1. Energy Recovery Ventilator Market Overview - Definition, scope, and significance?

The Energy Recovery Ventilator (ERV) market encompasses devices that exchange indoor and outdoor air while transferring heat and moisture, thereby improving indoor air quality and reducing HVAC energy consumption. The scope includes residential, commercial, and industrial applications, offered in wall‑mounted, ceiling‑mounted, and cabinet configurations, and utilizing plate heat exchangers, heat‑pipe, rotary, or run‑around coil technologies. ERVs are significant because they align with global energy‑efficiency mandates, support sustainable building standards, and contribute to lower operating costs and carbon footprints.

2. Energy Recovery Ventilator Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers are stringent green‑building codes, rising awareness of indoor air quality, and governmental incentives for energy‑saving retrofits. Restraints include high upfront costs and limited consumer knowledge in emerging economies. Challenges arise from competing ventilation solutions and the need for skilled installation. Opportunities stem from advances in smart‑connected ERVs, integration with IoT building management systems, and expanding refurbishment projects in mature markets, which can accelerate adoption despite price sensitivity.

3. Energy Recovery Ventilator Market Growth Trends - Current and emerging trends shaping the market?

Current trends highlight a shift toward high‑efficiency plate heat exchangers and the adoption of rotatory designs for compact spaces. Emerging trends include the incorporation of predictive analytics for demand‑controlled ventilation and the development of hybrid ERV‑HRV units that offer flexible moisture handling. Additionally, manufacturers are launching modular, cabinet‑type solutions that simplify retrofitting, while sustainability certifications such as LEED and WELL drive demand across both residential and commercial segments.

4. COVID-19 Impact on the Energy Recovery Ventilator Market - Pandemic effects and recovery trajectory?

The pandemic heightened focus on ventilation, leading to a temporary surge in ERV demand for healthcare and office settings as occupants sought healthier indoor environments. Supply‑chain disruptions delayed some projects, but the overall impact was positive for market sentiment. Recovery accelerated in 2022‑2023 as building owners invested in air‑quality upgrades, and the momentum continues, positioning the market for robust growth through 2032.

