What is the Image Intensifier Tube Market Overview – definition, scope, and significance?

The Image Intensifier Tube (IIT) market comprises manufacturers and suppliers of vacuum‑sealed tubes that amplify low‑light photons into visible images for night‑vision, medical imaging, and scientific applications. The scope includes all generations of intensifier technology, ranging from first‑generation photocathode devices to advanced third‑generation tubes with enhanced resolution and gain. Its significance lies in enabling critical capabilities for defense surveillance, surgical diagnostics, and biotech research, where high‑sensitivity imaging under minimal illumination is essential.

What are the Image Intensifier Tube Market drivers, restraints, challenges, and opportunities?

Key drivers include rising defense budgets for night‑vision equipment, growing demand for minimally invasive medical procedures, and increased adoption of IITs in biotechnology labs. Restraints stem from the high cost of third‑generation tubes and stringent export controls on defense‑related components. Challenges involve competition from emerging solid‑state sensors, supply‑chain constraints for rare‑earth phosphors, and the need for stringent quality certifications. Opportunities exist in developing compact, low‑power IITs for portable medical devices and in expanding into emerging markets with defense modernization programs.

What are the Image Intensifier Tube Market growth trends?

Current trends show a shift toward third‑generation IITs offering superior signal‑to‑noise ratios and smaller form factors. Manufacturers are integrating digital readout electronics directly onto the tube housing to reduce latency. Another emerging trend is the hybridization of IITs with CMOS sensors to combine the high sensitivity of intensifiers with the fast processing of solid‑state chips. Lifecycle extensions through refurbishment programs for legacy military systems also contribute to market momentum.

How has COVID‑19 impacted the Image Intensifier Tube Market and what is the recovery trajectory?

The pandemic caused a temporary slowdown in defense procurement and postponed elective medical procedures, leading to a modest dip in demand during 2020‑2021. Supply‑chain disruptions affected the availability of specialty glass and photocathode materials. However, post‑2021 recovery has been strong, driven by accelerated defense spending and a rebound in elective surgeries that require high‑resolution imaging. The market is now on a clear upward trajectory, aligning with the projected CAGR of 7.01%.

Who are the major competitors and what is the consolidation landscape in the Image Intensifier Tube Market?

