What is the Architecture Software Market Overview – definition, scope, and significance?

The Architecture Software Market comprises digital tools that enable architects, engineers, and design firms to create, visualize, and manage building projects. It spans desktop, cloud‑based, and mobile applications covering drafting, BIM (Building Information Modeling), rendering, and project collaboration. The market is significant because it drives efficiency, reduces construction errors, supports sustainable design, and meets the growing demand for rapid project delivery in both commercial and institutional sectors.

What are the key drivers, restraints, challenges, and opportunities shaping the Architecture Software Market?

Key drivers include increasing adoption of BIM, rising construction activity in emerging economies, and the need for remote collaboration accelerated by digital transformation. Restraints involve high licensing costs and steep learning curves for advanced tools. Challenges stem from interoperability issues among disparate platforms and data security concerns. Opportunities arise from AI‑enhanced design automation, subscription‑based pricing models, and expanding market penetration among small‑to‑mid‑size enterprises.

What are the current growth trends in the Architecture Software Market?

Current trends feature a shift toward cloud‑native solutions that enable real‑time collaboration across globally distributed teams. AI and machine‑learning algorithms are being integrated to automate code compliance checks and generate design alternatives. Moreover, the market is witnessing a rise in modular subscription tiers—basic, advance, and pro—catering to varied user needs, and an expanding ecosystem of third‑party plugins that extend functionality.

How has COVID‑19 impacted the Architecture Software Market and what is the recovery trajectory?

During the pandemic, demand for remote collaboration tools surged as project teams moved to virtual environments, accelerating cloud adoption. Although on‑site construction slowed, software sales remained resilient, and many firms increased investment in digital twins to sustain progress. The recovery trajectory is positive, with the market expected to continue its rapid expansion as construction activity rebounds and firms retain the digital workflows adopted during COVID‑19.

Who are the major competitors and what is the level of consolidation in the Architecture Software Market?

The competitive landscape features established players such as Autodesk Inc, Dassault Systèmes, Trimble Inc, and Vectorworks, Inc., alongside niche providers like ActCAD LLC, Bluebeam, Inc, and Chief Architect, Inc. Consolidation is moderate; larger firms acquire specialized technology startups to broaden their BIM and visualization portfolios, while smaller firms focus on differentiation through industry‑specific features and pricing flexibility.

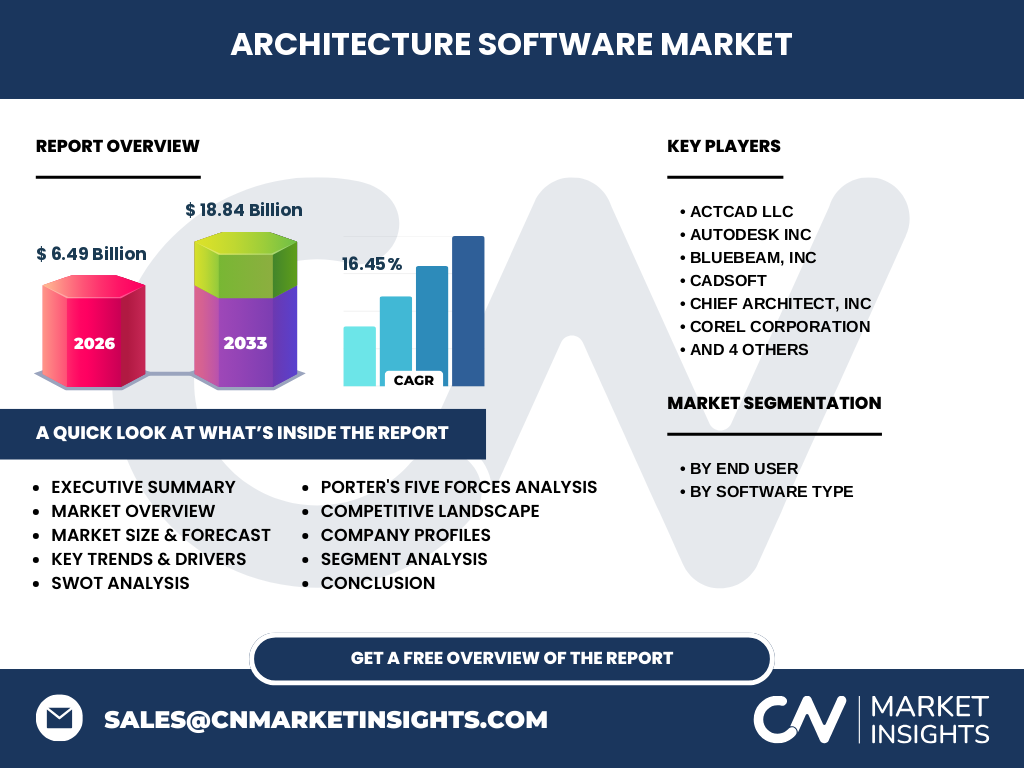

What are the high‑level findings presented in the Executive Summary?

The Architecture Software Market is valued at $6.49 billion in 2026 and is projected to reach $18.84 billion by 2033, reflecting a robust CAGR of 16.45 %. Growth is fueled by BIM adoption, cloud migration, and AI‑driven design tools. Enterprise and institutional end users dominate demand, while the pro software tier captures the highest revenue share. Competitive dynamics are shaped by strategic acquisitions and expanding subscription models.

