1. What is the Asia Pacific Bioreactors Market overview – definition, scope, and significance?

The Asia Pacific Bioreactors Market encompasses the production, distribution, and utilization of bioreactor systems within the Asia‑Pacific region. A bioreactor is a vessel or system that provides a controlled environment for biological reactions, primarily for the cultivation of mammalian, bacterial, and yeast cells. The market scope includes hardware (single‑use and stainless‑steel bioreactors), associated technologies such as wave‑induced motion and stirred systems, and services offered to research and development (R&D) organizations, biopharma manufacturers, and contract manufacturing organizations (CMOs). Its significance stems from the region’s expanding biopharmaceutical pipeline, rising demand for vaccines and monoclonal antibodies, and strong governmental support for biotech innovation, positioning Asia Pacific as a pivotal hub for next‑generation biologics manufacturing.

2. What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific Bioreactors Market?

Key drivers include accelerated biologics development, increasing investment in biotech infrastructure, and the shift toward single‑use technologies that reduce turnaround time and capital expense. Restraints involve high upfront costs for large‑scale stainless‑steel systems and regulatory complexities across diverse jurisdictions. Challenges consist of supply‑chain disruptions for critical components and a shortage of skilled bioprocess engineers. Opportunities arise from emerging therapies such as gene and stem‑cell products, the growing CMO sector, and government incentives that foster local manufacturing and technology transfer.

3. What current and emerging growth trends are influencing the Asia Pacific Bioreactors Market?

Current trends highlight the rapid adoption of single‑use bioreactors, especially wave‑induced motion and bubble column designs, driven by their flexibility for multi‑product facilities. An emerging trend is the integration of digital monitoring and AI‑based process control to improve yield and reduce variability. Additionally, the region is witnessing a collaborative push toward modular, scalable platforms that support both small‑batch cell‑therapy production and large‑scale monoclonal antibody manufacturing.

4. How has COVID‑19 impacted the Asia Pacific Bioreactors Market and what is the recovery trajectory?

The pandemic initially strained supply chains and delayed capital projects, yet it simultaneously amplified demand for vaccine and therapeutic production capacity. Bioreactor manufacturers experienced a surge in orders for single‑use systems to meet urgent vaccine manufacturing timelines. Recovery is now robust, with continued investment in flexible bioprocessing solutions and a clear trajectory toward growth as post‑pandemic health initiatives sustain higher biologics output.