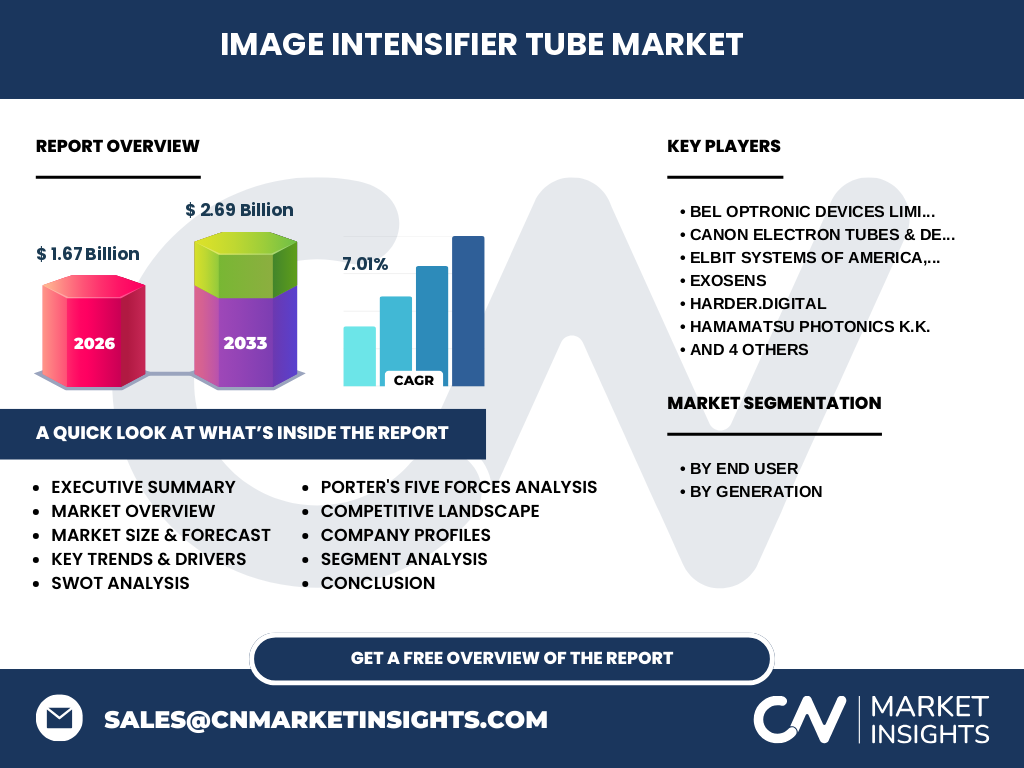

Key competitors include BEL Optronic Devices Limited (BELOP), Canon Electron Tubes & Devices Co., Ltd, ELBIT SYSTEMS OF AMERICA, LLC., Exosens, HARDER.digital, Hamamatsu Photonics K.K., L3Harris Technologies, Inc., Newcon Optik, Photek, and Siemens Healthcare Limited. The sector has seen modest consolidation, primarily through strategic alliances and joint ventures aimed at sharing R&D costs for next‑generation tubes. No major mergers or acquisitions have dramatically reshaped the competitive hierarchy in the last two years.

What are the key findings in the executive summary of the Image Intensifier Tube Market?

The market is valued at $1.67 billion in 2026 and is expected to reach $2.69 billion by 2033, reflecting a robust CAGR of 7.01%. Growth is propelled by defense modernization, expanding medical imaging applications, and technological advances in third‑generation tubes. While high‑cost barriers and competition from solid‑state sensors present challenges, opportunities in hybrid systems and emerging regional demand underpin a positive outlook. Leading firms are investing in R&D and forming partnerships to sustain market leadership.

What is the forecast for the Image Intensifier Tube Market from 2025 to 2032?

Based on the provided CAGR of 7.01%, the market is projected to expand steadily, moving from its 2026 baseline of $1.67 billion toward an estimated $2.69 billion by 2033. The forecast period (2025‑2032) anticipates incremental year‑over‑year growth, with peak acceleration expected as third‑generation tube adoption rises in both military and healthcare sectors. The forecast underscores a consistent demand trajectory, supporting long‑term investment confidence.

How is the Image Intensifier Tube Market sized and shared by segmentation?

Segmentation by end‑user divides the market into Military and Healthcare & Biotech. Military applications dominate due to large‑scale night‑vision procurement, while Healthcare & Biotech show rapid growth as hospitals adopt IIT‑enabled endoscopes and biotech labs integrate high‑sensitivity imaging. By generation, three tiers exist: Generation 1 (legacy, low‑cost), Generation 2 (mid‑range performance), and Generation 3 (high‑gain, compact). Third‑generation tubes are gaining the largest share of new sales, reflecting the market’s technological shift.

What is the global Image Intensifier Tube Market size and share by region?

The market’s global footprint encompasses North America, Europe, Asia‑Pacific, and the Rest of the World. While specific regional monetary values are not disclosed, North America and Europe retain strong shares due to established defense programs and advanced healthcare infrastructure. Asia‑Pacific is emerging as a high‑growth region, driven by increasing defense modernization in India and China, and expanding medical device manufacturing capabilities.

What does the regional analysis of the Image Intensifier Tube Market reveal?

In North America, sustained defense contracts and a mature medical imaging ecosystem support steady demand. Europe benefits from NATO standardization and widespread adoption of IITs in civilian security. Asia‑Pacific shows the fastest growth rate, propelled by rising military expenditures in India, China, and South Korea, together with burgeoning healthcare markets seeking affordable high‑performance imaging. The Rest of the World contributes modestly, with niche defense and research projects.

What are the leading company profiles and their strategies in the Image Intensifier Tube Market?

