1. Europe Menstrual Cups Market Overview - Definition, scope, and significance?

The Europe Menstrual Cups Market comprises manufacturers, distributors, and retailers of reusable or disposable menstrual cups used by women during their menstrual cycle. The market scope includes all product types (small, medium, large), materials (medical‑grade silicone, natural rubber, thermoplastic elastomer), and distribution channels (online stores, pharmacies, retail stores) across European countries. Its significance stems from a growing preference for sustainable feminine hygiene solutions, heightened environmental awareness, and increasing disposable income, positioning menstrual cups as a strategic alternative to conventional sanitary products.

2. Europe Menstrual Cups Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include heightened environmental concerns prompting a shift from single‑use pads and tampons, supportive regulatory frameworks for medical‑grade silicone products, and strong advocacy by women's health NGOs. Opportunities arise from product innovation (e.g., thermoplastic elastomer blends for enhanced comfort) and expanding e‑commerce penetration. Restraints involve cultural taboos around menstrual health, limited awareness in certain regions, and higher upfront cost compared with disposables. Challenges include supply‑chain disruptions for raw materials and the need for clear usage education to mitigate leakage concerns.

3. Europe Menstrual Cups Market Growth Trends - Current and emerging trends shaping the market?

Current trends highlight a rapid increase in online sales, driven by convenience and detailed product information available on e‑commerce platforms. Emerging trends include the launch of size‑specific designs to improve fit, the introduction of natural‑rubber cups targeting eco‑conscious consumers, and collaborations with healthcare professionals to endorse clinical safety. Additionally, brands are exploring subscription models to encourage repeat purchases and sustain user engagement.

