What is the Data Center Equipment Market Overview – definition, scope, and significance?

The Data Center Equipment Market comprises hardware that powers, stores, processes, and cools digital workloads in enterprise and hyperscale facilities. It includes servers, storage devices, cooling systems, power distribution units (PDUs), racks, and enclosures across Tier‑1 to Tier‑4 classifications. The market’s significance stems from exponential data growth, cloud adoption, and the need for high‑availability infrastructure, making equipment procurement a strategic asset for digital transformation worldwide.

What are the primary drivers, restraints, challenges, and opportunities in the Data Center Equipment Market?

Key drivers include rising cloud services, edge‑computing expansion, and demand for high‑performance computing. Restraints involve high capital expenditure and energy‑intensity of Tier‑4 facilities. Challenges arise from supply‑chain disruptions and the rapid obsolescence of hardware. Opportunities are found in modular designs, AI‑optimized cooling, and sustainable power solutions that lower operating costs while meeting stricter environmental regulations.

What growth trends are currently shaping the Data Center Equipment Market?

Emerging trends feature a shift toward hyperscale deployments, increased adoption of liquid‑cooling technologies, and the integration of software‑defined infrastructure. Vendors are also bundling compute and storage in composable architectures, while Tier‑3 and Tier‑4 data centers prioritize redundancy and energy efficiency to support mission‑critical workloads.

How did COVID‑19 impact the Data Center Equipment Market and what is the recovery trajectory?

The pandemic accelerated remote work and digital services, prompting a surge in demand for compute and storage capacity. Although initial supply‑chain constraints slowed shipments, the market quickly rebounded as cloud providers expanded capacity. Recovery is now robust, with growth sustained by post‑pandemic digitalization and the continued rollout of 5G and IoT services.

Who are the major competitors and what is the consolidation landscape in the Data Center Equipment Market?

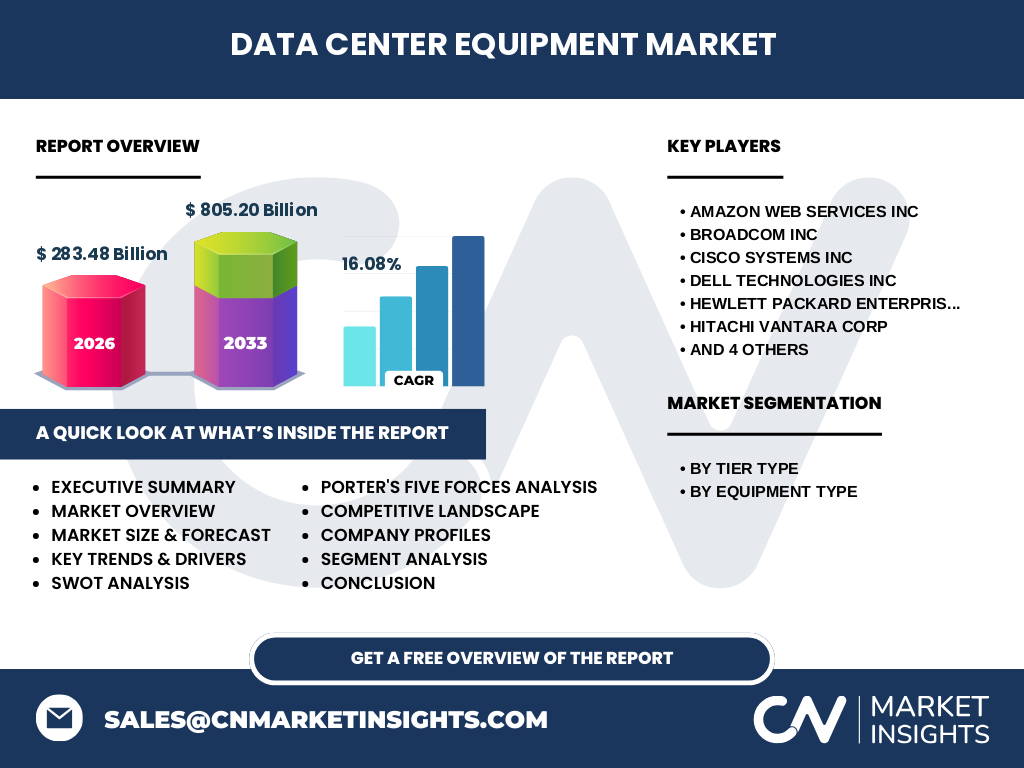

Leading competitors include Amazon Web Services Inc, Broadcom Inc, Cisco Systems Inc, Dell Technologies Inc, Hewlett Packard Enterprise Co, Hitachi Vantara Corp, International Business Machines Corp, Kyndryl Holdings Inc, Microsoft Corp, and Oracle Corp. The sector is witnessing consolidation through strategic acquisitions and partnerships, allowing vendors to broaden product portfolios and enhance end‑to‑end service offerings.

What are the key findings highlighted in the Executive Summary?

The market is projected to grow from a 2026 size of $283.48 billion to $805.20 billion by 2033, reflecting a robust CAGR of 16.08 %. Growth is fueled by cloud expansion, tier‑upgrading, and sustainability initiatives. Competitive dynamics indicate a few dominant players leveraging ecosystem integrations, while emerging technologies such as AI‑driven cooling and composable hardware create new avenues for differentiation.

What is the forecast for the Data Center Equipment Market through 2032?

