1. What is the Industrial Networking Solutions Market, including its definition, scope, and significance?

The Industrial Networking Solutions Market encompasses products and services that enable reliable, secure, and real‑time communication among machines, sensors, controllers, and enterprise IT systems in manufacturing, energy, transportation, and other heavy‑industry sectors. Its scope covers hardware (switches, routers, gateways), software and services (network management, security, edge analytics), and both wired and wireless connectivity. The market is significant because it underpins Industry 4.0, automation, predictive maintenance, and the digital transformation of factories worldwide.

2. What are the primary drivers, restraints, challenges, and opportunities influencing market growth?

Key drivers include the rapid adoption of IIoT, demand for high‑speed deterministic networking, and government initiatives supporting smart factories. Restraints stem from legacy equipment compatibility issues and high upfront CAPEX. Challenges involve cybersecurity threats, skill gaps in network engineering, and complex integration across heterogeneous protocols. Opportunities arise from emerging 5G and private‑network deployments, edge‑computing services, and growing demand for modular, scalable solutions in emerging economies.

3. Which current and emerging trends are shaping the Industrial Networking Solutions Market?

Current trends feature the shift to time‑sensitive networking (TSN), convergence of IT and OT domains, and increased use of managed services. Emerging trends include AI‑driven network optimization, integration of 5G‑based private networks, and the rise of software‑defined networking (SD‑N) for flexible plant reconfiguration. Vendors are also expanding portfolio breadth by bundling hardware with cloud‑native analytics and security subscriptions.

4. How did COVID‑19 affect the Industrial Networking Solutions Market, and what is the recovery trajectory?

The pandemic initially disrupted supply chains and delayed capital projects, reducing short‑term sales. However, lockdown‑driven emphasis on automation and remote monitoring accelerated digital‑infrastructure investments. Post‑2020, the market rebounded strongly, with manufacturers prioritizing resilient, connected factories to mitigate future disruptions. Recovery is now on a growth path, reinforcing the long‑term upside driven by Industry 4.0 initiatives.

