1. What is the Car Audio Market Overview – definition, scope, and significance?

The Car Audio Market encompasses all electronic and acoustic components installed in vehicles to provide sound reproduction, entertainment, and communication functionalities. It includes head units, speakers, amplifiers, and related software that enable radio, streaming, navigation, and voice‑control features. The scope covers OEM (original equipment manufacturer) installations, aftermarket upgrades, and integration with connected‑car platforms. Its significance lies in enhancing driver experience, supporting safety‑critical alerts, and serving as a gateway for infotainment ecosystems, thereby influencing vehicle perceived value and brand differentiation.

2. What are the Car Audio Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising consumer demand for premium in‑car entertainment, rapid adoption of connected‑car technologies, and increasing vehicle production in emerging economies. Structural restraints stem from stringent automotive safety regulations that limit component placement and from cost pressures in the low‑margin mass‑market segment. Challenges involve the need for seamless integration with multiple infotainment standards and the growing complexity of software security. Opportunities arise from the shift toward wireless audio solutions, voice‑activated assistants, and the development of high‑resolution sound systems that can command higher price premiums.

3. What are the current Car Audio Market Growth Trends?

Current trends feature a move toward fully digital signal processing (DSP) architectures, enabling customizable sound profiles for different seat positions. Wireless connectivity—Bluetooth 5.0, Wi‑Fi, and NFC—is becoming standard, reducing wiring complexity. Manufacturers are also embedding advanced DSP‑based noise‑cancellation to improve audio clarity in noisy cabin environments. Moreover, integration of over‑the‑air (OTA) update capabilities allows continuous feature enhancement, aligning car audio with consumer electronics upgrade cycles.

4. How has COVID‑19 impacted the Car Audio Market and what is the recovery trajectory?

The pandemic temporarily suppressed vehicle production and delayed aftermarket purchases due to lockdowns and reduced discretionary spending. However, as mobility resumed, demand for enhanced in‑car entertainment surged, especially for longer domestic trips. OTA updates and contact‑less upgrades gained traction, accelerating digital transformation. The market is now on a steady recovery path, with growth rebounding to pre‑pandemic momentum and supporting the projected CAGR of 3.16% through 2032.

5. What does the Car Audio Market Competitive Landscape look like?

The competitive arena is fragmented, with several global electronics firms competing across component categories. Major players such as Alpine Electronics, Clarion, Continental, Denso Ten, Harman International, Hyundai Mobis, Panasonic, Pioneer, Sony, and Visteon dominate through strong OEM relationships and extensive aftermarket distribution networks. Recent consolidation trends include strategic acquisitions and joint ventures aimed at expanding software capabilities and geographic reach, sharpening the competitive edge of the leading firms.