5. Energy Recovery Ventilator Market Competitive Landscape - Major competitors and market consolidation?

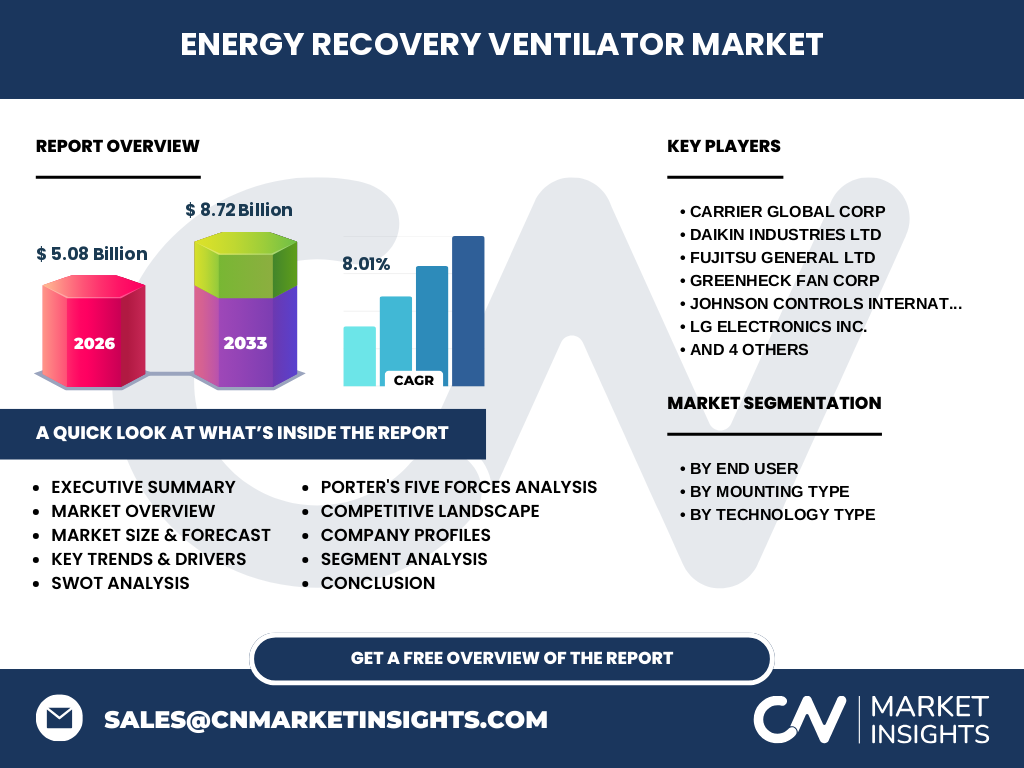

The competitive landscape features established players such as Carrier Global Corp, Daikin Industries Ltd, Fujitsu General Ltd, Greenheck Fan Corp, Johnson Controls International Plc, LG Electronics Inc., Mitsubishi Electric Corp., Munters Group AB, Nortek Air Solutions, LLC, and Panasonic Holdings Corp. Recent activity includes strategic acquisitions and joint ventures aimed at expanding product portfolios and geographic reach, indicating a moderate level of consolidation as firms seek scale and technology synergies.

6. Executive Summary - High-level overview and key findings about Energy Recovery Ventilator Market?

The ERV market is projected to reach USD 5.08 billion in 2026 and grow to USD 8.72 billion by 2033, reflecting a CAGR of 8.01%. Growth is driven by regulatory pressure, health‑centric design, and technological innovation. Residential and commercial‑industrial end users dominate, while plate heat exchangers hold the largest technology share. Geographic expansion, smart integration, and sustainability initiatives are the primary catalysts, positioning the market for sustained expansion.

7. Energy Recovery Ventilator Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 8.01%, the market is expected to maintain steady acceleration from the 2025 baseline, surpassing USD 6 billion by 2028 and approaching the 2032 target of roughly USD 8.5 billion. The forecast reflects continued adoption in retrofit projects, new constructions seeking energy compliance, and increasing demand for smart ventilation solutions across all major regions.

8. Energy Recovery Ventilator Market Size and Share by Segmentation - Breakdown by segment data?

By end‑user, the market splits between residential and commercial‑industrial applications, with commercial‑industrial typically commanding a larger share due to larger system volumes. Mounting type segmentation shows wall‑mounted units leading in residential retrofits, while ceiling‑mounted and cabinet configurations gain traction in commercial spaces. Technology segmentation indicates plate heat exchangers as the dominant type, followed by heat‑pipe, rotary, and run‑around coil technologies, each serving niche performance or space‑constraint requirements.

9. Global Energy Recovery Ventilator Market Size and Share by Region - Geographic distribution?

Although specific regional figures are not disclosed, the market’s global footprint encompasses North America, Europe, Asia‑Pacific, and the Rest of World. Developed regions such as North America and Europe contribute the highest proportion due to strict building codes and mature construction sectors. Rapid urbanization and growing awareness in Asia‑Pacific drive emerging market share, while Latin America and the Middle East present incremental growth opportunities.

10. Regional Analysis of the Energy Recovery Ventilator Market - Detailed regional market performance?

North America leads with early adoption of high‑efficiency HVAC systems and extensive retrofitting programs. Europe follows, propelled by the EU’s Energy Efficiency Directive and widespread green‑building certifications. Asia‑Pacific shows the fastest growth rate, fueled by massive residential construction, rising middle‑class demand, and increasing governmental focus on indoor air quality. Emerging regions exhibit lower penetration but are poised for future expansion as awareness spreads.

11. Leading Company Profiles in the Energy Recovery Ventilator Market - Industry players and strategies?

Carrier Global Corp leverages its HVAC legacy to deliver integrated ERV solutions and emphasizes smart controls. Daikin Industries focuses on energy‑saving technologies and expands through regional partnerships. Fujitsu General targets residential markets with compact wall‑mounted units. Greenheck Fan Corp differentiates with robust commercial‑grade products. Johnson Controls integrates ERVs into its broader building‑automation platform, while LG Electronics and Panasonic capitalize on consumer electronics expertise to create user‑friendly designs. Mitsubishi Electric, Munters Group, and Nortek Air Solutions pursue niche technologies and geographic diversification.