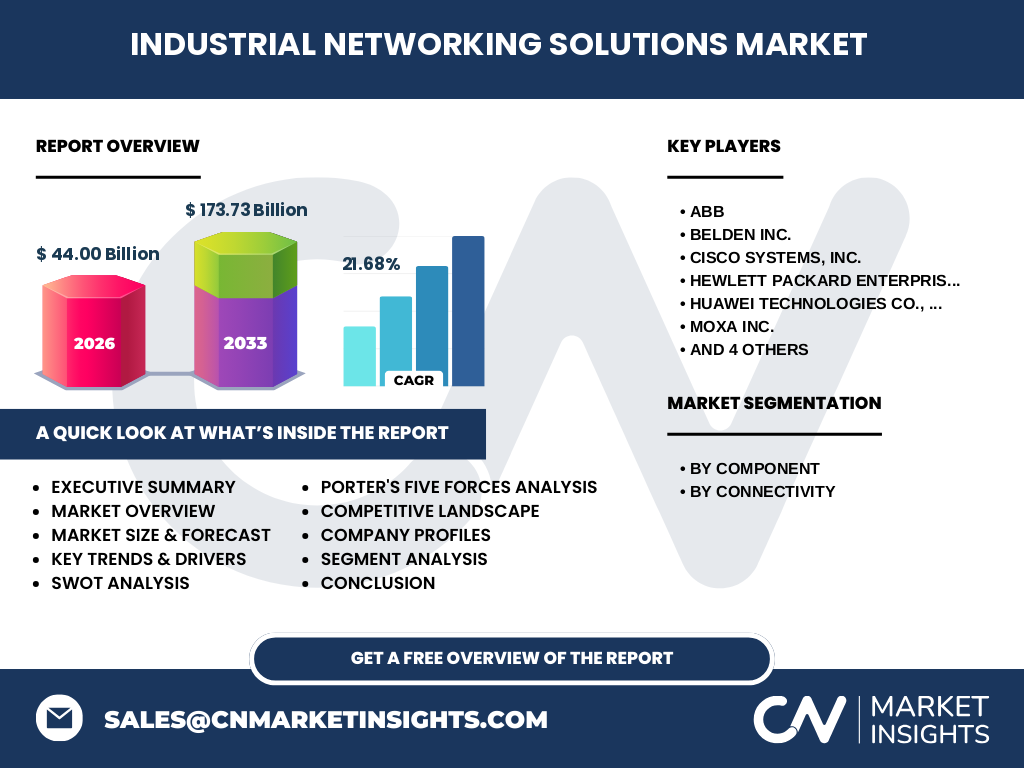

5. Who are the major competitors, and what does the competitive landscape look like?

The market is led by a mix of traditional industrial automation players and global networking giants. Key competitors include ABB, Belden Inc., Cisco Systems, Hewlett Packard Enterprise Development LP, Huawei Technologies, Moxa Inc., Nokia, Rockwell Automation, Semtech, and Siemens. Consolidation is moderate, with strategic acquisitions focused on edge‑computing, 5G, and security capabilities, creating a competitive environment where breadth of portfolio and ecosystem partnerships are critical.

6. What are the high‑level takeaways and key findings of the Industrial Networking Solutions Market?

The market is poised for rapid expansion, projected to reach $173.73 billion by 2033, driven by a 21.68% CAGR. Growth is fueled by digitization, 5G rollout, and demand for deterministic, secure connectivity. Hardware and software/services segments both benefit, with a balanced shift toward wireless solutions for flexibility. The competitive arena is consolidating around integrated, managed offerings, while regional demand spikes in Asia‑Pacific and Europe.

7. What are the market forecasts for 2025‑2032?

Based on the provided CAGR of 21.68%, the market is expected to expand from its 2026 size of $44.00 billion to roughly $173.73 billion by 2033. This trajectory suggests a sustained, high‑growth environment throughout 2025‑2032, with annual increments driven by increasing adoption of IIoT, private 5G, and cloud‑edge integration across manufacturing verticals.

8. How is the market sized and shared by component and connectivity segmentation?

Segmented by component, the market splits between hardware (physical switches, routers, gateways) and software & services (network management, security, analytics). By connectivity, it divides into wired solutions, which dominate deterministic, high‑throughput environments, and wireless solutions, gaining traction for flexible, mobile, and remote‑asset monitoring. While exact numeric shares are undisclosed, both segments are experiencing parallel growth as manufacturers seek hybrid architectures.

9. What is the global market size and share distribution by region?

Globally, the market reached $44.00 billion in 2026 and is projected to climb to $173.73 billion by 2033. Geographic distribution reflects strong demand in North America and Europe due to mature industrial bases, while rapid expansion is observed in the Asia‑Pacific region, where rising manufacturing capacity and government digital‑industry programs drive adoption. The Middle East and Africa show incremental growth, primarily in oil‑&‑gas and utilities.

10. What are the detailed regional performance insights?

In North America, growth is propelled by advanced factory automation and early 5G private‑network deployments. Europe benefits from stringent Industry 4.0 regulations, strong OEM presence, and cross‑border standardization efforts. Asia‑Pacific leads in volume, with China, India, Japan, and South Korea investing heavily in smart‑factory pilots and upgrading legacy plants. Latin America and the Middle East exhibit niche growth tied to specific sectors such as automotive and energy.

11. Which leading companies dominate, and what strategies are they employing?

ABB focuses on integrated automation suites and edge‑compute gateways. Belden leverages its robust cabling legacy to expand into managed Ethernet switches. Cisco bets on end‑to‑end networking with strong security layers and cloud integration. HPE drives hyper‑converged infrastructure for industrial edge. Huawei pushes 5G‑enabled routers, while Nokia emphasizes private‑network services. Rockwell and Siemens combine hardware expertise with software ecosystems, and Moxa targets rugged, compact solutions for harsh environments. Semtech contributes specialized RF components for wireless links.