4. COVID-19 Impact on the Europe Menstrual Cups Market - Pandemic effects and recovery trajectory?

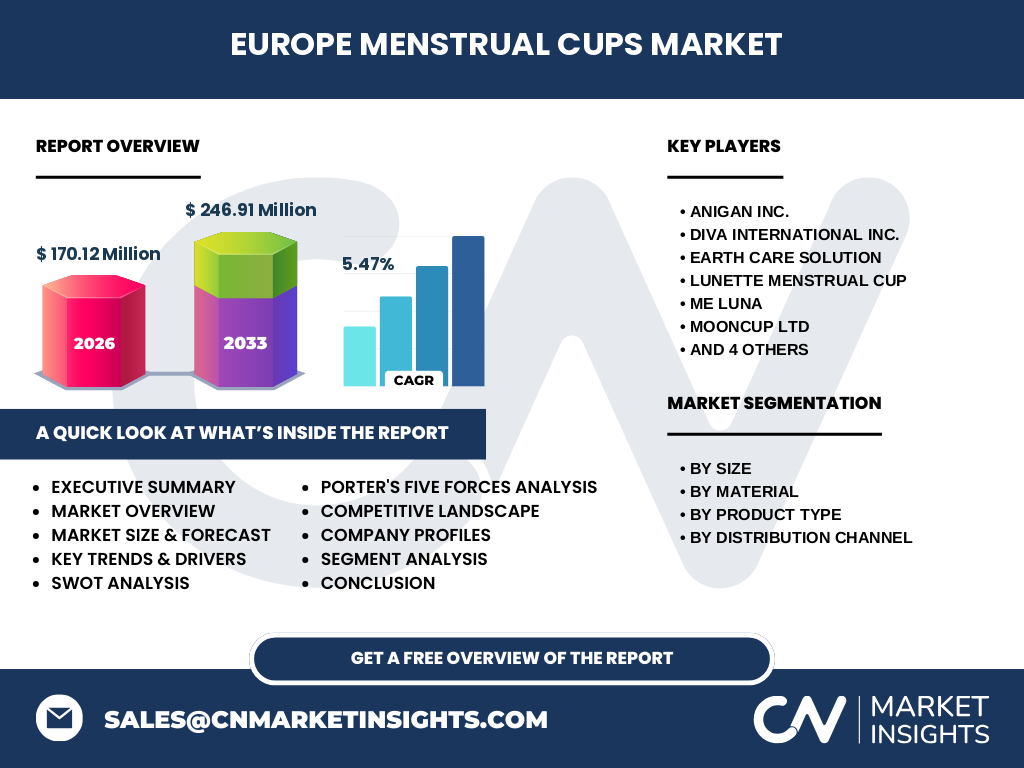

The COVID‑19 pandemic initially disrupted supply chains for raw materials, causing a short‑term dip in production volumes. However, lockdowns accelerated digital adoption, resulting in a surge of online orders for menstrual cups as consumers sought contactless purchasing options. Post‑pandemic, the market has rebounded strongly, with recovery reflected in the projected CAGR of 5.47% and a forecasted market size of €246.91 million by 2033, indicating robust long‑term growth.

5. Europe Menstrual Cups Market Competitive Landscape - Major competitors and market consolidation?

The competitive landscape is fragmented, featuring both specialist manufacturers and large consumer‑goods conglomerates. Key players include Anigan Inc., Diva International Inc., Earth Care Solution, Lunette Menstrual Cup, Me Luna, Mooncup Ltd, Procter & Gamble, Silky Cup, The Keeper Inc., and YUUKI COMPANY S.R.O. Recent activity shows strategic partnerships and product line extensions rather than significant M&A, suggesting a market focused on differentiation through material innovation and channel expansion.

6. Executive Summary - High-level overview and key findings about Europe Menstrual Cups Market?

The Europe Menstrual Cups Market is valued at €170.12 million in 2026 and is projected to reach €246.91 million by 2033, growing at a CAGR of 5.47%. Growth is propelled by sustainability trends, digital distribution, and product innovation across size and material categories. While cultural barriers and higher upfront costs remain restraints, expanding e‑commerce, subscription services, and clinical endorsements present clear opportunities. The market remains competitive with a diverse set of manufacturers focusing on niche differentiation.

7. Europe Menstrual Cups Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 5.47%, the market is expected to maintain steady growth throughout the 2025‑2032 horizon. Starting from the 2026 baseline of €170.12 million, the market will progress toward the 2033 forecast of €246.91 million, reflecting continued consumer adoption, broader retail availability, and sustained innovation in cup design and materials.

8. Europe Menstrual Cups Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by size (small, medium, large) reflects diverse anatomical needs, with medium likely commanding the largest share due to average fit. Material segmentation shows medical‑grade silicone as the premium standard, while natural rubber and thermoplastic elastomer capture environmentally focused niches. Product‑type segmentation highlights reusable cups dominating the market, with disposable options serving a secondary, convenience‑driven segment. Distribution channels are split among online stores (fastest‑growing), pharmacies (trusted health outlets), and retail stores (mass‑market presence).

9. Global Europe Menstrual Cups Market Size and Share by Region - Geographic distribution?

Within Europe, market concentration is strongest in Western European economies (Germany, France, United Kingdom, Netherlands) where disposable income and eco‑conscious consumer behavior are high. Northern Europe (Scandinavia) also shows robust uptake due to strong sustainability policies. Southern and Eastern European nations are in earlier adoption phases, offering future growth potential as awareness campaigns expand.

10. Regional Analysis of the Europe Menstrual Cups Market - Detailed regional market performance?

Western Europe leads in both volume and value, driven by mature retail networks and high e‑commerce penetration. Scandinavia demonstrates the highest per‑capita adoption, aided by government‑backed gender‑equality programs. Central Europe (Poland, Czech Republic, Hungary) exhibits moderate growth, with pharmacies serving as primary channels. The Mediterranean region shows gradual acceptance, with retail stores introducing dedicated shelf space for menstrual cups.

11. Leading Company Profiles in the Europe Menstrual Cups Market - Industry players and strategies?

Procter & Gamble leverages its extensive distribution network to introduce premium silicone cups under a trusted brand umbrella. Mooncup Ltd focuses on medical‑grade silicone and collaborates with health professionals for endorsements. Anigan Inc. differentiates through natural‑rubber formulations targeting the zero‑waste segment. Diva International Inc. expands its online footprint with subscription services, while Silky Cup emphasizes design aesthetics and size variety. Each company balances material innovation with channel diversification to capture distinct consumer segments.