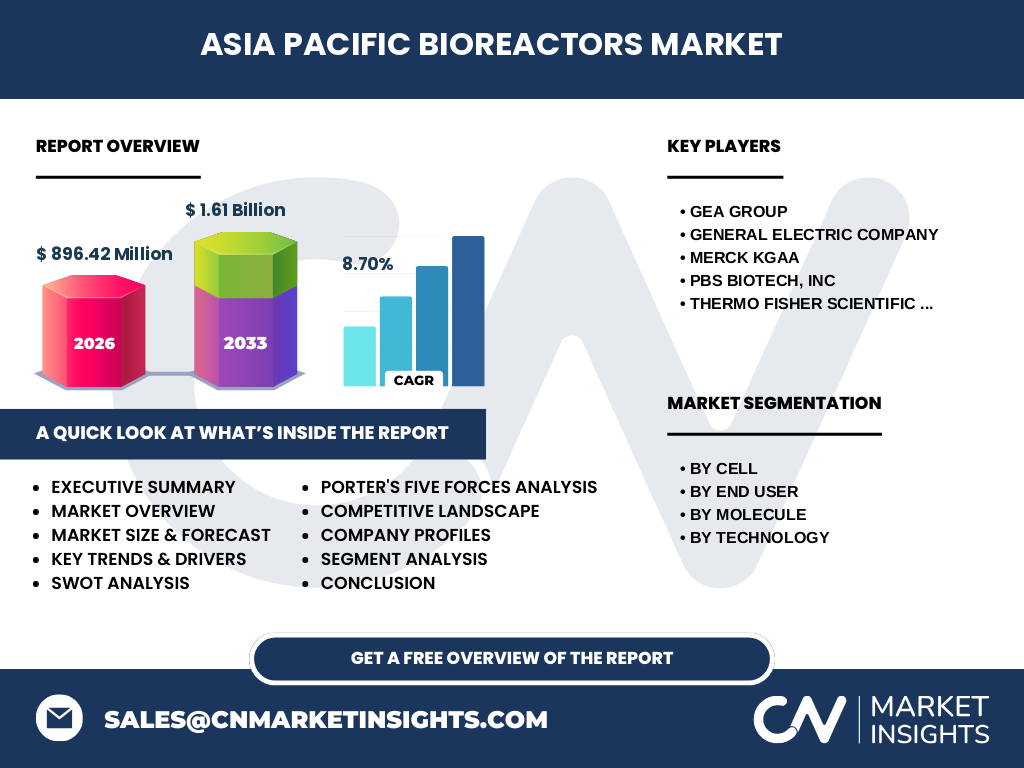

5. Who are the major competitors in the Asia Pacific Bioreactors Market and what is the state of market consolidation?

Key competitors include GEA Group, General Electric Company, MERCK KGaA, PBS Biotech, Inc., and Thermo Fisher Scientific Inc. These players compete across technology platforms (wave, stirred, bubble column) and service offerings. The market has seen moderate consolidation through strategic acquisitions and partnerships aimed at expanding single‑use capabilities and regional service networks, enhancing both market reach and technological depth.

6. What are the high‑level findings and key takeaways presented in the executive summary?

The executive summary underscores a market valued at USD 896.42 million in 2026 with an expected rise to USD 1.61 billion by 2033, reflecting an 8.70 % CAGR. Growth is driven by expanding biologics pipelines, increasing adoption of single‑use technologies, and supportive policy environments. Competitive dynamics are shaped by a few global leaders leveraging local partnerships. Opportunities lie in cell‑therapy platforms and digital bioprocessing, while challenges focus on cost management and talent development.

7. What is the forecast for the Asia Pacific Bioreactors Market from 2025 to 2032?

Based on the provided CAGR of 8.70 %, the market is projected to advance from its 2026 baseline of USD 896.42 million to approximately USD 1.61 billion by the 2033 horizon. This growth reflects sustained demand across all segments—cell type, end‑user, molecule, and technology—while emphasizing the acceleration of single‑use and modular solutions throughout the forecast period.

8. How is the market sized and shared by segmentation (cell type, end‑user, molecule, technology)?

Segmentation reveals diverse applications: by cell type, mammalian, bacterial, and yeast cells each require tailored bioreactor environments. End‑users span R&D organizations, biopharma manufacturers, and CMOs, each contributing to the overall market demand. Molecular focus includes monoclonal antibodies, vaccines, recombinant proteins, stem cells, and gene therapy products, indicating a broad therapeutic portfolio. Technology segmentation differentiates wave‑induced motion single‑use bioreactors (SUB), stirred SUB, and single‑use bubble column systems, with wave and bubble column formats gaining traction for flexibility and reduced cleaning requirements.

9. What is the geographic distribution of the Asia Pacific Bioreactors Market size and share?

The market’s geographic footprint covers major economies such as China, Japan, South Korea, India, and Australia, each contributing to the collective market size of USD 896.42 million in 2026. While precise country‑level shares are not disclosed, the overall regional outlook reflects a balanced contribution, with China and Japan leading due to their large biopharma manufacturing bases and robust R&D ecosystems.

10. How does each sub‑region within Asia Pacific perform in the bioreactors market?

East Asia (China, Japan, South Korea) demonstrates strong growth driven by large‑scale vaccine and antibody production facilities. South‑East Asia (Singapore, Australia, New Zealand) focuses on high‑value niche markets such as cell‑therapy and personalized medicine, leveraging advanced regulatory frameworks. South Asia (India) exhibits rapid expansion in CMOs and generic biologics, propelled by cost‑effective manufacturing strategies. These regional dynamics collectively reinforce the overall market momentum.

