What is the Push to Talk Market overview – definition, scope, and significance?

The Push to Talk (PTT) market encompasses technologies that enable instant voice communication at the press of a button, replicating the functionality of traditional two‑way radios over modern networks. Its scope includes hardware devices, software platforms, and related services delivered via land mobile radio (LMR) and cellular networks to a wide range of end‑users such as government, defense, transportation, logistics, travel, hospitality, energy, utilities, construction, and manufacturing. The significance lies in its ability to provide real‑time coordination, improve operational efficiency, and reduce communication costs for both large enterprises and SMEs.

What are the key drivers, restraints, challenges, and opportunities shaping the Push to Talk market?

Growth is driven by increasing demand for instant communication in mission‑critical sectors, the rollout of 5G enabling high‑quality cellular PTT, and cost‑effective convergence of voice and data services. Restraints include high initial hardware investment and regulatory hurdles in certain regions. Challenges stem from interoperability issues between legacy LMR systems and modern IP‑based solutions, as well as cybersecurity concerns. Opportunities arise from the expanding IoT ecosystem, integration of AI‑enhanced voice analytics, and the rising need for remote workforce coordination in post‑pandemic environments.

What are the current growth trends in the Push to Talk market?

Key trends include a shift from traditional analog LMR to digital and cellular‑based PTT solutions, accelerated adoption of software‑defined radio (SDR) platforms, and the bundling of PTT with unified communications‑as‑a‑service (UCaaS). Vendors are increasingly offering hybrid models that combine hardware, software, and managed services to meet diverse enterprise needs. Additionally, the proliferation of ruggedized smartphones and wearables is expanding the user base beyond conventional radio operators.

How has COVID‑19 impacted the Push to Talk market and what is the recovery trajectory?

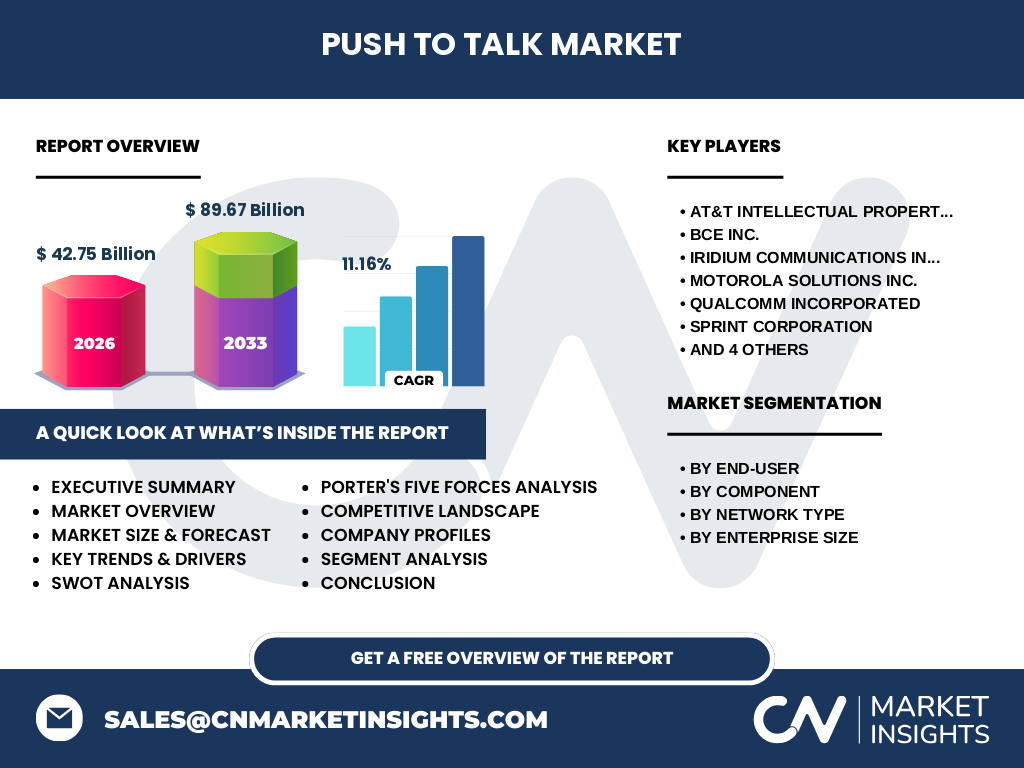

The pandemic highlighted the importance of reliable, instant communication for emergency responders and essential service providers, leading to a temporary surge in demand for robust PTT solutions. Remote work and social distancing accelerated the deployment of cloud‑based PTT services. Recovery is strong, with organizations continuing to invest in resilient communication infrastructures, supported by the market’s projected CAGR of 11.16% through 2032.

Who are the major competitors in the Push to Talk market and what is the state of market consolidation?

The competitive landscape features global telecom operators, network equipment manufacturers, and specialized communication firms. Leading players include AT&T Intellectual Property, BCE Inc., Iridium Communications Inc., Motorola Solutions Inc., Qualcomm Incorporated, Sprint Corporation, Tait Communications, Telstra Corporation Limited, Verizon Communications Inc., and Zebra Technologies Corporation. While the market remains fragmented, strategic partnerships and acquisitions are driving modest consolidation, especially around integrated hardware‑software service bundles.

What are the high‑level findings in the executive summary of the Push to Talk market?

The Push to Talk market is poised for rapid expansion, reaching a valuation of $89.67 billion by 2033 from $42.75 billion in 2026, driven by a robust 11.16% CAGR. Digital and cellular PTT are outpacing legacy LMR, with strong adoption in government, defense, transportation, and construction. Key growth levers include 5G rollout, hybrid service models, and AI‑enabled analytics. Competitive dynamics favor firms that can offer end‑to‑end solutions across hardware, software, and services.