12. Porter's Five Forces Analysis of the Europe Menstrual Cups Market - Competitive forces assessment?

Threat of new entrants: Moderate. Low capital intensity but high regulatory standards for medical‑grade materials create entry barriers. Bargaining power of suppliers: Moderate, as silicone and specialized elastomers have limited supplier pools. Bargaining power of buyers: Growing, driven by increased access to product information online. Threat of substitutes: Low to moderate; while pads and tampons remain alternatives, sustainability concerns reduce their appeal. Industry rivalry: High, with many firms competing on material quality, size options, and distribution channels.

13. SWOT Analysis of the Europe Menstrual Cups Market - Strengths, weaknesses, opportunities, threats?

Strengths: Sustainable product profile, long‑term cost savings for users, and increasing clinical validation. Weaknesses: Higher upfront price, need for proper usage education, cultural stigmas in certain markets. Opportunities: Expansion into underserved Eastern European markets, development of biodegradable materials, and subscription‑based models. Threats: Potential regulatory changes, raw‑material price volatility, and competition from emerging eco‑friendly disposable products.

14. Europe Menstrual Cups Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw‑material sourcing (medical‑grade silicone, natural rubber, TPE), followed by R&D for design and testing. Manufacturing involves precise molding processes, then quality assurance and certification. Distribution channels include direct‑to‑consumer e‑commerce platforms, pharmacy wholesaling, and retail logistics. Marketing leverages digital influencers, health‑care professional endorsements, and sustainability messaging. Post‑sale services include user education, customer support, and product warranty programs.

15. Key Investment Insights in the Europe Menstrual Cups Market - Strategic investment recommendations?

Investors should prioritize companies with strong e‑commerce infrastructure and diversified material portfolios, as these mitigate supply‑chain risk and capture digitally savvy consumers. Strategic acquisitions of niche natural‑rubber producers can accelerate entry into the zero‑waste segment. Funding for R&D focused on biodegradable elastomers offers a differentiated growth path. Finally, partnerships with health‑care providers can reinforce product credibility and drive premium pricing.

16. Europe Menstrual Cups Market Conclusion - Summary and key takeaways?

The Europe Menstrual Cups Market is on a clear growth trajectory, moving from €170.12 million in 2026 to an estimated €246.91 million by 2033. Sustainability, digital channels, and material innovation are the primary catalysts. While cultural and price barriers persist, the market’s fragmented yet dynamic competitive environment offers ample opportunity for investors and manufacturers to capture value through differentiation, regional expansion, and strategic collaborations.

17. Research Methodology - How this research was conducted?

The study combined primary interviews with industry experts, secondary data collection from company reports, trade publications, and regulatory filings, and quantitative modeling using the provided market size, forecast, and CAGR figures. Segmentation analysis leveraged product‑type, size, material, and channel data, while regional assessments were based on publicly available market penetration indicators across European economies.

18. Research Scope - Coverage and limitations?

The scope covers the European market for menstrual cups, detailing product segmentation, distribution channels, and major competitive players. Geographic focus is limited to Europe, with no extrapolation to global markets beyond the provided figures. Financial estimates are confined to the given market size (2026) and forecast (2027‑2033) with a CAGR of 5.47%; no additional revenue breakdowns were generated.

19. Key Companies and Recent Developments in the Europe Menstrual Cups Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent developments include Procter & Gamble’s launch of a new silicone cup line integrated with a QR‑code education platform, Mooncup Ltd.’s partnership with a leading Scandinavian retailer to expand shelf visibility, Anigan Inc.’s rollout of a biodegradable natural‑rubber cup in select EU markets, and Silky Cup’s introduction of a size‑customization kit sold through its online store. Diva International Inc. announced a subscription service offering quarterly kit deliveries, while YUUKI COMPANY S.R.O. entered a joint venture with a medical‑device distributor to streamline pharmacy placement across Central Europe.