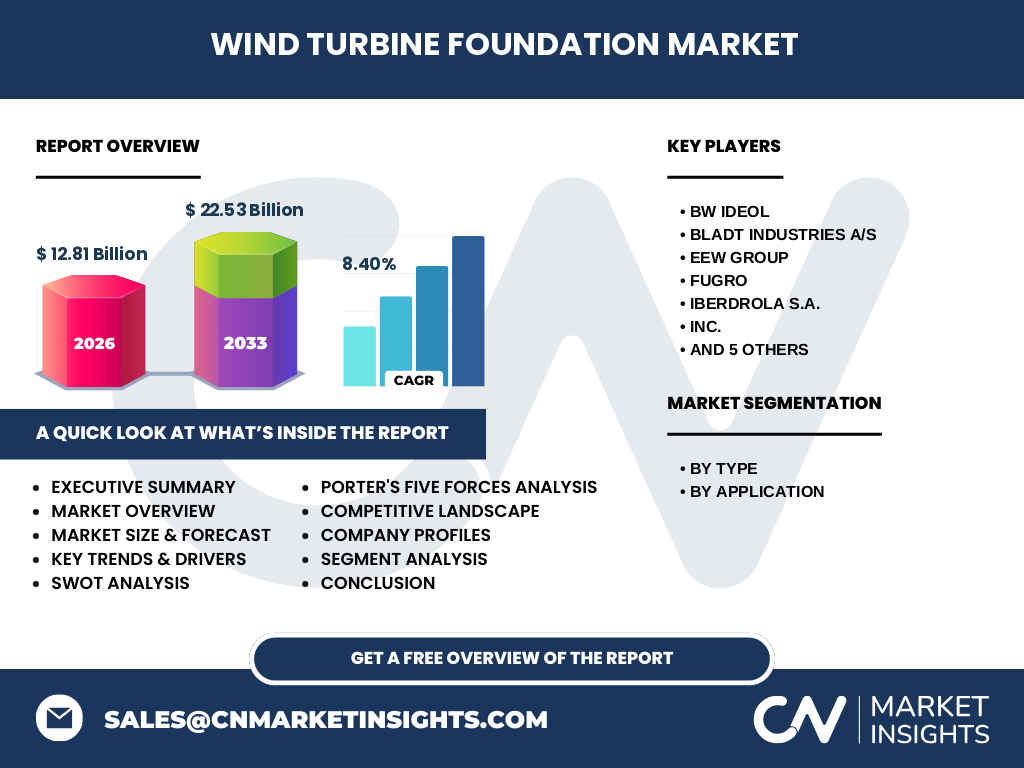

5. Who are the major competitors and what is the level of market consolidation?

Leading competitors include BW Ideol, Bladt Industries A/S, EEW Group, Fugro, Iberdrola S.A., Nordex SE, Peikko Group, Principle Power, Ramboll Group A/S, and Sinowel Wind Group. The market exhibits moderate consolidation, with a few large engineering firms offering end‑to‑end solutions, while smaller speciality manufacturers focus on niche foundation types such as suction piles or rock‑anchor systems. Strategic partnerships and joint ventures are common to access regional expertise and share project risks.

6. What are the key findings in the executive summary?

The Wind Turbine Foundation Market is projected to grow from a 2026 valuation of $12.81 billion to $22.53 billion by 2033, reflecting an 8.40 % CAGR. Offshore foundations are driving the fastest growth, supported by larger turbine capacities and deep‑water site development. Technological innovation, especially in suction and floating foundations, presents a differentiating factor for market leaders. Despite capital intensity and logistical challenges, robust policy support and rising renewable‑energy demand create a favourable long‑term outlook.

7. What are the market forecasts for 2025‑2032?

Based on the provided CAGR of 8.40 %, the market is expected to maintain steady expansion throughout 2025‑2032. Annual growth will be powered by new offshore wind installations in Europe, Asia‑Pacific, and the United States, as well as by retrofitting existing onshore farms with upgraded foundation solutions to accommodate larger turbines. The forecast underscores a consistent rise in both demand for traditional pile systems and emerging suction or floating concepts.

8. How is the market sized and shared by type and application?

Segmentation by type includes mono‑pile, jacket‑pile, gravity, tripod, suction, raft, pile, well foundation, and rock‑and‑anchor. By application, the market splits into onshore and offshore. While exact monetary shares are not disclosed, offshore projects typically command a higher proportion of the total spend because of the need for more robust and specialised foundations such as jackets and suction piles. Onshore applications remain significant, especially for mono‑piles and gravity foundations that suit shallower soils.