12. Porter's Five Forces Analysis of the Energy Recovery Ventilator Market - Competitive forces assessment?

Threat of new entrants is moderate due to high R&D costs and certification barriers. Bargaining power of suppliers remains low as key components like heat‑exchanger cores are commoditized. Bargaining power of buyers is growing, driven by cost sensitivity and demand for smart features. Threat of substitutes includes simple exhaust fans and HRVs, but ERVs’ combined heat‑and‑moisture recovery offers a unique value proposition. Industry rivalry is intense, with numerous global firms competing on technology, price, and service.

13. SWOT Analysis of the Energy Recovery Ventilator Market - Strengths, weaknesses, opportunities, threats?

Strengths: Energy efficiency, improved indoor air quality, alignment with regulatory trends. Weaknesses: High initial investment and limited awareness in some markets. Opportunities: Smart‑connected ERVs, expanding retrofits, and integration with renewable energy systems. Threats: Competitive pressure from lower‑cost ventilation alternatives and potential supply‑chain volatility for specialty components.

14. Energy Recovery Ventilator Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw material suppliers (metals, polymers, heat‑exchange media), proceeds to component manufacturers (fans, controllers, exchangers), then to system integrators that assemble wall‑mounted, ceiling‑mounted, or cabinet units. Distributors and OEM partners handle channel sales, while end‑users (residential homeowners, commercial facilities) drive demand. After‑sales service, maintenance contracts, and data‑analytics platforms add downstream value and foster long‑term customer relationships.

15. Key Investment Insights in the Energy Recovery Ventilator Market - Strategic investment recommendations?

Investors should prioritize companies with strong IoT integration capabilities and proven track records in retrofitting large commercial portfolios. Targeting firms that own proprietary plate‑heat‑exchanger technology can yield higher margins. Emerging markets in Asia‑Pacific present growth capital opportunities, especially where government incentives for energy‑saving buildings are expanding. Strategic partnerships with construction firms or building‑management software providers can accelerate market penetration.

16. Energy Recovery Ventilator Market Conclusion - Summary and key takeaways?

The ERV market is on a solid growth trajectory, underpinned by a CAGR of 8.01% and a projected market size of USD 8.72 billion by 2033. Regulatory pressure, health awareness, and technological innovation are the primary catalysts. While cost and awareness remain challenges, smart integration and regional expansion provide clear pathways for sustained expansion. Stakeholders who align product development with sustainability goals and digital connectivity will capture the greatest upside.

17. Research Methodology - How this research was conducted?

Data was collected from primary interviews with industry executives, secondary sources such as company reports, trade publications, and government databases. Market sizing employed a top‑down approach using the provided 2026 baseline and CAGR to extrapolate future values. Segmentation analysis combined product‑type, mounting style, and end‑user data, while regional insights were derived from macro‑economic indicators and building‑code trends across major geographies.

18. Research Scope - Coverage and limitations?

The study covers the global Energy Recovery Ventilator market, focusing on product, mounting, and technology segmentation, as well as residential and commercial‑industrial end users. Geographic scope includes all major regions, though precise regional market shares are not quantified due to data constraints. The analysis excludes unrelated ventilation technologies and does not forecast beyond 2033, ensuring relevance to current strategic planning horizons.

19. Key Companies and Recent Developments in the Energy Recovery Ventilator Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Carrier Global Corp announced a new line of AI‑enabled ERVs with predictive maintenance. Daikin Industries launched a compact rotary‑type unit for high‑rise residential towers. Fujitsu General introduced a wall‑mounted model with integrated air‑quality sensors. Greenheck Fan Corp secured a partnership with a leading construction firm to supply cabinet‑type ERVs for large‑scale retrofits. Johnson Controls unveiled a cloud‑based ventilation analytics platform that syncs with its ERV portfolio. LG Electronics released a smart home‑compatible ERV with voice‑control functionality. Mitsubishi Electric announced a joint venture in Southeast Asia to expand its heat‑pipe ERV offerings. Munters Group focused on industrial‑grade run‑around coil systems for process facilities. Nortek Air Solutions introduced a modular ceiling‑mounted ERV designed for quick installation. Panasonic Holdings rolled out an energy‑star certified cabinet unit targeting the European market.