What is the Server Market Overview – definition, scope, and significance?

The Server Market comprises the design, manufacture, distribution, and support of computing hardware that provides centralized processing, storage, and networking capabilities for enterprises, cloud providers, and hyperscale data‑centers. It spans a broad scope that includes blade, rack, tower, and multinode configurations, as well as distinct server classes such as high‑end, mid‑range, and volume servers. These products serve a wide array of verticals—including BFSI, IT & Telecom, Government, Healthcare, Manufacturing, and Consumer Goods—enabling critical workloads like banking transactions, telecommunication routing, e‑government services, patient data management, industrial automation, and e‑commerce platforms. The market’s significance lies in its role as the backbone of digital transformation, supporting cloud adoption, AI/ML processing, and the explosion of data generated by IoT devices. A robust server ecosystem is essential for business continuity, scalability, and competitive advantage in today’s information‑driven economy.

What are the Server Market drivers, restraints, challenges, and opportunities?

Key drivers include rapid cloud migration, escalating data‑center capacity needs, and the surge in AI/ML workloads that demand high‑performance compute. Increasing adoption of edge computing and 5G expands demand for compact, energy‑efficient servers. Restraints stem from high capital expenditure for data‑center upgrades and supply‑chain disruptions that affect component availability. Challenges involve growing concerns over energy consumption and heat dissipation, as well as the need for skilled personnel to manage complex server environments. Opportunities arise from the emergence of liquid‑cooling technologies, the shift toward modular blade and multinode architectures, and the development of sustainable, low‑power server designs that align with ESG goals.

What are the current Server Market growth trends?

Current trends show a decisive move toward hyper‑converged infrastructure, where compute, storage, and networking are tightly integrated to simplify management. Hyperscale data‑centers favor rack‑mount and multinode servers for density and ease of scaling. Additionally, there is a noticeable rise in the deployment of high‑end servers equipped with GPUs and specialized accelerators for AI inference and training. The market also witnesses a growing preference for subscription‑based server leasing models, reflecting a shift from CapEx to OpEx spending. Finally, sustainability trends push vendors to offer servers with higher efficiency ratings and recyclable materials.

How did COVID‑19 impact the Server Market and what is the recovery trajectory?

The pandemic accelerated digital adoption as remote work, online education, and telehealth surged, creating an immediate spike in demand for data‑center capacity and, consequently, servers. While initial supply chain constraints caused short‑term shortages, the market rebounded quickly in late 2020 as manufacturers ramped up production. Recovery has continued robustly, with enterprises expanding cloud footprints and governments investing in digital public services. The trajectory remains upward, supported by post‑pandemic hybrid work models and ongoing investment in edge and AI infrastructure.

Who are the major competitors in the Server Market and what is the current competitive landscape?