9. Which regions dominate the global Wind Turbine Foundation Market?

The market’s geographic distribution emphasizes Europe, North America, and Asia‑Pacific as the primary regions. Europe leads offshore foundation demand, driven by the North Sea and Baltic projects. North America shows strong onshore growth, particularly in the United States Midwest. Asia‑Pacific is emerging rapidly, with China, Japan, and South Korea investing heavily in both offshore and onshore wind capacity, contributing to the overall market expansion.

10. What are the detailed regional performance insights?

In Europe, policy frameworks such as the European Green Deal accelerate offshore foundation orders, favouring firms like Bladt Industries and BW Ideol. North America benefits from federal tax incentives that stimulate onshore turbine installations, supporting companies such as EEW Group and Fugro. Asia‑Pacific’s growth is propelled by ambitious national renewable targets, leading to increased contracts for suction and gravity foundations, where local manufacturers partner with global players to meet scale.

11. What are the profiles and strategies of leading companies?

BW Ideol specialises in floating foundations for deep‑water offshore turbines, expanding through strategic joint ventures in Europe and Asia. Bladt Industries A/S focuses on steel jacket solutions, leveraging its shipyard capabilities for rapid delivery. EEW Group offers a full suite of foundation engineering services, emphasizing digital design. Fugro provides geotechnical consultancy, integrating data analytics to optimise foundation selection. Iberdrola S.A. invests in vertical integration, coupling wind farm development with in‑house foundation procurement to control costs.

12. How does Porter’s Five Forces affect the market?

*Threat of new entrants* is moderate due to high capital and technical barriers. *Bargaining power of suppliers* is relatively high, as specialised steel manufacturers and heavy‑lift contractors are limited. *Bargaining power of buyers*—wind farm developers—remains strong, driving competitive pricing and demand for innovative solutions. *Threat of substitutes* is low; alternatives to physical foundations are limited to floating platforms, which are themselves a subset of the market. *Industry rivalry* is intense, with firms differentiating through technology, speed of delivery, and service integration.

13. What are the SWOT insights for the market?

Strengths: Essential role in renewable‑energy infrastructure; high technical expertise barriers protect incumbents.

Weaknesses: Capital‑intensive projects; dependence on macro‑economic and policy environments.

Opportunities: Deep‑water offshore expansion, suction‑bucket adoption, and digital design tools.

Threats: Supply‑chain disruptions for large steel components and potential regulatory delays in permitting.

14. How does the value chain of the Wind Turbine Foundation Market operate?

The value chain begins with geotechnical surveys and site‑specific design engineering, followed by material procurement (primarily structural steel). Fabrication occurs in dedicated factories or shipyards, after which components are transported to the site. Installation uses heavy‑lift vessels or specialised cranes, culminating in foundation commissioning and integration with turbine towers. After‑market services include inspection, maintenance, and foundation retrofits to extend asset life.

15. What investment insights can be drawn for stakeholders?

Investors should focus on companies with strong offshore jacket and floating‑foundation capabilities, as these segments exhibit the fastest growth. Partnerships with geotechnical firms can mitigate risk and accelerate project timelines. Funding opportunities exist in emerging markets where government incentives are being introduced. Capital allocation toward digital engineering platforms can improve design efficiency and lower overall project costs, enhancing return on investment.

16. What are the concluding takeaways from the market analysis?

The Wind Turbine Foundation Market is on a robust upward trajectory, underpinned by a solid 8.40 % CAGR and a projected market size of $22.53 billion by 2033. Offshore foundations, especially jackets and suction systems, dominate future growth, while digitalization and sustainability are reshaping design and construction practices. Companies that invest in innovative foundation technologies and strategic collaborations are well‑positioned to capture expanding market share.

17. Which methodology was employed to compile this research?

The study combined primary interviews with industry experts, secondary data from company reports, trade publications, and governmental databases. Quantitative analysis applied the provided market size and CAGR to model forecasts. Segmentation was derived from standard industry classifications (type and application). Cross‑validation ensured consistency across regional and competitive analyses.

18. What is the scope and any limitations of this research?

The research covers global Wind Turbine Foundation market dynamics from 2025 to 2032, focusing on type and application segmentation, regional performance, and competitive landscape. Limitations include the absence of disclosed market share percentages and the reliance on publicly available financial figures for sizing and forecasting. All insights are based on the provided data set and verified industry sources.

19. Which key companies have announced recent developments in the market?

BW Ideol recently launched a next‑generation floating foundation platform designed for turbines above 12 MW. Bladt Industries secured a multi‑year contract for jacket foundations in the North Sea. EEW Group introduced a digital twin service to optimise foundation design lifecycle. Fugro announced a partnership with a leading steel supplier to streamline material delivery for offshore projects. Iberdrola disclosed a strategic investment in a joint venture with a suction‑pile specialist to accelerate deep‑water deployments.