What are the forecast projections for the Architecture Software Market from 2025 to 2032?

Based on a 16.45 % CAGR, the market will expand from its 2026 baseline of $6.49 billion to approximately $18.84 billion by 2033. This trajectory suggests steady annual growth, with each subsequent year adding roughly $2–3 billion in revenue, driven by increasing penetration of advanced and pro‑level software across enterprises and institutions worldwide.

How is the Architecture Software Market sized and shared by segmentation?

Segmentation by end user divides the market into enterprises and institutions, with enterprises typically adopting higher‑tier solutions for complex projects. By software type, the market consists of basic, advance, and pro tiers. Basic solutions address drafting and 2D design needs, advance packages add BIM and collaboration features, while pro offerings deliver full‑stack AI‑assisted design, simulation, and integration capabilities. Revenue share aligns with the sophistication of user requirements, with pro solutions capturing the largest proportion.

What is the geographic distribution of the Architecture Software Market?

The market exhibits a global footprint, with strong adoption in North America and Europe due to mature construction sectors and early BIM implementation. Asia‑Pacific shows rapid growth driven by large infrastructure projects and urbanization. Emerging markets in Latin America and the Middle East are beginning to invest in digital design tools, contributing to overall market expansion.

What does the regional analysis reveal about Architecture Software Market performance?

North America leads in revenue, propelled by major software vendors and high R&D investment. Europe follows closely, with stringent regulatory standards encouraging BIM use. Asia‑Pacific registers the highest growth rate, reflecting governmental push for smart city initiatives and increased construction spending. Regions such as Africa and the Middle East display nascent yet promising adoption patterns as local firms modernize their design processes.

Which companies are leading in the Architecture Software Market and what are their strategic approaches?

Key players include Autodesk Inc, Dassault Systèmes, Trimble Inc, and Vectorworks, Inc., which focus on platform integration, AI features, and subscription flexibility. Niche innovators like ActCAD LLC, Bluebeam, Inc, and Chief Architect, Inc emphasize specialized vertical solutions and user‑friendly interfaces. Most leaders pursue strategic partnerships, cloud service expansions, and regular product launches to maintain competitive advantage.

How does Porter’s Five Forces model apply to the Architecture Software Market?

• Threat of new entrants is moderate; high development costs and established brand loyalty create barriers. • Bargaining power of buyers is increasing as enterprises demand flexible licensing and interoperability. • Supplier power is low because software components are largely interchangeable. • Threat of substitutes is limited, with few alternatives to comprehensive design suites. • Competitive rivalry is intense, driven by rapid innovation cycles and frequent product updates.

What are the SWOT insights for the Architecture Software Market?

Strengths: Strong demand for BIM, high switching costs, and robust R&D ecosystems. Weaknesses: Complex pricing structures and steep learning curves. Opportunities: AI‑driven automation, expansion into emerging markets, and subscription‑based models. Threats: Data security concerns, potential regulatory changes, and competition from open‑source platforms.

What does the value chain analysis reveal about the Architecture Software Market?

The value chain starts with research & development, followed by software engineering, cloud infrastructure provisioning, and licensing. Distribution occurs through direct sales, reseller networks, and online marketplaces. Post‑sale services include training, technical support, and regular updates. Value is created primarily through continuous innovation and integration of emerging technologies such as AI and VR.

What key investment insights can be drawn for stakeholders in the Architecture Software Market?

Investors should focus on companies offering scalable cloud platforms and AI‑enhanced design tools, as these areas promise the highest growth. Acquisitions of niche firms with proprietary plugins can accelerate product diversification. Prioritizing subscription revenue models reduces churn and improves cash flow stability. Geographic diversification into Asia‑Pacific provides exposure to the fastest‑growing demand base.

What are the main conclusions of the Architecture Software Market report?

The Architecture Software Market is on a strong upward trajectory, with a projected three‑fold increase by 2033. Digital transformation, BIM adoption, and AI integration are the primary catalysts. Enterprises and institutions are the main end users, with pro‑level software leading revenue generation. Competitive dynamics will be shaped by innovation speed, strategic acquisitions, and the shift toward subscription licensing.

How was the research methodology designed for this Architecture Software Market report?

The study combined primary interviews with industry experts, secondary data from company filings, market databases, and reputable industry publications. Quantitative analysis employed top‑down and bottom‑up approaches to validate the $6.49 billion 2026 base and the $18.84 billion 2033 forecast. Trend extrapolation used historical CAGR and scenario modeling to ensure reliability.

What is the scope of this Architecture Software Market research?

The research covers global market size, segmentation by end user and software type, regional performance, competitive landscape, and forward‑looking forecasts through 2033. It excludes unrelated construction equipment markets and limits financial metrics to the figures provided. The study emphasizes strategic insights rather than detailed pricing breakdowns.

Which key companies and recent developments are notable in the Architecture Software Market?

Notable companies include Autodesk Inc, which launched a new AI‑assisted design suite; Dassault Systèmes, expanding its cloud BIM platform; Trimble Inc, introducing integrated hardware‑software solutions for construction sites; and Vectorworks, Inc., releasing a collaborative cloud module. Smaller players such as ActCAD LLC and progeSOFT have announced partnerships to broaden distribution in emerging markets, and Bluebeam, Inc introduced enhanced PDF collaboration tools tailored for remote project teams.