Based on the provided CAGR of 16.08 %, the market is expected to maintain strong upward momentum, reaching well beyond $800 billion by the end of the forecast horizon. This trajectory underscores continued investment in high‑density infrastructure, especially in Tier‑3 and Tier‑4 facilities, and reinforces the strategic importance of scalable, energy‑efficient equipment.

How is the Data Center Equipment Market sized and shared by segment?

Segmentation by Tier Type includes Tier‑1, Tier‑2, Tier‑3, and Tier‑4 facilities, each demanding distinct equipment reliability levels. By Equipment Type, the market splits into servers, storage devices, cooling equipment, power distribution units, racks, and enclosures. While exact monetary shares are not disclosed, Tier‑3 and Tier‑4 segments command premium pricing due to redundancy requirements, whereas servers and storage drive the highest volume sales.

What is the global geographic distribution of the Data Center Equipment Market?

The market exhibits a worldwide footprint, with major demand clusters in North America, Europe, and the Asia‑Pacific region. These regions host the largest hyperscale operators and benefit from advanced manufacturing capabilities, ensuring steady procurement of servers, cooling solutions, and power infrastructure. Geographic expansion is further supported by emerging markets investing in Tier‑2 and Tier‑3 data centers.

What does the regional analysis reveal about market performance?

North America leads in high‑value Tier‑4 deployments, driven by leading cloud providers. Europe emphasizes sustainability, prompting adoption of energy‑efficient cooling and power solutions. The Asia‑Pacific region shows the fastest growth rate, fueled by rapid digital transformation, mobile broadband rollout, and increasing enterprise data center projects across Tier‑2 and Tier‑3 classifications.

What are the profiles of leading companies and their strategic approaches?

Amazon Web Services Inc leverages its cloud backbone to integrate proprietary servers and cooling. Broadcom Inc focuses on networking ASICs and storage adapters. Cisco Systems Inc drives convergence through unified networking and power solutions. Dell Technologies Inc and Hewlett Packard Enterprise Co offer end‑to‑end rack‑and‑stack offerings. Hitachi Vantara Corp emphasizes data‑centric storage, while IBM and Oracle provide hybrid cloud‑tuned hardware. Kyndryl Holdings Inc and Microsoft Corp pursue managed services that embed equipment into long‑term contracts.

How does Porter’s Five Forces assess the Data Center Equipment Market?

Threat of new entrants is moderate due to high capital barriers and technology expertise. Bargaining power of suppliers is low to moderate as component markets are competitive. Bargaining power of buyers is high, with large cloud operators consolidating purchases. Threat of substitutes remains low because alternatives to physical hardware (e.g., pure software services) still require underlying equipment. Rivalry among existing firms is intense, driven by innovation cycles and service bundling.

What are the SWOT insights for the Data Center Equipment Market?

Strengths: Growing demand for high‑performance compute, strong vendor ecosystems. Weaknesses: Capital intensity and reliance on complex supply chains. Opportunities: Sustainable cooling, modular designs, AI‑optimized hardware. Threats: Geopolitical trade tensions, rapid product obsolescence, and potential regulatory shifts on energy consumption.

How is the value chain structured in the Data Center Equipment Market?

The value chain begins with component suppliers (semiconductors, steel, plastics), proceeds to OEMs that assemble servers, storage, and cooling units, followed by system integrators that configure Tier‑specific solutions. Distribution channels include direct sales to hyperscale operators and indirect channels through VARs. After‑sales services, maintenance contracts, and end‑of‑life recycling complete the chain, adding recurring revenue streams.

What key investment insights should stakeholders consider?

Investors should target companies with strong R&D pipelines in energy‑efficient cooling and composable infrastructure. Partnerships that expand service‑oriented revenue (managed PDU or cooling as a service) present higher margins. Geographic diversification, especially into fast‑growing Asia‑Pacific markets, can capture incremental demand for Tier‑2 and Tier‑3 facilities.

What conclusions can be drawn about the Data Center Equipment Market?

The market is on a clear expansion path, underpinned by digital acceleration and sustainability imperatives. Tier‑3 and Tier‑4 facilities will dominate value creation, while servers and storage maintain volume leadership. Competitive pressure will intensify, rewarding innovators who combine hardware excellence with integrated services and green solutions.

What research methodology was employed for this report?

Primary data were gathered through interviews with industry executives, supplier surveys, and technology experts. Secondary sources included company filings, press releases, and reputable market databases. Quantitative forecasting applied compound annual growth rate (CAGR) modeling, while qualitative analysis leveraged Porter’s framework and SWOT assessments.

What is the scope of the research and its limitations?

The study covers global equipment categories, Tier classifications, and the top ten listed vendors. It focuses on the 2026 baseline and 2027‑2033 forecast horizon. Geographic granularity is limited to major regions, and exact market‑share percentages are not disclosed due to confidentiality of proprietary datasets.

Which key companies have announced recent developments in the Data Center Equipment Market?

Amazon Web Services Inc unveiled a new energy‑efficient server line optimized for AI workloads. Broadcom Inc released next‑generation networking chips to improve data throughput. Cisco Systems Inc launched an integrated power‑over‑Ethernet cooling platform. Dell Technologies Inc announced a modular rack system for rapid Tier‑4 scaling. Hewlett Packard Enterprise Co introduced AI‑driven predictive maintenance for PDUs. Hitachi Vantara Corp released high‑density storage arrays, while IBM rolled out hybrid cloud‑ready servers. Microsoft Corp disclosed a partnership with a leading cooling‑technology firm, and Oracle Corp expanded its engineered systems portfolio with enhanced security features.