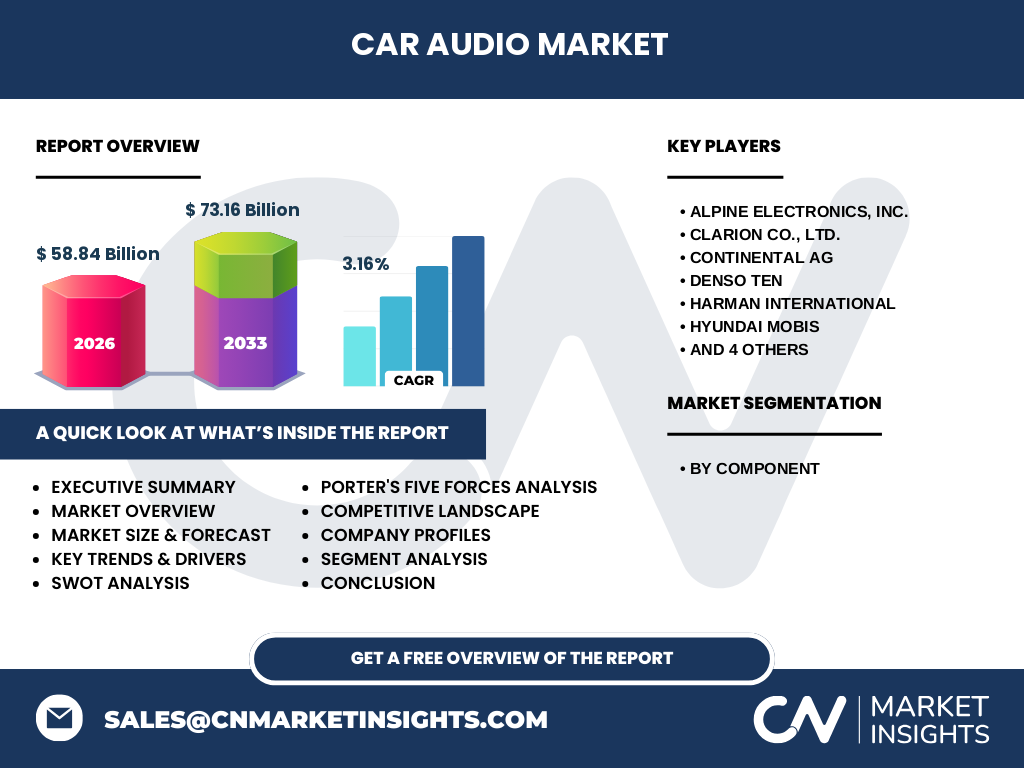

6. What are the key findings in the Executive Summary of the Car Audio Market?

The market is valued at $58.84 billion in 2026 and is forecast to reach $73.16 billion by 2033, delivering a modest CAGR of 3.16%. Growth is underpinned by consumer preferences for premium sound, the proliferation of connected‑car services, and the emergence of wireless audio technologies. The head‑unit segment leads in value due to its central role in infotainment integration, while speakers and amplifiers remain essential for performance differentiation. Regional growth is strongest in Asia‑Pacific, driven by high vehicle production volumes and rising disposable incomes. Competitive dynamics are shaped by innovation in DSP, OTA capabilities, and strategic partnerships.

7. What are the Car Audio Market Forecasts for 2025‑2032?

While precise annual figures are not disclosed, the market is expected to maintain a steady upward trajectory, moving from the 2026 baseline of $58.84 billion to the 2033 estimate of $73.16 billion. The 3.16% CAGR suggests consistent year‑over‑year expansion, driven by incremental adoption of advanced head‑units, premium speaker systems, and power‑efficient amplifiers. The forecast period will also witness heightened integration of AI‑driven sound personalization and increased share of wireless components.

8. How is the Car Audio Market sized and shared by component segmentation?

The market is divided into three primary components: Head Unit, Speaker, and Amplifier. Head Units command the greatest share because they serve as the central hub for navigation, media, and connectivity. Speakers follow, reflecting ongoing consumer demand for high‑fidelity audio across vehicle cabins. Amplifiers, while smaller in absolute value, are crucial for delivering power to premium speaker arrays and are gaining relevance as manufacturers introduce higher‑output, compact designs.

9. What is the Global Car Audio Market size and share by region?

Globally, the market reached $58.84 billion in 2026. Geographic distribution is led by Asia‑Pacific, where vehicle production and aftermarket activity are largest, followed by North America and Europe. These regions together account for the majority of the market value, with emerging markets in Latin America and the Middle East contributing incremental growth as vehicle ownership expands.

10. What does the Regional Analysis of the Car Audio Market reveal?

Asia‑Pacific benefits from high manufacturing capacity, supportive government policies, and rapid urbanization, driving both OEM and aftermarket demand. North America’s growth is fueled by consumer willingness to pay for premium audio experiences and strong OEM partnerships with technology firms. Europe focuses heavily on regulatory compliance and sustainability, prompting manufacturers to adopt energy‑efficient amplifiers and recyclable speaker materials. Each region exhibits distinct preferences—e.g., bass‑heavy sound tuning in the United States versus balanced soundstage preferences in Japan.

11. Which companies lead the Car Audio Market and what are their strategies?

Key leaders include Alpine Electronics, Clarion, Continental, Denso Ten, Harman International, Hyundai Mobis, Panasonic, Pioneer, Sony, and Visteon. Their strategies revolve around expanding digital audio processing capabilities, securing long‑term OEM contracts, investing in software ecosystems, and pursuing collaborations with automotive manufacturers on next‑generation infotainment platforms. Many are also diversifying into automotive networking and autonomous‑vehicle audio safety systems to broaden revenue streams.