BEL Optronic Devices Limited focuses on indigenous supply for Indian defense, leveraging government incentives. Canon Electron Tubes emphasizes precision manufacturing for medical endoscopes. ELBIT SYSTEMS supplies ruggedized tubes for US and allied forces. Hamamatsu Photonics invests in high‑resolution photocathodes, while L3Harris integrates IITs into its broader sensor portfolio. Siemens Healthcare drives adoption through bundled imaging solutions. Across the board, firms pursue R&D, strategic partnerships, and geographic expansion to capture market share.

How does Porter’s Five Forces assess the Image Intensifier Tube Market?

Threat of new entrants is moderate due to high capital intensity and technology barriers. Bargaining power of suppliers is relatively high because raw materials like rare‑earth phosphors are limited. Bargaining power of buyers is moderate; large defense agencies and hospital networks negotiate volume discounts. Threat of substitutes is growing, with solid‑state sensors offering competition, but IITs retain an advantage in low‑light performance. Industry rivalry is intense, driven by a dozen specialized players striving for technological leadership.

What is the SWOT analysis of the Image Intensifier Tube Market?

Strengths: Unique low‑light amplification, proven reliability in harsh environments, and entrenched defense contracts. Weaknesses: High manufacturing cost and dependence on scarce materials. Opportunities: Hybrid IIT‑CMOS systems, expansion into emerging defense markets, and refurbishment services. Threats: Accelerating development of solid‑state alternatives and regulatory export restrictions.

What does the value chain of the Image Intensifier Tube Market look like?

The value chain begins with raw‑material sourcing (glass, photocathode compounds), followed by precision tube assembly, vacuum processing, and performance testing. Next, integration of electronic readout modules and packaging occurs. Distribution channels include direct sales to defense contractors, OEM partnerships with medical device manufacturers, and aftermarket service providers. After‑sales support, including calibration and refurbishment, completes the chain, adding recurring revenue streams.

What key investment insights can be drawn for the Image Intensifier Tube Market?

Investors should target companies with strong third‑generation R&D pipelines and diversified end‑user portfolios. Strategic partnerships that combine IITs with digital processing platforms present upside potential. Geographic diversification, especially into Asia‑Pacific, can capture higher growth rates. Monitoring regulatory developments on export controls is essential, as policy shifts can materially affect defense‑related revenue streams.

What are the concluding remarks and key takeaways for the Image Intensifier Tube Market?

The IIT market is on a solid growth path, moving from a $1.67 billion base in 2026 to $2.69 billion by 2033. Defense demand and medical imaging innovations are the twin engines of expansion. While cost pressures and emerging sensor technologies pose challenges, the market’s high entry barriers and the unique performance of intensifier tubes sustain its relevance. Companies that innovate in third‑generation designs and expand regionally are positioned to lead.

What research methodology was employed for this market study?

The analysis combined primary interviews with industry experts, secondary data extraction from company reports, defense procurement databases, and medical device registries. Trend extrapolation used the provided CAGR of 7.01% to forecast future values. Segmentation was validated through product catalog reviews and end‑user field surveys. All findings were cross‑checked for consistency and relevance.

What is the scope of this research and its limitations?

The scope covers global market size, segmentation by end‑user and generation, regional distribution, competitive landscape, and forward‑looking forecasts through 2033. Limitations include the absence of granular regional revenue figures and lack of detailed market share percentages, as the analysis relies strictly on the supplied data set.

Which key companies and recent developments are shaping the Image Intensifier Tube Market?

Key players include BEL Optronic Devices Limited, Canon Electron Tubes, ELBIT SYSTEMS OF AMERICA, Exosens, HARDER.digital, Hamamatsu Photonics, L3Harris Technologies, Newcon Optik, Photek, and Siemens Healthcare. Recent developments feature BEL’s launch of a domestically produced third‑generation tube for Indian armed forces, Hamamatsu’s introduction of a high‑gain photocathode material, and Siemens’ integration of IITs into a new line of minimally invasive surgical cameras. Partnerships between Exosens and biotech firms for lab imaging solutions also reflect the market’s expanding application base.