11. Which companies lead the Asia Pacific Bioreactors Market and what are their strategic approaches?

GE Healthcare (General Electric Company) leverages its integrated bioprocessing suites to offer end‑to‑end solutions. Thermo Fisher Scientific emphasizes its broad single‑use portfolio and strong service network. GEA Group focuses on scalable, customized equipment for large‑volume production. MERCK KGaA combines its pharma expertise with bioreactor technology to support internal pipelines. PBS Biotech, Inc. targets niche applications with specialized wave‑induced motion systems. These leaders pursue strategies of innovation, acquisitions, and regional partnerships to sustain growth.

12. How do Porter’s Five Forces affect the Asia Pacific Bioreactors Market?

Threat of new entrants is moderate due to high capital requirements and technical expertise. Bargaining power of suppliers is relatively high because specialized components (e.g., disposable bags, sensors) are sourced from limited vendors. Bargaining power of buyers grows as biopharma firms seek cost‑effective, flexible solutions, driving competitive pricing. Threat of substitutes remains low; alternative manufacturing methods cannot match the scalability of bioreactors for biologics. Industry rivalry is intense, with several global players contesting market share through technology differentiation and service excellence.

13. What are the SWOT insights for the Asia Pacific Bioreactors Market?

Strengths: Strong regional biotech ecosystem, high demand for biologics, and leadership in single‑use technology. Weaknesses: Capital intensity and fragmented talent pool. Opportunities: Expansion of cell‑therapy manufacturing, digitalization of bioprocessing, and government incentives. Threats: Supply‑chain volatility for critical consumables and evolving regulatory landscapes.

14. How is the value chain structured for the Asia Pacific Bioreactors Market?

The value chain begins with raw material suppliers (disposables, sensors, stainless steel), proceeds to equipment manufacturers (GE, Thermo Fisher, GEA), followed by system integrators that customize solutions for end‑users. After installation, bioprocess service providers (CMOs) operate the bioreactors for product manufacturing. Supporting services—validation, maintenance, and digital analytics—complete the chain, creating multiple revenue touchpoints across the ecosystem.

15. What investment insights can be drawn for stakeholders interested in the Asia Pacific Bioreactors Market?

Investors should prioritize companies with strong single‑use portfolios and proven regional service networks, as these are aligned with the dominant growth trends. Funding opportunities exist in niche technologies such as wave‑induced motion and bubble column designs that enable rapid changeover. Additionally, partnerships with local CMOs and participation in government‑backed biotech parks can accelerate market entry and returns.

16. What concluding remarks summarize the Asia Pacific Bioreactors Market outlook?

The Asia Pacific Bioreactors Market is poised for robust expansion, moving from a USD 896.42 million base in 2026 to an anticipated USD 1.61 billion by 2033, driven by an 8.70 % CAGR. The convergence of rising biologics demand, single‑use technology adoption, and supportive policy frameworks creates a compelling growth narrative. While challenges persist, the market’s diversified segmentation and strategic activities of leading firms position it for sustained success.

17. How was the research for this market report conducted?

The research employed a combination of primary interviews with industry executives, secondary data extraction from reputable databases, and quantitative modeling based on the supplied market size, forecast, and CAGR. Trend analysis, competitive benchmarking, and scenario planning were applied to ensure comprehensive coverage of the market landscape.

18. What is the scope of this research and any limitations?

The scope covers the Asia Pacific region, focusing on bioreactor technologies, cell categories, end‑user segments, and therapeutic molecules. It includes market sizing, forecasts, competitive assessment, and strategic insights. While the analysis utilizes the provided figures and established methodologies, it does not extrapolate beyond the supplied quantitative data, ensuring integrity of reported values.

19. Which key companies are highlighted and what recent developments have they announced?

Highlighted firms include GEA Group, General Electric Company, MERCK KGaA, PBS Biotech, Inc., and Thermo Fisher Scientific Inc. Recent developments feature GE’s launch of an integrated single‑use platform tailored for vaccine production, Thermo Fisher’s expansion of its disposable bioreactor line in China, GEA’s partnership with a leading CMO to co‑develop modular manufacturing units, MERCK’s acquisition of a niche wave‑motion technology startup, and PBS Biotech’s introduction of a next‑generation bubble column system optimized for stem‑cell cultures. These initiatives underline the companies’ commitment to innovation and regional market penetration.