What is the forecast for the Push to Talk market from 2025 to 2032?

Based on the provided data, the market is expected to more than double, climbing from $42.75 billion in 2026 to $89.67 billion by 2033. This translates to a sustained compound annual growth rate of 11.16% throughout the forecast horizon, reflecting strong demand across all end‑user segments and continued investment in next‑generation network infrastructure.

How is the Push to Talk market sized and shared by segmentation?

Segmentation reveals three primary dimensions. By end‑user, government and defense lead due to mission‑critical communication needs, followed by transportation, logistics, and construction. Component‑wise, hardware holds the largest share, supported by the rollout of rugged devices, while software and services are gaining traction as subscription models grow. Network type segmentation shows land mobile radio still dominant in legacy sectors, but cellular PTT is expanding rapidly, especially with 5G adoption. Enterprise size analysis indicates large enterprises dominate purchases, although SMEs are increasingly adopting cloud‑based PTT services.

What is the global Push to Talk market size and share by region?

The market displays a worldwide distribution, with North America and Europe contributing the largest shares due to early technology adoption and strong government contracts. Asia‑Pacific is emerging rapidly, driven by infrastructure projects and rising logistics activity. While precise regional monetary values are not disclosed, the overall growth trajectory reflects balanced expansion across all major territories.

What are the detailed regional performances in the Push to Talk market?

In North America, adoption is propelled by extensive public safety networks and advanced telecom infrastructure. Europe benefits from harmonized spectrum allocations and robust defense spending. Asia‑Pacific’s growth is fueled by large‑scale transportation and construction initiatives, alongside expanding mobile broadband coverage. Latin America and the Middle East & Africa show moderate growth, primarily in government and energy sectors, but present significant upside as network modernization progresses.

Which companies lead the Push to Talk market and what are their strategic approaches?

Motorola Solutions focuses on integrated hardware‑software platforms and strong service contracts with public safety agencies. Qualcomm drives PTT through chipset innovation and partnerships with cellular operators. Verizon and AT&T leverage their extensive network footprints to offer managed PTT services. Iridium provides satellite‑based PTT for remote locations, while Zebra Technologies targets industry‑specific solutions for logistics and manufacturing. These leaders combine R&D investment, strategic alliances, and diversified portfolios to capture market share.

How does Porter’s Five Forces analysis apply to the Push to Talk market?

Threat of new entrants is moderate; high capital requirements and regulatory barriers deter many newcomers. Bargaining power of suppliers is low to moderate, as component suppliers are abundant but specialized hardware can be limited. Bargaining power of buyers is increasing, especially for large enterprises seeking cost‑effective subscription models. Threat of substitutes remains low, given the unique real‑time voice capability of PTT compared to standard messaging apps. Industry rivalry is intense, with numerous global players competing on technology, coverage, and service integration.

What are the SWOT insights for the Push to Talk market?

Strengths: Immediate voice communication, proven reliability in mission‑critical environments, and growing integration with 5G. Weaknesses: Legacy system incompatibility and high upfront hardware costs. Opportunities: Expansion into IoT, AI‑driven analytics, and underserved emerging markets. Threats: Cybersecurity risks, regulatory changes, and potential market saturation in mature regions.

How is the value chain structured in the Push to Talk market?

The value chain begins with component manufacturers (RF modules, processors), proceeds to device assemblers (hardware), then software developers creating PTT platforms and middleware. Telecommunications operators provide network connectivity (LMR or cellular). Service providers deliver managed services, support, and integration. End‑users consume the solution, generating aftermarket revenue through maintenance, upgrades, and analytics services.

What key investment insights can be drawn for the Push to Talk market?

Investors should focus on companies that own end‑to‑end capabilities, especially those integrating hardware, software, and managed services. Growth capital is attractive in the cellular PTT segment, given 5G rollouts. Satellite‑based PTT providers present niche opportunities in remote and maritime sectors. Partnerships with large enterprises and government contracts provide stable, recurring revenue streams, making them prime targets for long‑term investment.

What conclusions can be drawn from the Push to Talk market analysis?

The Push to Talk market is on a steep growth curve, underpinned by digital transformation, 5G, and heightened demand for reliable, instant voice communication across critical industries. While legacy systems pose integration challenges, the shift toward hybrid and cloud‑based models offers substantial upside. Companies that innovate with AI, IoT, and unified communications are best positioned to capture future market share.

What research methodology was employed for this Push to Talk market study?

The study combines primary interviews with industry experts, surveys of end‑users, and secondary data collection from reputable sources such as company annual reports, regulatory filings, and market databases. Quantitative data were validated through triangulation, and qualitative insights were synthesized to develop forecasts and strategic recommendations.

What is the scope of the research and its coverage limitations?

The research covers global market size, segmentation by end‑user, component, network type, and enterprise size, as well as regional performance, competitive landscape, and forward‑looking forecasts up to 2033. Limitations include reliance on publicly disclosed financials and an inability to provide granular market share percentages beyond the aggregate figures supplied.

Who are the key companies and what recent developments have they announced in the Push to Talk market?

Motorola Solutions recently launched a next‑generation digital radio with integrated AI analytics. Qualcomm announced new 5G‑optimized chipsets for cellular PTT devices. Verizon expanded its cloud‑based PTT service to include advanced security features. Iridium introduced a satellite‑backed PTT solution for offshore energy platforms. Zebra Technologies unveiled a rugged handheld PTT device tailored for logistics and warehouse operations. These developments illustrate the industry’s focus on convergence, security, and vertical‑specific solutions.