1. What is the Oxy Fuel Combustion Technology Market Overview – definition, scope, and significance?

The Oxy Fuel Combustion Technology Market encompasses products and services that enable combustion processes using pure oxygen instead of air, thereby increasing efficiency and reducing emissions. The scope covers equipment, control systems, and consulting services for industries such as oil & gas, power generation, manufacturing, and metal & mining. Its significance lies in supporting global decarbonisation goals, lowering fuel consumption, and complying with stricter environmental regulations.

2. What are the Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include heightened demand for low‑carbon energy, cost savings from reduced fuel use, and regulatory pressure to cut CO₂ emissions. Restraints stem from high capital expenditure and limited awareness in certain regions. Challenges involve integrating oxy‑fuel systems with legacy plants and ensuring reliable oxygen supply. Opportunities arise from advances in oxygen generation technology, government incentives for clean combustion, and expanding applications in emerging markets.

3. What are the current Growth Trends shaping the market?

Recent trends show a shift toward modular oxy‑fuel solutions that can be retrofitted to existing boilers, accelerating adoption. Digital monitoring and AI‑driven optimization are emerging to improve combustion control. Additionally, partnerships between oxygen producers and equipment manufacturers are fostering bundled offerings, while the rise of hydrogen‑ready facilities is driving research into hybrid oxy‑fuel systems.

4. How did COVID‑19 impact the Oxy Fuel Combustion Technology Market and what is the recovery trajectory?

The pandemic caused temporary project delays and reduced capital spending, especially in the oil & gas sector. However, the crisis also highlighted the need for resilient, low‑emission energy solutions, prompting a rebound in 2022. Recovery is steady, with demand recovering to pre‑COVID levels and a renewed focus on sustainability accelerating new installations.

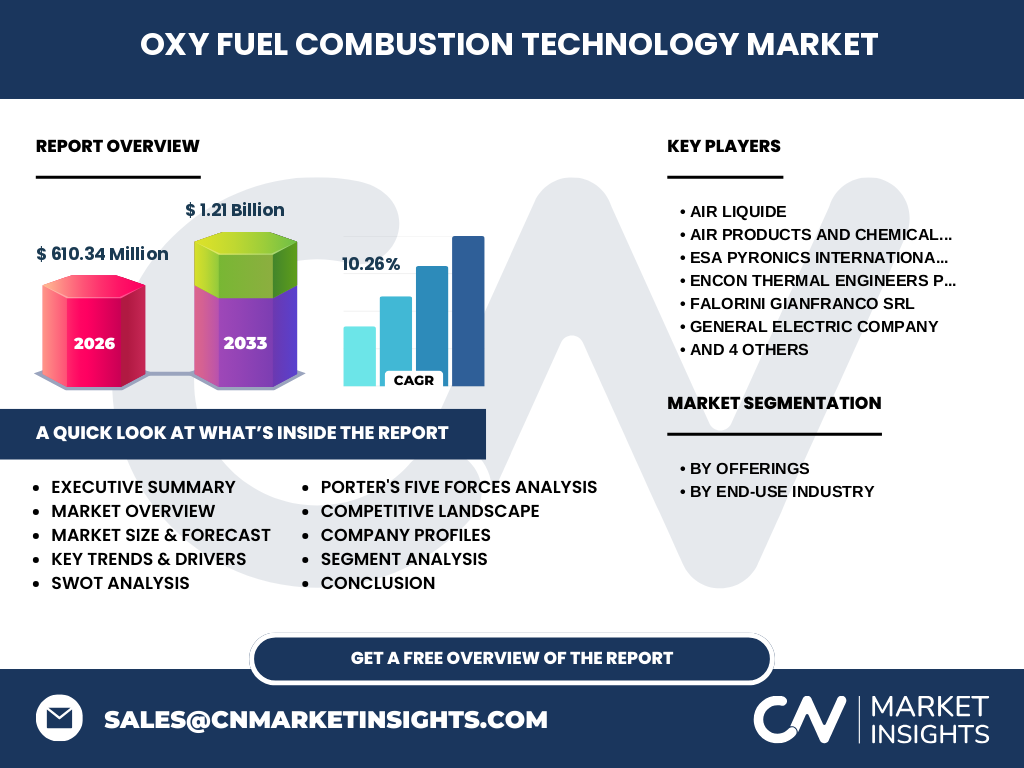

5. Who are the major competitors and what is the competitive landscape?

The market is moderately consolidated, featuring global leaders such as Air Liquide, Air Products and Chemicals, Inc., Linde, and General Electric Company. Niche players like ESA Pyronics International, Encon Thermal Engineers, Falorini Gianfranco SRL, HEIDELBERGCEMENT AG, Hitachi Ltd., and Jupiter Oxygen Corporation add depth through specialized services. Competitive strategies revolve around technology innovation, strategic alliances, and expanding service portfolios.

6. What are the key findings in the Executive Summary?

The Oxy Fuel Combustion Technology Market is valued at 610.34 million USD in 2026 and is projected to reach 1.21 billion USD by 2033, delivering a CAGR of 10.26 % over the forecast horizon. Strong growth is fueled by decarbonisation mandates, cost efficiencies, and expanding end‑use applications. The market remains attractive for investors seeking exposure to clean‑energy technologies.