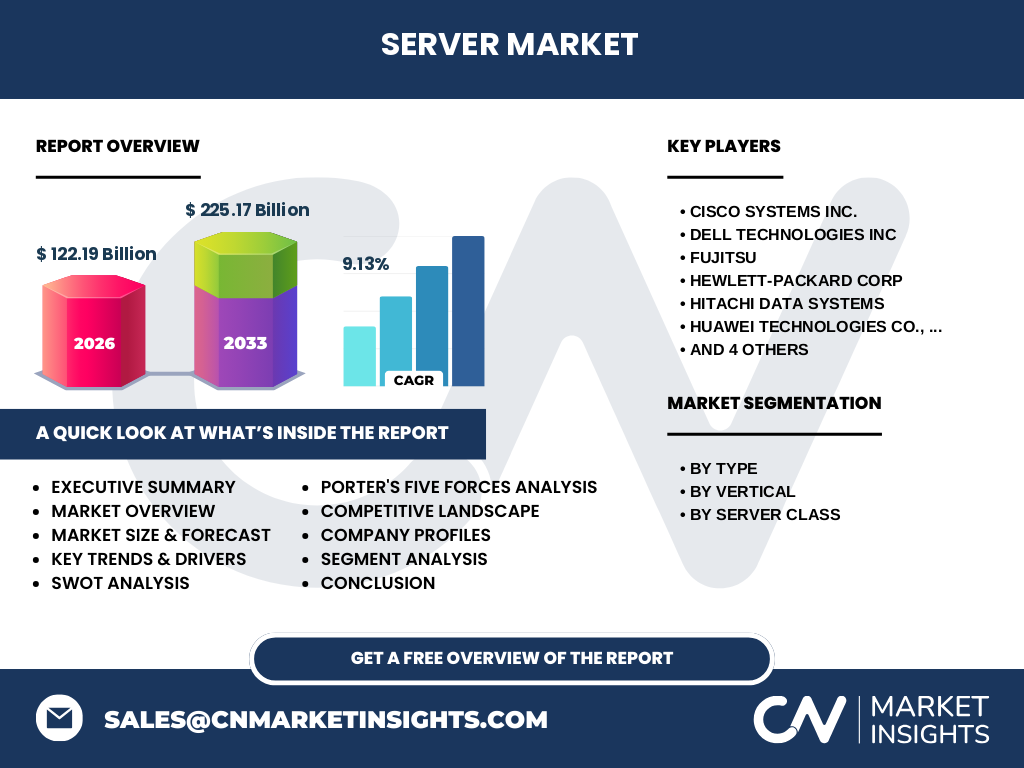

The competitive landscape is dominated by a mix of legacy OEMs and emerging Asian manufacturers. Key players include Cisco Systems Inc., Dell Technologies Inc., FUJITSU, Hewlett‑Packard Corp., Hitachi Data Systems, Huawei Technologies Co., Ltd, IBM Corporation, Inspur Technologies Co. Ltd, Lenovo, and Oracle Inc. The market has seen consolidation through strategic acquisitions—such as Dell’s integration of EMC—and partnership arrangements that enhance software‑defined networking and AI capabilities. Competition centers on performance, energy efficiency, total cost of ownership, and the ability to provide end‑to‑end solutions encompassing hardware, firmware, and cloud management platforms.

What are the key findings in the Executive Summary of the Server Market?

The Server Market is projected to grow from a 2026 valuation of $122.19 billion to $225.17 billion by 2033, reflecting a robust CAGR of 9.13 %. Growth is driven by cloud expansion, AI workload acceleration, and edge‑computing adoption across multiple verticals. Blade and rack servers dominate the type segmentation, while high‑end servers capture the most value due to performance‑intensive applications. The market remains highly competitive, with ten major vendors controlling a significant share, and is characterized by ongoing innovation in cooling, modularity, and subscription‑based offerings. Opportunities exist in sustainable server design and emerging demand from developing regions.

What is the Server Market forecast for the 2025‑2032 period?

Based on the provided CAGR of 9.13 %, the market is expected to maintain a steady upward trajectory throughout 2025‑2032. By 2028, the market size is anticipated to surpass $150 billion, reaching approximately $190 billion by 2030, and approaching the forecasted $225 billion mark by 2033. These figures indicate strong, consistent growth driven by expanding cloud services, AI/ML adoption, and the proliferation of edge data‑centers.

How is the Server Market size and share distributed by segmentation?

Segmentation by type includes Blade, Rack, Tower, and Multinode servers, with Blade and Rack solutions holding the largest share due to their scalability in hyperscale and enterprise data‑centers. By vertical, BFSI, IT & Telecom, and Government sectors represent the highest demand, reflecting the critical nature of transaction processing, network services, and public‑sector digitalization. The Server Class segmentation shows high‑end servers commanding a premium share because of their role in AI, scientific computing, and large‑scale virtualization, while mid‑range and volume servers serve broader enterprise workloads.

What is the global Server Market size and share by region?

The global market is anchored by North America and Asia‑Pacific, which together account for the majority of the $122.19 billion valuation in 2026. Europe also contributes a substantial share, driven by strong financial services and manufacturing bases. Emerging economies in Latin America and the Middle East & Africa are witnessing accelerated adoption due to digital government initiatives and growing cloud services, adding incremental growth to the overall market.

What are the key findings of the regional analysis of the Server Market?

North America leads in high‑end and AI‑optimized server deployments, propelled by major cloud providers and technology firms. Asia‑Pacific demonstrates the fastest growth rate, fueled by manufacturing automation, expanding telecommunications infrastructure, and aggressive government data‑center programs in China, India, and Southeast Asia. Europe shows steady growth, with a focus on sustainability and energy‑efficient server solutions to meet stringent regulatory standards. Each region presents distinct opportunities: North America for advanced AI workloads, Asia‑Pacific for volume and edge servers, and Europe for green‑technology adoption.

Which companies lead the Server Market and what are their strategic approaches?

Leading firms such as Dell Technologies, Hewlett‑Packard, and IBM focus on integrated solutions that combine hardware with proprietary management software and cloud services. Cisco emphasizes networking‑centric server architectures and hybrid cloud partnerships. Huawei and Inspur target price‑sensitive markets with high‑density, cost‑effective rack and blade offerings. Lenovo differentiates through customizable enterprise servers and strong channel partnerships. Oracle leverages its database and middleware ecosystem to sell integrated server‑software bundles. Across the board, strategies include expanding services revenue, investing in AI‑accelerated hardware, and pursuing sustainability certifications.

