1. What is the UPS Battery Market Overview – definition, scope, and significance?

The UPS (Uninterruptible Power Supply) Battery Market comprises all battery types and technologies used to provide backup power for UPS systems. Its scope covers manufacturing, distribution, and servicing of batteries for commercial, residential, and other applications worldwide. These batteries are critical for safeguarding data centers, hospitals, manufacturing lines, and home offices against power interruptions, thereby ensuring operational continuity, equipment protection, and compliance with reliability standards.

2. What are the UPS Battery Market drivers, restraints, challenges, and opportunities?

Key drivers include the rising adoption of critical IT infrastructure, increased reliance on renewable energy storage, and stricter uptime requirements across industries. Restraints stem from high upfront costs of advanced chemistries such as lithium‑ion and regulatory compliance burdens. Challenges involve managing battery lifespan, disposal, and safety concerns, especially with lead‑acid units. Opportunities arise from the growing demand for lightweight, high‑density lithium‑ion solutions, government incentives for green energy storage, and the emergence of smart‑monitoring technologies.

3. What are the current UPS Battery Market growth trends?

Current trends highlight a shift from traditional lead‑acid batteries toward lithium‑ion due to superior cycle life and lower maintenance. Vendors are integrating IoT‑enabled battery management systems to provide real‑time health diagnostics. Additionally, modular UPS designs are gaining traction, allowing scalable battery configurations. Environmentally conscious procurement policies are also driving the adoption of recyclable battery options.

4. How did COVID‑19 impact the UPS Battery Market and what is the recovery trajectory?

Pandemic‑related disruptions temporarily slowed production and logistics, creating short‑term supply gaps. However, the surge in remote work and digital transformation increased demand for reliable power backup, accelerating market recovery. Post‑COVID, the sector has experienced steady growth, supported by renewed investments in data center resilience and a backlog of delayed infrastructure projects.

5. Who are the major competitors and what is the consolidation landscape in the UPS Battery Market?

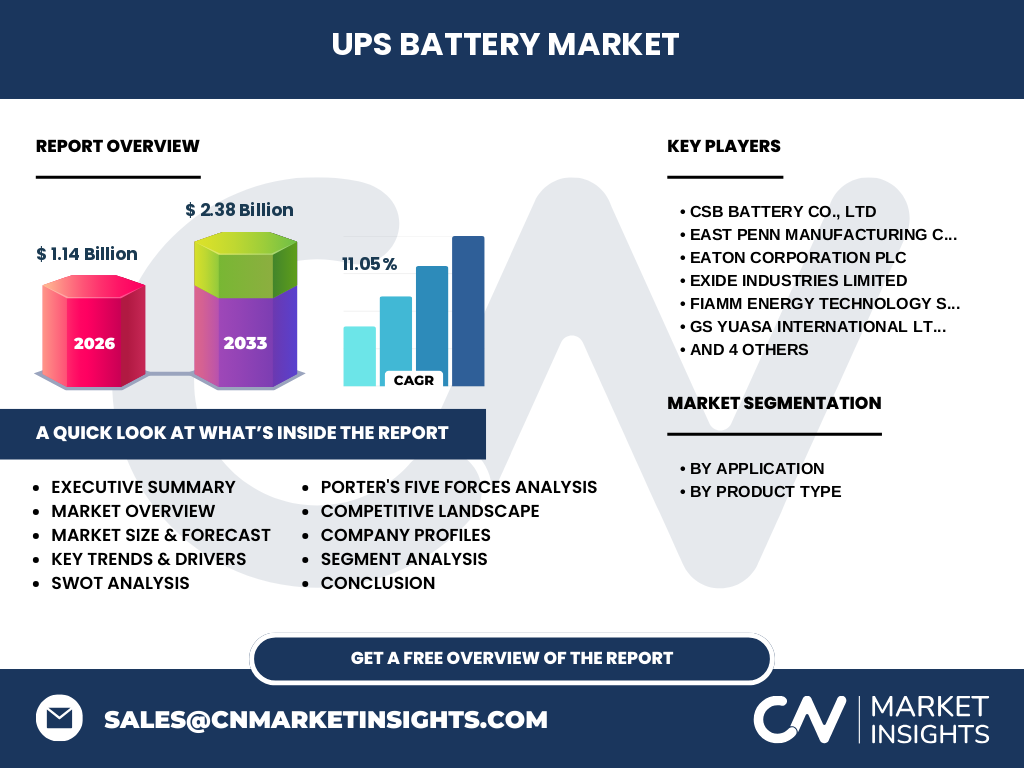

The market is moderately consolidated, led by established manufacturers such as CSB Battery Co., Ltd, East Penn Manufacturing, Eaton Corporation plc, Exide Industries, FIAMM Energy Technology, GS Yuasa International, NorthStar Group Services, Schneider Electric SE, Vertiv Group Corporation, and Leoch International Technology. These firms compete on product reliability, technology innovation, and service networks, while strategic partnerships and acquisitions are common to broaden geographic reach and product portfolios.

6. What are the key findings in the executive summary of the UPS Battery Market?

The UPS Battery Market is valued at 1.14 billion USD in 2026 and is projected to reach 2.38 billion USD by 2033, reflecting a robust CAGR of 11.05 %. Growth is driven by expanding commercial and residential demand, a pronounced shift to lithium‑ion chemistries, and heightened focus on energy resilience. Leading players are investing in advanced battery management solutions, while regional opportunities are strongest in North America and Asia‑Pacific.