12. How do Porter’s Five Forces affect the market?

• Threat of new entrants: Moderate, due to high capital requirements and technology expertise. • Bargaining power of suppliers: Low‑to‑moderate, as component sourcing is diversified. • Bargaining power of buyers: Increasing, as OEMs demand flexible, cost‑effective solutions and can switch vendors. • Threat of substitutes: Limited, because industrial networking requires specialized, reliable hardware. • Competitive rivalry: High, driven by rapid innovation, acquisitions, and the need for end‑to‑end offerings.

13. What are the SWOT highlights for the market?

Strengths: Strong growth drivers, essential role in digital transformation, and expanding ecosystem. Weaknesses: High upfront costs and integration complexity. Opportunities: 5G private networks, AI‑enabled network management, and growth in emerging economies. Threats: Cybersecurity risks, potential supply‑chain bottlenecks, and regulatory variations across regions.

14. How does the value chain of Industrial Networking Solutions operate?

The value chain begins with raw component suppliers (semiconductors, copper, fiber). Manufacturers design and assemble hardware, then integrate firmware and software platforms. System integrators configure solutions for end users, while service providers offer monitoring, security, and analytics as recurring revenue. Final customers—manufacturers, energy firms, and transportation operators—consume the solutions to enable real‑time data exchange and automation.

15. What investment insights can be drawn for stakeholders?

Investors should target companies with strong hybrid portfolios (hardware plus software services) and those advancing 5G/TSN capabilities. Strategic M&A in edge‑computing and cybersecurity can accelerate market share. Geographic focus on Asia‑Pacific offers volume growth, while North America and Europe provide premium, high‑margin opportunities. Partnerships with cloud providers and system integrators enhance recurring‑revenue models.

16. What are the concluding key takeaways from the market analysis?

The Industrial Networking Solutions Market is on a steep growth trajectory, underpinned by a 21.68% CAGR and a projected $173.73 billion valuation by 2033. Connectivity is shifting toward hybrid wired‑wireless architectures, with software services gaining parity with hardware. Competitive pressure is fostering consolidation and innovation, especially around 5G, AI, and security. Regional demand is strongest in Asia‑Pacific, but mature markets continue to drive high‑value deployments.

17. Which research methodology was employed to compile this report?

The study combined primary interviews with industry executives, supplier surveys, and secondary data from company filings, trade publications, and market databases. Trend analysis, CAGR extrapolation, and cross‑validation with macroeconomic indicators ensured reliability. Qualitative insights were triangulated with the provided financial figures to produce a coherent, data‑backed outlook.

18. What is the scope of the research, including coverage and limitations?

The research covers global Industrial Networking Solutions, segmented by component (hardware, software & services) and connectivity (wired, wireless). It includes major players, regional performance, and forward‑looking forecasts to 2033. Limitations stem from the absence of granular market‑share percentages and proprietary financial data beyond the supplied figures; however, qualitative analysis compensates by focusing on strategic trends and competitive dynamics.

19. Which key companies have announced recent developments, and what are those initiatives?

ABB launched a new edge‑gateway series supporting TSN and AI analytics. Belden introduced a modular industrial Ethernet switch line designed for rapid scaling. Cisco announced expanded 5G private‑network services bundled with cybersecurity suites. HPE rolled out hyper‑converged edge platforms integrated with its GreenLake consumption model. Huawei unveiled a 5G‑enabled router for harsh‑environment plants. Moxa released compact, ultra‑rugged wireless bridges. Nokia secured multiple private‑network contracts in Europe. Rockwell Automation and Siemens partnered on an open‑architecture automation framework, while Semtech announced advanced RF modules for industrial IoT deployments.