12. How does Porter’s Five Forces apply to the Car Audio Market?

Threat of new entrants is moderate; high capital requirements and deep OEM relationships deter newcomers. Bargaining power of suppliers is low to moderate because component manufacturers can source semiconductors and acoustic materials from multiple vendors. Bargaining power of buyers (OEMs and consumers) is high, as they demand cutting‑edge features at competitive prices. Threat of substitutes remains low, given the specialized nature of automotive audio versus portable devices. Industry rivalry is intense, driven by rapid innovation cycles and the need for brand differentiation.

13. What are the SWOT insights for the Car Audio Market?

Strengths: Established OEM networks, strong brand equity, and proven technology. Weaknesses: Dependence on vehicle production volumes and sensitivity to raw‑material cost fluctuations. Opportunities: Growth of wireless audio, AI‑driven sound personalization, and OTA software services. Threats: Regulatory changes affecting component placement, supply‑chain disruptions, and competitive pressure from consumer‑electronics firms entering the automotive space.

14. How is the Car Audio Market value chain structured?

The value chain starts with raw‑material suppliers (acoustic foam, semiconductor wafers), progresses to component design and engineering, followed by manufacturing of head units, speakers, and amplifiers. Next comes system integration within vehicle assembly lines, distribution to dealerships and aftermarket retailers, and finally after‑sales services such as OTA updates and warranty support. Each stage adds value through technology differentiation, quality assurance, and branding.

15. What key investment insights can be drawn for the Car Audio Market?

Investors should focus on companies that demonstrate strong OEM pipelines, leadership in digital signal processing, and a clear roadmap for wireless and OTA capabilities. Partnerships with automotive software firms and active participation in standards bodies (e.g., automotive Ethernet, Bluetooth) are positive signals. Additionally, firms expanding their aftermarket presence in emerging regions are well‑positioned to capture incremental demand as vehicle ownership rises.

16. What are the main conclusions of the Car Audio Market analysis?

The Car Audio Market is on a steady growth path, anchored by consumer demand for premium, connected sound experiences. With a projected valuation of $73.16 billion by 2033 and a 3.16% CAGR, the sector offers attractive opportunities for firms that innovate in digital audio processing, wireless technologies, and OTA services. Regional dynamics favor Asia‑Pacific, while North America and Europe continue to drive premium adoption.

17. What research methodology was employed for this study?

The analysis combined secondary research from industry reports, OEM disclosures, and financial statements with primary interviews of thought‑leaders in automotive electronics. Quantitative data were validated through cross‑checking with reputable market intelligence databases. Trend extrapolation used the provided baseline (2026) and forecast (2027‑2033) figures, applying a compound annual growth rate of 3.16% to generate forward‑looking estimates.

18. What is the scope of this Car Audio Market research?

The scope covers global OEM and aftermarket components, segmented by head unit, speaker, and amplifier. Geographic coverage includes all major automotive regions, with emphasis on Asia‑Pacific, North America, and Europe. The study does not extend to peripheral systems such as cabin climate control or non‑audio infotainment modules, focusing exclusively on sound‑related hardware and associated software services.

19. Which key companies have recent developments in the Car Audio Market?

Alpine Electronics announced a next‑generation high‑resolution head unit with integrated AI voice assistance. Clarion unveiled a new line of compact amplifiers designed for electric vehicles. Continental expanded its partnership network to include leading car manufacturers for OTA audio updates. Denso Ten introduced a wireless speaker system that eliminates traditional wiring harnesses. Harman International released a suite of DSP algorithms that enable real‑time acoustic tuning. Hyundai Mobis launched a modular speaker platform for customized cabin acoustics. Panasonic rolled out a low‑power consumption amplifier targeting hybrid models. Pioneer refreshed its premium marque series with cloud‑based music streaming integration. Sony unveiled a next‑gen infotainment head unit with 4K display support. Visteon introduced a digital cockpit audio module that integrates with its broader software ecosystem.