7. What are the UPS Battery Market forecasts for 2025‑2032?

Based on the provided CAGR, the market is expected to maintain double‑digit growth through 2032, nearly doubling its size from the 2026 baseline. Forecasts anticipate continued substitution of lead‑acid with lithium‑ion, broader adoption of modular UPS systems, and increased spending on smart monitoring. These dynamics will sustain demand across all application segments and support ongoing revenue expansion for manufacturers.

8. How is the UPS Battery Market sized and shared by segmentation?

By application, the market is divided into Commercial, Residential, and Other Applications, each reflecting distinct usage patterns and performance requirements. By product type, three categories exist: Lead‑Acid, Lithium‑Ion, and Other Product Types. While exact share percentages are undisclosed, commercial usage dominates due to data‑center and industrial needs, whereas residential and niche sectors contribute incremental growth, particularly for lithium‑ion solutions.

9. What is the geographic distribution of the global UPS Battery Market?

The market exhibits a worldwide footprint, with significant activity in North America, Europe, and Asia‑Pacific. Developed economies lead in early adoption of lithium‑ion technologies, while emerging markets drive volume sales of lead‑acid batteries due to cost sensitivity. The combined regional presence supports the overall market size of 1.14 billion USD in 2026.

10. How does each region perform in the UPS Battery Market?

North America shows high penetration of advanced battery systems in data‑center and healthcare sectors. Europe emphasizes sustainability and regulatory compliance, fostering a gradual shift to recyclable lithium solutions. Asia‑Pacific, propelled by rapid industrialization and expanding residential electrification, delivers the largest absolute demand volume. These regional dynamics collectively underpin the market’s growth trajectory.

11. Which companies lead the UPS Battery Market and what are their strategies?

Top players such as Eaton Corporation, Schneider Electric, and Vertiv focus on integrated UPS‑battery solutions with service contracts. Battery specialists like CSB Battery and East Penn emphasize high‑performance lead‑acid and emerging lithium lines. Companies are pursuing R&D for longer cycle life, expanding global service networks, and forming strategic alliances with UPS manufacturers to secure OEM placements.

12. What does Porter’s Five Forces reveal about the UPS Battery Market?

Competitive rivalry is strong due to many established manufacturers and price competition. Supplier power is moderate; raw material sourcing for lithium and lead is concentrated but manageable. Buyer power is growing as end‑users demand higher performance and lower total cost of ownership. Threat of new entrants is limited by capital intensity and regulatory barriers. Substitutes are minimal, limited mainly to alternative power backup like generators.

13. What are the SWOT insights for the UPS Battery Market?

Strengths include essential reliability functions and a growing base of critical infrastructure. Weaknesses involve high material costs and environmental disposal concerns. Opportunities arise from lithium‑ion expansion, smart‑monitoring integration, and green‑energy incentives. Threats consist of supply chain volatility for key metals and potential regulatory tightening on lead‑acid usage.

14. How does the UPS Battery value chain operate?

The value chain starts with raw material extraction (lead, lithium, electrolytes), proceeds to cell manufacturing, module assembly, and integration into UPS systems. Distribution channels include direct OEM supply, third‑party distributors, and service contractors. After‑sales services such as installation, monitoring, and end‑of‑life recycling complete the chain, creating recurring revenue streams for manufacturers.

15. What investment insights are derived from the UPS Battery Market?

Investors should prioritize companies with strong lithium‑ion pipelines and robust service networks, as these segments promise higher margins and recurring income. Funding R&D for battery‑management software and eco‑friendly recycling facilities offers differentiated growth. Geographic diversification, especially targeting Asia‑Pacific expansion, can capture volume growth while mitigating regional regulatory risk.

16. What are the main conclusions of the UPS Battery Market analysis?

The UPS Battery Market is on a rapid expansion path, driven by digitalization, energy resilience, and technology shift toward lithium‑ion. The projected market size of 2.38 billion USD by 2033 underscores strong demand across commercial and residential sectors. Companies that innovate in battery chemistry, management intelligence, and sustainable practices will capture the greatest share of this burgeoning market.

17. Which research methodology was employed for this market study?

The study combined primary interviews with industry experts, OEMs, and end‑users, alongside secondary data from company reports, trade publications, and reputable databases. Quantitative analysis used historical sales figures and the provided CAGR to forecast future revenues. Qualitative assessment involved trend mapping, competitive benchmarking, and scenario analysis to validate findings.

18. What is the scope of this research and its limitations?

The research covers global UPS battery manufacturers, product and application segmentation, and regional performance up to 2033. It focuses on the provided market size, forecast, and CAGR, without delving into proprietary financial disclosures beyond those figures. While comprehensive, the study does not include granular market shares or pricing data due to data availability constraints.

19. Which key companies have recent developments in the UPS Battery Market?

Recent announcements include CSB Battery’s launch of a high‑capacity lithium‑ion module, East Penn’s expansion of a lead‑acid recycling plant, Eaton’s partnership with data‑center operators for integrated UPS solutions, Exide’s introduction of a smart‑monitoring platform, FIAMM’s acquisition of a European battery‑management firm, GS Yuasa’s rollout of a modular UPS battery series, NorthStar’s entry into the residential market, Schneider Electric’s launch of eco‑rated UPS‑battery kits, Vertiv’s service‑contract expansion, and Leoch’s collaboration with renewable‑energy firms to supply storage for grid‑interactive UPS units.