How does Porter’s Five Forces analysis apply to the Server Market?

• Threat of new entrants: Moderate to low, due to high capital requirements, technology barriers, and entrenched OEM relationships. • Bargaining power of suppliers: Moderate, as key components (processors, memory, storage) are sourced from a limited number of suppliers, though long‑term contracts mitigate risk. • Bargaining power of buyers: High, especially large cloud providers and enterprises that negotiate volume discounts and demand customized solutions. • Threat of substitutes: Low, because alternative computing models (e.g., serverless) still rely on underlying server infrastructure. • Industry rivalry: Intense, with ten major players competing on performance, price, service, and innovation, leading to frequent product launches and strategic alliances.

What are the strengths, weaknesses, opportunities, and threats (SWOT) of the Server Market?

Strengths: Fundamental role in digital infrastructure, strong demand across multiple verticals, and continuous technological innovation. Weaknesses: Capital‑intensive nature, dependence on component supply chains, and pressure on margins from high‑volume price competition. Opportunities: Growth in AI/ML workloads, edge‑computing expansion, sustainable server designs, and service‑based revenue models. Threats: Potential supply chain disruptions, escalating energy costs, and geopolitical tensions affecting cross‑border technology sales.

How is the Server Market value chain structured?

The value chain begins with component suppliers (CPU, memory, storage, networking chips), progresses to OEMs that design and assemble servers, followed by system integrators that customize solutions for specific customers. Distribution occurs through direct sales, channel partners, and cloud service providers. Post‑sale services—such as maintenance, firmware updates, and lifecycle management—constitute the final stage, increasingly delivered as subscription‑based offerings that generate recurring revenue.

What key investment insights can be drawn for the Server Market?

Investors should focus on companies that demonstrate strong R&D pipelines in AI accelerators and energy‑efficient designs, as these areas align with the market’s growth drivers. Firms expanding into subscription‑based services and offering end‑to‑end cloud‑ready solutions are positioned for higher-margin revenue. Geographic exposure to Asia‑Pacific offers the fastest growth potential, while North American leaders provide stability in high‑end segments. Strategic partnerships that enhance software‑defined capabilities also signal future upside.

What conclusions can be drawn from the Server Market analysis?

The Server Market is on a sustained growth path, underpinned by digital transformation, AI, and edge computing. While competition is fierce, leading vendors that invest in innovation, sustainability, and services are likely to capture the greatest share of the projected $225 billion market by 2033. Regional dynamics underline the importance of a diversified portfolio to exploit growth in both mature and emerging economies.

What research methodology was employed in this Server Market study?

The study combines primary interviews with industry experts, secondary data from reputable market reports, vendor financial statements, and technology forecasts. Quantitative estimates were derived using a top‑down approach anchored to the provided 2026 market size and CAGR, while qualitative insights were validated through cross‑verification with multiple sources.

What is the scope of this Server Market research?

The research covers global server hardware across all major configurations (blade, rack, tower, multinode) and classes (high‑end, mid‑range, volume). It includes analysis by vertical end‑users, regional performance, competitive dynamics, and forward‑looking forecasts through 2033. The scope excludes software‑only offerings, network‑only equipment, and niche micro‑server segments.

Which key companies are active in the Server Market and what recent developments have they announced?

• Cisco Systems Inc. – launched a new line of AI‑optimized UCS servers with integrated GPUs. • Dell Technologies Inc. – announced a subscription‑based server‑as‑a‑service program targeting mid‑market enterprises. • FUJITSU – introduced a liquid‑cooling solution for its high‑density rack servers. • Hewlett‑Packard Corp. – unveiled a sustainable server series with up to 40 % lower power consumption. • Hitachi Data Systems – expanded its hyper‑converged offerings for government data‑centers. • Huawei Technologies Co., Ltd – released a next‑gen 5G‑ready edge server platform. • IBM Corporation – integrated its Power10 processor into a new high‑end server for AI workloads. • Inspur Technologies Co. Ltd – secured a large procurement contract with a leading Chinese cloud provider. • Lenovo – announced modular blade servers designed for rapid scaling in hyperscale facilities. • Oracle Inc – rolled out a bundled Oracle‑engineered system that couples servers with autonomous database software. These announcements reflect a market emphasis on AI performance, energy efficiency, and subscription‑based business models.