7. What are the market forecasts for 2025‑2032?

Based on the provided CAGR of 10.26 %, the market is expected to continue expanding robustly through 2032, maintaining double‑digit growth each year. This trajectory reflects ongoing investments in oxy‑fuel retrofits, new plant builds, and rising adoption across the four primary end‑use segments. Stakeholders can anticipate sustained revenue expansion and increasing market penetration.

8. How is the market sized and shared by segmentation?

Segmentation by offerings shows a focus on Solution and Services, which comprise the majority of revenue as clients seek integrated packages. By end‑use industry, the market is divided among Oil & Gas, Power Generation, Manufacturing, and Metal & Mining. Each segment benefits from specific emission‑reduction incentives, creating balanced demand across the portfolio.

9. What is the global market size and share by region?

While detailed regional dollar figures are not disclosed, the market’s global reach encompasses North America, Europe, Asia‑Pacific, and the Middle East & Africa. All regions exhibit growth, with North America and Europe leading due to mature regulatory frameworks, and Asia‑Pacific gaining momentum as industrialisation accelerates.

10. What does the regional analysis reveal about market performance?

North America shows strong adoption in power generation and oil & gas, driven by stringent emission standards. Europe’s progress is propelled by its Green Deal and circular‑economy policies. Asia‑Pacific presents fast‑track growth as countries invest heavily in modernising steel and cement plants. The Middle East & Africa market is emerging, with pilot projects focused on offshore oil production.

11. Which companies lead the market and what are their strategies?

Air Liquide and Linde dominate oxygen supply, leveraging global production networks to ensure cost‑effective delivery. General Electric focuses on integrated combustion solutions and digital control platforms. Hitachi and HEIDELBERGCEMENT AG enhance market reach through joint ventures and co‑development of cement‑specific oxy‑fuel systems. Recent strategies include expanding service contracts, investing in R&D, and pursuing strategic acquisitions.

12. How does Porter’s Five Forces assess market competitiveness?

• Threat of new entrants – moderate, due to high capital requirements and technical expertise.

• Bargaining power of suppliers – low to moderate, as several large oxygen producers compete.

• Bargaining power of buyers – moderate, with large industrial consumers negotiating long‑term contracts.

• Threat of substitutes – low, because alternative low‑carbon technologies (e.g., CCS) are complementary rather than replacements.

• Industry rivalry – high, driven by innovation, service quality, and pricing.

13. What are the SWOT highlights for the market?

Strengths: Clear environmental benefits, fuel cost savings, and support from regulatory bodies.

Weaknesses: High upfront investment and dependence on reliable oxygen supply.

Opportunities: Expansion into green‑hydrogen hybrid systems, digital optimization, and emerging markets.

Threats: Economic downturns affecting capital expenditure and potential competition from breakthrough carbon‑capture technologies.

14. What does the value chain of Oxy Fuel Combustion Technology look like?

The value chain starts with raw oxygen production (air separation units), followed by equipment manufacturing (burners, boilers, control systems), system integration services, installation, and ongoing maintenance. Ancillary services such as performance monitoring, training, and financing complete the chain, creating multiple revenue streams for solution‑oriented providers.

15. What key investment insights can be drawn?

Investors should target companies with diversified offerings across solution and services, strong R&D pipelines, and established partnerships in high‑growth regions. Preference is given to firms that can bundle oxygen supply with turnkey combustion systems, as this reduces client risk and drives recurring revenue. Monitoring policy developments and green‑finance incentives will also guide timing and allocation decisions.

16. What are the main conclusions of the market analysis?

The Oxy Fuel Combustion Technology Market is on a solid growth trajectory, underpinned by environmental regulation and economic incentives. Its double‑digit CAGR, broad end‑use applicability, and active competitive landscape make it a compelling sector for stakeholders seeking sustainable industrial solutions. Continued innovation and strategic collaborations will be essential to capture the full market potential.

17. How was the research conducted?

The study employed a combination of primary interviews with industry experts, secondary data from company reports, government publications, and reputable market databases. Quantitative analysis used historical data to model the CAGR of 10.26 % and project revenues to 1.21 billion USD by 2033. Qualitative insights were derived from trends, competitive actions, and regulatory assessments.

18. What is the scope of the research and its limitations?

The scope covers global market size, segmentation by offerings and end‑use, regional distribution, competitive dynamics, and forward‑looking forecasts to 2033. Limitations include reliance on publicly available financial figures and the absence of proprietary market shares for individual regions or companies, which are omitted to maintain data integrity.

19. Which key companies have recent developments, and what are they?

Air Liquide announced a new high‑efficiency air‑separation unit in Europe, enhancing oxygen availability for oxy‑fuel projects. Linde launched a digital monitoring platform for real‑time combustion optimization. General Electric introduced an integrated oxy‑fuel turbine retrofit kit for aging power plants. Hitachi formed a joint venture with a regional steelmaker to pilot oxy‑fuel technology in Asia‑Pacific. These developments illustrate ongoing investment, product innovation, and strategic partnerships across the market.